Changes in appearance and in display of formulas, tables, and text may have occurred during translation of this document into an electronic medium. This HTML document may not be an accurate version of the official document and should not be relied on.

For an official paper copy, contact the Florida Public Service Commission at contact@psc.state.fl.us or call (850) 413-6770. There may be a charge for the copy.

|

DATE: |

||

|

TO: |

Office of Commission Clerk (Cole) |

|

|

FROM: |

Division of Economic Regulation (Mouring, Cicchetti, Daniel, Deason, Fletcher, Golden, Hudson, Jones-Alexis, Lingo, Linn, Maurey, Rieger, Salnova, Simpson, Springer, Stallcup, Thompson, Walden, Williams) Office of the General Counsel (Jaeger, Bennett, Klancke) |

|

|

RE: |

Docket No. 100330-WS – Application for increase in water/wastewater rates in Alachua, Brevard, DeSoto, Hardee, Highlands, Lake, Lee, Marion, Orange, Palm Beach, Pasco, Polk, Putnam, Seminole, Sumter, Volusia, and Washington Counties by Aqua Utilities Florida, Inc.

Docket No. 080121-WS – Application for increase in water and wastewater rates in Alachua, Brevard, DeSoto, Highlands, Lake, Lee, Marion, Orange, Palm Beach, Pasco, Polk, Putnam, Seminole, Sumter, Volusia, and Washington Counties by Aqua Utilities Florida, Inc. |

|

|

AGENDA: |

05/24/11 – Regular Agenda – Proposed Agency Action Except For Issue Nos. 44, 46 and 48 – Interested Persons May Participate |

|

|

COMMISSIONERS ASSIGNED: |

||

|

PREHEARING OFFICER: |

||

|

5-Month Effective Date Waived through 05/24/11 |

||

|

SPECIAL INSTRUCTIONS: |

||

|

FILE NAME AND LOCATION: |

S:\PSC\ECR\WP\100330.RCM.DOC |

|

Issue Description Page

1 Quality of Service (Rieger, Williams, Golden, Thompson, Jones-Alexis)

2 Audit Adjustments Agreed to by Utility (Fletcher)

3 Adjustments to Utility's Pro Forma Plant Additions (Deason)

4 Excessive Unaccounted for Water (Walden, Simpson, Fletcher, Mouring)

5 Used and Useful for Water Treatment (Walden, Simpson, Fletcher)

6 Used and Useful for Storage (Walden, Simpson)

7 Used and Useful for Water Distribution (Walden, Simpson, Fletcher)

8 Excessive Infiltration and Inflow (Walden, Simpson, Fletcher, Mouring)

9 Used and Useful for Wastewater Treatment (Walden, Simpson, Fletcher)

10 Used and Useful for Wastewater Collection (Walden, Simpson, Fletcher)

11 Other Deferred Debits (Linn)

13 Deferred Rate Case Expense (Linn)

14 Appropriate Working Capital Allowance (Linn)

15 Appropriate Rate Base (Deason)

16 Appropriate Capital Structure for Rate Setting (Springer, Salnova, Cicchetti)

17 Accumulated Deferred Taxes (Salnova, Springer)

18 Cost Rates for Short and Long-Term Debt (Springer, Cicchetti)

19 Appropriate Return on Equity (ROE) (Springer, Cicchetti)

20 Appropriate Weighted Average Cost of Capital (Cicchetti, Salnova)

21 Disallow Fines and Penalties (Hudson)

22 Adjustments to Charges from Affiliates (Fletcher, Jaeger)

23 Sludge Hauling, Accounting, and Legal Expenses (Mouring)

25 Director and Officers Liability Insurance (Fletcher)

26 Adjustments to Salaries and Wages (Fletcher)

28 Appropriate Amount of Rate Case Expense (Linn)

29 Adjustments to the Utility's Normalization Adjustments (Mouring)

30 Adjustments to Pro Forma Expense Adjustments (Mouring)

31 Duplicative Billing Adjustment (Mouring)

32 Operating Income Before Revenue Increase (Mouring)

33 Appropriate Pre-Repression Revenue Requirement (Mouring)

34 Subsidy Limit (Stallcup, Lingo)

35 Appropriate Rate Cap Thresholds (Stallcup, Lingo)

36 Appropriate Rate Structures (Stallcup, Lingo)

37 Consolidation of Water Systems (Stallcup, Lingo)

38 Consolidation of Wastewater Systems (Stallcup, Lingo)

39 Appropriate Repression Adjustments (Stallcup, Lingo)

40 Appropriate Monthly Rates (Stallcup, Lingo, Thompson, Fletcher)

41 Revise Miscellaneous Service Charges (Thompson)

42 Service Availability Charges (Fletcher)

43 Customer Deposits (Hudson, Fletcher)

44 Four-Year Rate Reduction for Docket No. 080121-WS (Fletcher)

46 Four-Year Rate Reduction (Linn)

47 Regulatory Asset (Fletcher)

48 Proof of Adjustments (Fletcher)

49 Close Docket (Jaeger, Klancke)

Attachment 1– Matrix of Complaints from Customer Meetings

Attachment 2 – Staff’s Report on AUF’s Phase II Monitoring Reports

Attachment 3 – Excessive Unaccounted For Water

Attachment 4A – Used and Useful Water Treatment

Attachment 4B – Used and Useful Water Treatment

Attachment 5 – Used and Useful Water Distribution

Attachment 6 – Excessive Infiltration and Inflow

Attachment 7A – Used and Useful Wastewater Treatment

Attachment 7B – Used and Useful Wastewater Treatment

Attachment 8 – Used and Useful Wastewater Collection

Attachment 9 – Water Systems in Current Rate Bands.

Schedule 1 – Capital Structure

Schedule 2 – Revenue Requirements

Schedule 3-A – Water Band 1 Rate Base

Schedule 3-C – Water Band 1 Adjustments to Rate Base

Schedule 4-A – Water Band 1 Operating Income

Schedule 4-C – Water Band 1 Adjustments to Operating Income

Schedule 5-A – Water Band 1 Rates

Schedule 3-A – Water Band 2 Rate Base

Schedule 3-C – Water Band 2 Adjustments to Rate Base

Schedule 4-A – Water Band 2 Operating Income

Schedule 4-C – Water Band 2 Adjustments to Operating Income

Schedule 5-A – Water Band 2 Rates

Schedule 3-A – Water Band 3 Rate Base

Schedule 3-C – Water Band 3 Adjustments to Rate Base

Schedule 4-A – Water Band 3 Operating Income

Schedule 4-C – Water Band 3 Adjustments to Operating Income

Schedule 5-A – Water Band 3 Rates

Schedule 3-A – Water Band 4 Rate Base

Schedule 3-C – Water Band 4 Adjustments to Rate Base

Schedule 4-A – Water Band 4 Operating Income

Schedule 4-C – Water Band 4 Adjustments to Operating Income

Schedule 5-A – Water Band 4 Rates

Schedule 3-B – Wastewater Band 1 Rate Base

Schedule 3-C – Wastewater Band 1 Adjustments to Rate Base

Schedule 4-B – Wastewater Band 1 Operating Income

Schedule 4-C – Wastewater Band 1 Adjustments to Operating Income

Schedule 5-B – Wastewater Band 1 Rates

Schedule 3-B – Wastewater Band 2 Rate Base

Schedule 3-C – Wastewater Band 2 Adjustments to Rate Base

Schedule 4-B – Wastewater Band 2 Operating Income

Schedule 4-C – Wastewater Band 2 Adjustments to Operating Income

Schedule 5-B – Wastewater Band 2 Rates

Schedule 3-B – Wastewater Band 3 Rate Base

Schedule 3-C – Wastewater Band 3 Adjustments to Rate Base

Schedule 4-B – Wastewater Band 3 Operating Income

Schedule 4-C – Wastewater Band 3 Adjustments to Operating Income

Schedule 5-B – Wastewater Band 3 Rates

Schedule 3-B – Wastewater Band 4 Rate Base

Schedule 3-C – Wastewater Band 4 Adjustments to Rate Base

Schedule 4-B – Wastewater Band 4 Operating Income

Schedule 4-C – Wastewater Band 4 Adjustments to Operating Income

Schedule 5-B – Wastewater Band 4 Rates

Schedule 3-A – Breeze Hill Water Rate Base

Schedule 3-B – Breeze Hill Wastewater Rate Base

Schedule 3-C – Breeze Hill Adjustments to Rate Base.

Schedule 4-A – Breeze Hill Water Operating Income

Schedule 4-B – Breeze Hill Wastewater Operating Income

Schedule 4-C – Breeze Hill Adjustments to Operating Income

Schedule 5-A – Breeze Hill Water Rates

Schedule 5-B – Breeze Hill Wastewater Rates

Schedule 3-A – Fairways Water Rate Base

Schedule 3-B – Fairways Wastewater Rate Base

Schedule 3-C – Fairways Adjustments to Rate Base

Schedule 4-A – Fairways Water Operating Income

Schedule 4-B – Fairways Wastewater Operating Income.

Schedule 4-C – Fairways Adjustments to Operating Income

Schedule 5-A – Fairways Water Rates

Schedule 5-B – Fairways Wastewater Rates

Schedule 3-A – Peace River Water Rate Base

Schedule 3-B – Peace River Wastewater Rate Base

Schedule 3-C – Peace River Adjustments to Rate Base.

Schedule 4-A – Peace River Water Operating Income

Schedule 4-B – Peace River Wastewater Operating Income

Schedule 4-C – Peace River Adjustments to Operating Income

Schedule 5-A – Peace River Water Rates

Schedule 5-B – Peace River Wastewater Rates

Abbreviations

The following abbreviations used herein are listed below for reference purposes:

ADIT Accumulated Deferred Income Taxes

AFPI Allowance for Funds Prudently Invested

AAI Aqua America, Inc.

ACO Aqua Customer Organization

ASC Accounting Standards Codification

ASI Aqua Services, Inc.

AUF Aqua Utilities Florida, Inc.

AWWA American Water Works Association

BFC Base Facility Charge

CATS Consumer Activity Tracking System

CIAC Contributions in Aid of Construction

CSRs Customer Service Representatives

CUPs Consumptive Use Permits

DEP Department of Environmental Protection

DITs Deferred Income Taxes

DOL Director and Officer Liability

ERCs Equivalent Residential Connections

EUW Excessive Unaccounted for Water

F.A.C. Florida Administrative Code

FPL Florida Power & Light Company

FPUC Florida Public Utilities Company

FRC Firm Reliable Capacity

F.S. Florida Statutes

FWSC Florida Water Services Corporation

GPD Gallons per Day

GPM Gallons per Minute

HD Health Department

I&I Infiltration and Inflow

IT Information Technology

IRC Internal Revenue Code

kgals Thousand Gallons

MACRS Modified Accelerated Cost Recovery System

MCLs Maximum Contaminant Levels

MFRs Minimum Filing Requirements

MGD Million Gallons per Day

MOU Memorandum of Understanding

NARUC National Association Regulatory Utility Commission

NWFWMD Northwest Florida Water Management District

O&M Operations and Maintenance

OPC Office of Public Counsel

POD Production of Documents

RAA Running Annual Average

RAFs Regulatory Assessment Fees

ROE Return on Equity

SARCs Staff-Assisted Rate Cases

SFWMD South Florida Water Management District

SJRWMD St. Johns River Water Management District

SSU Southern State Utilities, Inc.

SRWMD Suwannee River Water Management District

SWFWMD Southwest Florida Water Management District

TDS Total Dissolved Solids

TTHMs Total Trihalomethanes

U&U Used and Useful

USOA Uniform Systems of Accounts

WCI Water Conservation Initiative

WMDs Water Management Districts

WRCAs Water Resource Caution Areas

WTP Water Treatment Plant

WWTP Wastewater Treatment Plant

YES YES Communities, Inc. d/b/a Arredondo Farms

Formation of AUF

AUF’s footprint in Florida is the result of numerous transfers. By Order No. PSC-03-0163-FOF-WS, the Commission approved the transfer of majority organizational control of AquaSource Utility, Inc. from DQE, Inc. to Philadelphia Suburban Corporation, the predecessor to AAI.[1] The Commission subsequently authorized the AquaSource systems to operate under a fictitious name as Aqua Utilities Florida, Inc. by Order No. PSC-04-0715-FOF-WS.[2]

On April 20, 2004, Florida Water Services Corporation (FWSC) entered into an asset purchase agreement with AAI. The closing took place on June 30, 2004. On August 24, 2004, FWSC and AAI filed a joint application for the transfer of FWSC’s land, facilities, and certificates to AAI. The Commission approved the transfer by Order No. PSC-05-1242-PAA-WS.[3]

FWSC was formerly known as Southern States Utilities, Inc. (SSU). SSU’s rates were last established in 1996.[4] At that time, SSU provided water and wastewater service to approximately 102,500 water and 43,000 wastewater customers. In SSU’s last rate case, the Commission approved a capband rate structure that was later affirmed by the First District Court of Appeal (First DCA).[5] The capband rate structure approved in Order No. PSC-96-1320-FOF-WS combined 95 water systems and 43 wastewater systems into 8 rate groups for the water systems and 6 rate groups for the wastewater systems. Each of these groups consisted of several systems with similar costs; however, cross subsidies did exist within each group.

Prior to the transaction between FWSC and AAI, all of the former SSU’s larger, lower-cost systems were sold to municipalities and governmental entities. Under the capband rate structure approved in the 1996 case, SSU’s larger, lower-cost water and wastewater systems subsidized the numerous smaller, higher-cost water and wastewater systems.[6] When these larger systems were removed from the mix, the loss of subsidy resulted in the remaining smaller, higher-cost systems failing to produce revenues sufficient to cover their costs on a stand-alone basis. A comparison of a residential bill for a former SSU wastewater system under a stand-alone basis and under the approved rate band amount in AUF’s 2008 rate case illustrates this point. Based on a residential monthly wastewater gallonage cap of 6,000 gallons, the monthly bill for Beecher’s Point would have been $384 on a stand-alone basis compared to a monthly bill of $82 under the cap band rate structure approved in AUF’s last rate case.

Subsequent Transfers

On September 25, 2006, AAI’s six regulated Florida subsidiaries filed a joint application for acknowledgement of corporate reorganization and approval of name change. The purpose of the reorganization was to consolidate all AAI Commission-regulated water and wastewater assets in Florida under the ownership and name of its Florida corporation, AUF. By Order No. PSC-06-0973-FOF-WS, the Commission approved AAI’s corporate reorganization and request for name change, effective the date of the order.[7]

On December 27, 2007, the Utility filed an application for approval of the transfer of Fairways/Mt. Plymouth, Ltd.’s (Fairways) water and wastewater facilities to AUF. By Order No. PSC-09-0038-PAA-WS, the transfer was approved.[8] On March 21, 2008, the Utility filed an application for transfer of the Breeze Hill water and wastewater systems to AUF. By Order No. PSC-08-0533-FOF-WS, the transfer was approved.[9] On October 22, 2009, the Board of County Commissioners of Hardee County adopted Ordinance No. 2010-02, making the privately-owned water and wastewater facilities in Hardee County subject to the provisions of Chapter 367, Florida Statutes (F.S.). On January 22, 2010, AUF filed an application for certificates for its Peace River systems, under grandfather rights, to provide water and wastewater service in Hardee County. The certificates were granted on April 2, 2010.[10]

Prior Rate Case and Monitoring Plans (Docket No. 080121-WS)

Docket No. 080121-WS was established on February 29, 2008, with the Utility’s notification of its intent to submit an application for general rate relief for its water and wastewater systems in Alachua, Brevard, DeSoto, Highlands, Lake, Lee, Marion, Orange, Palm Beach, Pasco, Polk, Putnam, Seminole, Sumter, Volusia and Washington Counties. By Order No. PSC-09-0385-FOF-WS, the Commission found that the quality of service provided by AUF was marginal for all systems, except the Chuluota system, which was found to be unsatisfactory.[11] Because of concerns with AUF’s customer service, the Commission ordered a six-month Monitoring Plan to address concerns with AUF’s failure to handle customer complaints properly, AUF’s call centers’ process for handling complaints, and incorrect meter readings that resulted in improper bills. The Utility was required to submit monthly reports and other documentation to verify the accuracy of the meter readings and resulting customer bills.

Upon completion of these reporting requirements, staff presented its recommendation regarding AUF’s quality of service at the March 16, 2010 Commission Conference. In addition, staff provided an update of the Utility’s compliance with the Department of Environmental Protection (DEP) and county health departments, which oversee AUF’s quality of product and the operational condition of the water and wastewater facilities. After hearing from staff, interested parties, and several customers at the Commission Conference, the Commission concluded in Order No. PSC-10-0218-PAA-WS (April 2010 Order) that, while preliminary results showed substantial improvement in AUF’s customer service, additional monitoring was required to ultimately determine the adequacy of AUF’s quality of service.[12] The Commission ordered continued monitoring of AUF’s customer service through December 31, 2010, including customer complaints, meter reading and billing accuracy, and environmental compliance. The Commission instructed staff to work collaboratively with AUF and the other parties in order to develop a cost-effective, efficient, and meaningful supplemental monitoring plan.

Staff met with representatives from AUF, the Office of Public Counsel (OPC), the Office of the Attorney General (AG), and several customer representatives to discuss specifics of a cost-effective monitoring plan consistent with the Commission’s direction. AUF and OPC agreed to a jointly-proposed Phase II Monitoring Plan and submitted their Agreement on Scope of Phase II Monitoring. In this document, they agreed upon the criteria by which quality of service would be measured. By Order No. PSC-10-0297-PAA-WS (May 2010 Final Order), the Commission approved the Phase II Monitoring Plan jointly proposed by AUF and OPC with certain Commission-ordered additions.[13] The approved Phase II Monitoring Plan entailed monitoring customer complaints, estimated meter readings, and aesthetic water quality for seven of AUF’s systems; AUF’s and OPC’s filing of reports; staff’s monitoring of environmental compliance; and staff’s further evaluation of customer billing samples through calendar year 2010.

AUF and OPC have filed their responses concerning the Utility’s quality of service in Docket Nos. 080121-WS and 100330-WS in combined responses. Therefore, staff believes it is appropriate to combine its evaluations of AUF’s quality of service for purposes of this recommendation. Accordingly, this recommendation will address AUF’s overall quality of service, as monitored and evaluated in both dockets. This evaluation includes the Chuluota water and wastewater systems, which were involved in the rate case proceeding in Docket No. 080121-WS and were subject to the monitoring plans. The Chuluota systems are not involved in the current rate case proceeding.

Instant Rate Case

On September 1, 2010, the Utility filed an application for approval of interim and final water and wastewater rate increases. By letter dated September 22, 2010, staff advised AUF that its Minimum Filing Requirements (MFRs) had deficiencies. On October 7 and 14, 2010, the Utility submitted its responses to staff’s deficiency letter and satisfied all the identified deficiencies. Thus, the official date of filing has been established as October 14, 2010.

In the test year ended April 30, 2010, the Utility recorded total regulated operating revenues of $8,255,766 and $4,824,531 for water and wastewater, respectively. AUF reported regulated net operating income for the test year of $605,852 for water and $526,976 for wastewater. During the test year, 16,357 water and 6,789 wastewater customers received service from the Utility’s regulated systems. Water and wastewater rates were last established for this Utility in a rate case initiated in 2008.[14]

AUF's application for increased final water and wastewater rates is based on the historical 13-month average test year ended April 30, 2010, with requested adjustments for pro forma plant and operating expenses. In its filing, the Utility states that the rate increase is necessary because AUF has made substantial capital investments in plant and equipment to improve the quality of water and wastewater service. In addition, due to decreased revenue from reductions in consumption, the Utility states that it will not earn a fair and reasonable rate of return on its investment in 2010. In its MFR filing, AUF requested final rates that would result in additional operating revenues of $2,478,491 for water and $1,273,557 for wastewater.

While this is a Proposed Agency Action (PAA) proceeding, there have been several requests for intervention that have already been granted. OPC, YES Companies, LLC (YES), Mr. David L. Bussey (Bussey), and Ms. Lucy Wambsgan (Wambsgan) were granted intervention in this docket. Bussey subsequently withdrew his intervention in the docket. The parties have also commenced discovery in the docket. Additionally, YES filed a Memorandum in Opposition to the rate increase, arguing that AUF’s water product, service, and affordability as to Arredondo Farms has decreased, and, therefore, the rate increase should be denied.

By Order No. PSC-10-0707-FOF-WS, the Commission approved interim rates designed to generate annual water revenues of $9,062,892, an increase of $1,125,588[15] or 13.19 percent, and wastewater revenues of $5,391,338, an increase of $600,215[16] or 11.81 percent.[17]

The original five-month statutory deadline for the Commission to address the Utility’s requested final rates was March 14, 2011. However, by letter dated November 18, 2010, AUF waived the statutory time frame by which the Commission is required to address the Utility’s final requested rates through May 24, 2011. This recommendation addresses the Utility’s requested final rates and the appropriate disposition of the interim rates and regulatory assets. The Commission has jurisdiction pursuant to Sections 367.081 and 367.082, F.S.

Discussion of Issues

Is the quality of service provided by the Utility satisfactory, and, if not, what action should be taken by the Commission?

Recommendation:

Yes. Based on the results of the Phase II Monitoring Plan in Docket No. 080121-WS and staff’s evaluation in the instant rate case proceeding, the overall quality of service provided by AUF for all systems, including Chuluota, is satisfactory. (Rieger, Williams, Golden, Thompson, Jones-Alexis)

Staff Analysis:

Pursuant to Rule 25-30.433(1), Florida Administrative Code (F.A.C.), in a rate case proceeding, the Commission determines the overall quality of service provided by a utility by evaluating the quality of the utility’s product, the operating condition of the utility’s plant and facilities, and the utility’s attempt to address customer satisfaction. The utility’s compliance history with DEP, county health departments (HDS), and Water Management Districts (WMDs), as well as comments or complaints received from customers, are also reviewed.

In AUF’s last rate case, the Commission found that the quality of service provided by the Utility was marginal for all systems, except the Chuluota system, which was found to be unsatisfactory. Because of concerns with AUF’s customer service, a six-month monitoring plan was implemented to review (1) the handling of customer complaints, (2) the Utility’s call centers’ process for handling complaints, and (3) incorrect meter readings and resulting improper bills.

After the initial monitoring period ended, the Commission concluded in the April 2010 Order that while preliminary results showed substantial improvement in AUF’s customer service, additional monitoring was required to ultimately render a determination as to the adequacy of the Utility’s quality of service.[18] The Commission ordered continued monitoring of the Utility’s customer service through the calendar year 2010 and to work collaboratively with AUF and the other parties to develop a cost-effective and focused monitoring plan.

After several meetings, AUF and OPC submitted their Agreement on the Scope of the Phase II Monitoring Plan. By the May 2010 Final Order, the Commission approved the Phase II Monitoring Plan, which required the Utility to file monthly reports concerning customer calls and estimated meter readings.[19] As part of the Phase II Monitoring plan, seven systems were chosen for review concerning non-health-related aesthetic water quality issues, such as taste, color, odor, hardness, turbidity, sediment, and pressure. In addition, the Commission staff was required to track complaints filed at the Commission by AUF’s customers and continue monitoring existing environmental compliance issues.

AUF submitted the required monthly reports and conducted a series of meetings with customer representatives from the seven systems identified in the Phase II Monitoring Plan in order to address aesthetic water quality concerns and identify possible solutions and associated costs. Staff produced monthly reports tracking complaints filed against AUF in the Commission’s Consumer Activity Tracking System (CATS) and monitored AUF’s compliance with environmental regulations. The Utility filed its Final Phase II Quality of Service Monitoring Report (Final Report) on February 28, 2011. While not specifically addressing AUF’s Final Report, OPC provided comments on March 31, 2011, describing its positions with respect to the Utility’s quality of service. AUF responded to OPC’s comments with a filing on April 12, 2011.

The following discussion addresses staff’s evaluation of AUF’s quality of service based on the results of the Phase II Monitoring Plan required in Docket No. 080121-WS, as well as data and information acquired through the rate case proceeding in Docket No. 100330-WS. Staff’s analysis in the instant case, Docket No. 100330-WS, included the Utility’s compliance history with DEP, the county health departments, and WMDs with respect to the quality of water and treated wastewater, the operational condition of the water and wastewater facilities, and the Utility’s attempt to address customer satisfaction. Although the Chuluota water and wastewater systems are not included in the current rate case, AUF’s environmental compliance with respect to Chuluota was evaluated in order to fully address the terms of the Phase II Monitoring Plan.

Quality of the Product/Operational Conditions of the Plant and Facilities

AUF operates 58 water systems and 27 wastewater systems under the Commission’s jurisdiction in Alachua, Brevard, DeSoto, Hardee, Highlands, Lake, Lee, Marion, Orange, Palm Beach, Pasco, Polk, Putnam, Seminole, Sumter, Volusia, and Washington Counties. Many of these systems were constructed 40 to 50 years ago. The majority of AUF’s water systems are small systems that serve primarily residential customers, utilizing basic chlorination for treatment. The Utility’s wastewater systems vary in size and complexity but generally employ treatment methods that are typical when treating domestic wastewater. AUF operates nine water systems that use purchased treated water, and three wastewater systems that use purchased wastewater treatment. These systems have no treatment facilities; therefore, AUF operates only the distribution and collection systems.

As part of its investigation into quality of service, staff evaluated AUF’s compliance with DEP, county health departments, and WMDs. Staff also conducted field inspections of the majority of the Utility’s water and wastewater facilities between October 2010 and December 2010. Nineteen systems in five counties were not inspected because those systems either did not have any plant improvements or operational concerns since the last rate case or were reviewed as part of the Monitoring Plans. DEP inspection reports and correspondence with AUF were reviewed, the operational conditions of the facilities were observed, and items that needed improvement or correction were discussed with AUF staff.

Consent Orders and Warning Letters

Both DEP and the health departments conduct periodic inspections of all water and wastewater facilities and, if environmental compliance violations are found, a Noncompliance Letter is sent describing the violation. A utility is given time to respond and correct the violation. If the utility fails to respond, or if the response is insufficient, the utility is sent a Warning Letter which describes the outstanding violation and DEP’s recourse if the violation is not resolved. If the utility fails to correct the violation following the issuance of a Warning Letter, DEP will issue a Consent Order or Notice of Violation. A Consent Order is issued describing the resolution reached between the utility and DEP. If an agreement is not reached, a Notice of Violation is issued, which may result in a hearing. A Consent Order or Notice of Violation can require payment of a penalty or fine.

The majority of AUF’s water and wastewater systems are in compliance with all applicable standards of DEP, the various health departments, and the WMDs. Most of the systems have recently been inspected by the applicable regulatory agencies and have no outstanding compliance issues. There have been no Notices of Violation issued for any of the systems since the last rate case. Pursuant to the April 2010 Order in Docket No. 080121-WS, AUF had four open Consent Orders, one each for the Chuluota, Tomoka View, and Twin Rivers water systems and the Village Water wastewater system. In addition, the Utility had five pending Warning Letters, one each for the Sunny Hills and Peace River water systems and the Jasmine Lakes, Palm Terrace, and South Seas wastewater systems. Three of the four Consent Orders (Chuluota, Tomoka View, and Twin Rivers) and two of the five Warning Letters (Jasmine Lakes and Palm Terrace) are now closed. Following the April 2010 Order, AUF subsequently received three Consent Orders (Sunny Hills, Peace River, and Arredondo Farms) and one Warning Letter (Jungle Den).

The status of all recent environmental compliance issues are provided in the following three tables. Table 1-1 describes the status of each of these prior Consent Orders and Table 1-2 lists the status of the prior Warning Letters. Table 1-3 lists the status of each of the Consent Orders and Warning Letters issued subsequent to the April 2010 Order.

|

Table 1-1 Status of Consent Orders noted in Order No. PSC-10-0218-PAA-WS |

||

|

System |

County |

Current Status |

|

Chuluota WTP |

Seminole |

DEP Consent Order Closed |

|

Twin Rivers WTP |

Volusia |

HD Consent Order Closed |

|

Tomoka View WTP |

Volusia |

HD Consent Order Closed |

|

Village Water WWTP |

Polk |

DEP Consent Order Open |

The Chuluota system in Seminole County was initially issued a Consent Order in January 2007 regarding violations of the Maximum Contaminant Level (MCL) for Total Trihalomethanes (TTHMs). TTHMs are disinfection by-products created when water containing natural organic carbon is disinfected with chlorine. This system’s source water also has high levels of hydrogen sulfide which cause an unpleasant odor and taste in the water. After modifying plant processes in an unsuccessful attempt to address the TTHM levels, DEP modified the Consent Order in August 2009 to reflect AUF’s plan to construct an ion exchange treatment process. Pursuant to the May 2010 Final Order, staff was instructed to monitor the implementation of the ion exchange plant, and staff and AUF were instructed to address compliance with both the primary and secondary water quality standards. The modified Consent Order also required AUF to pay $5,750 in fines and penalties for the TTHM MCL violations. The ion exchange advanced treatment process was designed to lower the TTHM levels and address the high levels of hydrogen sulfide. The ion exchange treatment units were completed in June 2010 and later received DEP clearance, and they were placed online in August 2010. Once the new plant facilities were online, AUF spent the next few months fine tuning the treatment process and monitoring the effectiveness of the ion exchange treatment. According to DEP, the ion exchange process was successful in lowering the TTHM levels to well below the MCL and reducing the level of hydrogen sulfides in the water. After successful test results, DEP closed the Consent Order for the Chuluota system in December 2010. A follow up inspection in January 2011 noted that the plant was in good operating condition with no deficiencies. Staff believes that the new treatment process has improved both the health-related and aesthetic quality of the water.

The Volusia County Health Department issued Consent Orders in 2009 to the Twin Rivers and Tomoka View water systems regarding MCL violations for TTHMs. Operational modifications were made at the Twin Rivers plant that brought the TTHM levels down to within an acceptable range, and after paying a $1,400 penalty, the Consent Order was closed in November 2009. To resolve the TTHM problems at the Tomoka View plant, AUF modified the treatment process and constructed a chloramination system that was placed into service in December 2009. A flushing program was also implemented for the distribution system. AUF paid a $5,400 penalty and was required to sample monthly for TTHMs. After achieving six consecutive monthly samples for TTHMs below the MCL and maintaining a running annual average below the MCL, the Consent Order was closed in October 2010. Staff’s recommendation with respect to the regulatory treatment of fines or penalties paid by AUF is addressed in Issue 21.

DEP issued a Consent Order in May 2009 related to the Village Water wastewater system and the long-term effluent disposal capacity of the percolation ponds. AUF asserts that the ponds were constructed below the ground water table and receive runoff water associated with the nearby Polk County Parkway and, as a result, frequently operate near capacity. The Utility is required to identify an alternative effluent disposal option by May 2011. They have examined a number of alternatives and are currently negotiating with a nearby property owner to acquire land for a spray field for effluent disposal, which they anticipate will be operational in November 2011. AUF has requested inclusion of the project as pro forma plant.

|

Table 1-2 Status of Warning Letters noted in Order No. PSC-10-0218-PAA-WS |

||

|

System |

County |

Current Status |

|

Sunny Hills WTP |

Washington |

DEP Consent Order Open |

|

Peace River WTP |

Hardee |

DEP Consent Order Open |

|

Jasmine Lakes WWTP |

Pasco |

DEP Warning Letter Closed |

|

Palm Terrace WWTP |

Pasco |

DEP Warning Letter Closed |

|

South Seas WWTP |

Lee |

DEP Warning Letter Open |

In July 2009, AUF received a Warning Letter regarding the Sunny Hills water system storage capacity. DEP determined that the existing storage capacity for the water system is not sufficient, and it is requiring the Utility to increase its current storage capacity by replacing the existing storage tanks with larger ones. AUF retained an engineering firm to examine the system configuration and storage capacity. DEP issued a Consent Order in December 2010 requiring AUF to develop a plan to increase the storage capacity by February 2011 and pay $2,095 in penalties. AUF submitted its plan to increase storage capacity at the Sunny Hills facility and estimates that the tanks will be in service by June 2011. The Utility requested inclusion of the new storage tanks as pro forma plant.

In August 2009, DEP issued a Warning Letter for the Peace River water system as a result of tests which indicated Gross Alpha Particle Activity exceeding the MCL. AUF signed a DEP Consent Order for the Peace River system in June 2010 that required AUF to pay $1,500 in penalties and perform bimonthly sampling for Gross Alpha Particle Activity and combined Radium for 24 consecutive months. AUF has also conducted an ion exchange pilot study to evaluate possible treatment methods. The Consent Order will remain open pending the outcome of the bimonthly sampling. The Utility requested that the design of an alternative treatment process to address Gross Alpha Particle Activity be included as a pro forma project.

The Warning Letters issued by DEP for the Jasmine Lakes and Palm Terrace wastewater facilities in Pasco County related to whether the percolation ponds were subject to DEP rules addressing ground water quality. In a March 2007 Warning Letter, DEP required AUF to address the impact of the Jasmine Lakes percolation ponds on the adjacent ground water. In addition, the Utility was required to provide summary reports regarding the Palm Terrace land application system, provide results from an investigation of the use of an intermediate well, and construct a cross-over pipe between two percolation ponds as a part of the permitting requirements for the treatment plant. After further evaluation and testing by both AUF and DEP, it was determined that DEP rules did not apply to the Jasmine Lakes or Palm Terrace ponds because the ponds were grandfathered and, therefore, covered under separate regulations based on the original construction dates of the ponds. AUF received a renewed wastewater treatment plant permit for the Palm Terrace system in September 2009, and DEP issued a Consent Order in August 2010 in resolution of the Jasmine Lakes Warning Letter. DEP acknowledged that the rule violations initially cited in the Warning Letters for both Jasmine Lakes and Palm Terrace did not apply; however, AUF was required to pay $23,000 in penalties related to other percolation pond and ground water rule violations for the Jasmine Lakes system. All Warning Letters and Consent Orders for Jasmine Lakes are now closed.

In February 2010, DEP issued a Warning Letter for the South Seas wastewater system in Lee County in response to reject water storage tank failures and leaks that resulted in wastewater spills at the treatment facility. As a result, AUF has replaced four storage tanks at the facility, and a Consent Order is expected to be issued in resolution of this matter. AUF requested inclusion of the project in pro forma plant.

|

Table 1-3 Status of New Consent Orders and Warning Letters |

||

|

System |

County |

Current Status |

|

Jungle Den WTP |

Volusia |

HD Warning Letter Open |

|

Arredondo Farms WWTP |

Alachua |

DEP Consent Order Closed |

|

Tomoka View WTP |

Volusia |

WMD Consent Order Closed |

|

Twin Rivers WTP |

Volusia |

WMD Consent Order Closed |

The Jungle Den water system in Volusia County is a consecutive system that purchases bulk water from St. Johns River Utility, Inc. (St. Johns). In June 2010, St. Johns modified its water treatment process and installed a chloramination system. As a result, AUF was required to notify customers of this treatment modification before the system became operational. AUF did not provide the required notice until after the system was placed online, and this caused the Volusia County Health Department to issue a Warning Letter in February 2011. AUF expects the Health Department to issue a Consent Order that will summarize the resolution of this issue.

AUF was issued a Consent Order on August 26, 2010, for the Arredondo Farms wastewater system in Alachua County as a result of equipment failures that led to sewage spills. The Utility repaired the equipment, made additional system improvements, and paid $4,500 in penalties. The Consent Order was closed in October 2010. The Utility requested that the costs associated with the plant improvements be included in this rate case.

With respect to the evaluations performed by the WMDs, the majority of AUF’s systems are in compliance with the applicable rules and regulations. However, the St. Johns River WMD issued a Consent Order in April 2010 for the Tomoka View and Twin Rivers water systems in Volusia County after it was discovered that those systems had never been issued the required consumptive use permits (CUPs). Once this was discovered, AUF filed CUP applications. The systems were issued CUPs in November 2009, AUF paid $3,047 in penalties and costs as required by the Consent Order, and the Consent Order was closed.

Summary of Quality of Product and Operational Condition of the Plant and Facilities

AUF is in compliance with the applicable DEP, county health department, and WMD standards for the majority of its water and wastewater systems. AUF has no outstanding Notices of Violation. Currently, there are three outstanding Consent Orders related to (1) GAPA Particle Activity at the Peace River water system exceeding the MCL, (2) storage capacity at the Sunny Hills water system, and (3) effluent disposal at the Village Water wastewater system. There are two outstanding Warning Letters related to (1) AUF’s notification of the chloramine conversion at the Jungle Den water system, and (2) the replacement of reject water storage tanks at the South Seas wastewater treatment plant. As previously described in detail, AUF appears to be working to address the outstanding compliance issues with DEP, county health departments, and WMDs. Staff believes that the reduction in number of open Consent Orders and Warning Letters reflects an improvement in AUF’s efforts to address environmental compliance issues. Further, based on staff’s inspections and evaluation, the operational condition of AUF’s water and wastewater facilities is satisfactory. Therefore, staff recommends that the quality of the treated water and wastewater and the operational condition of the AUF plants and facilities, including the Chuluota system, be considered satisfactory.

The Utility’s Attempt to Address Customer Satisfaction

Staff reviewed comments from customer meetings, as well as correspondence filed in the current rate case docket and customer complaints received by AUF and the Commission. Staff also reviewed comments filed by OPC, as well as comments submitted on April 11, 2011, by YES Companies, LLC d/b/a Arredondo Farms (YES), which is the owner of the Arredondo Farms Mobile Home Park and representative of the customers of the corresponding system. Many of these comments are generally addressed below, describing concerns brought up at customer meetings. In addition, the unique concerns related to the aesthetic quality of water for the Arredondo Farms system are discussed below within the Joint Secondary Water Quality Task Force section of this recommendation. Additionally, in accordance with the Phase II Monitoring Plan, staff reviewed documentation filed by AUF as well as complaints filed with the Commission. The following is a summary of the customer complaints and concerns, as well as AUF’s, OPC’s, and other interested parties’ filings.

Customer Meetings

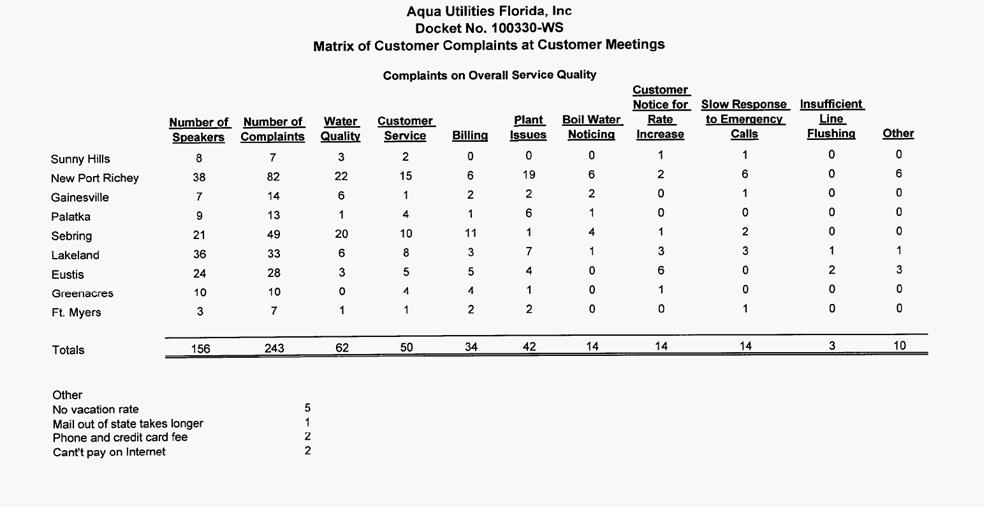

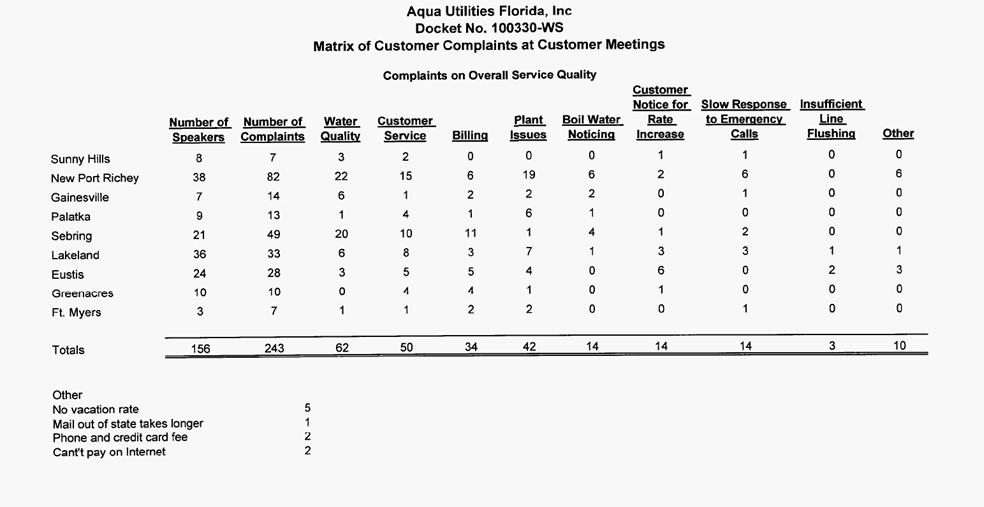

More than 700 AUF customers attended meetings held in nine locations around the state between October 14, 2010, and November 18, 2010. The purpose of the meetings was to allow customers to ask questions and provide input regarding AUF’s quality of service. According to OPC’s March 31, 2011 response to AUF’s February 28, 2011 Final Report, approximately 156 customers spoke during these meetings and raised 243 specific complaints. Attachment 1 is a table from OPC’s March 31, 2011 filing which presents the number of customers who spoke and the number of complaints discussed, categorized by meeting location and complaint classification. Local legislators and county officials also attended several of the meetings and provided comments. Table 1-4 reflects the number of customers who attended each customer meeting and the number who spoke.

|

Table 1-4 Customer Meeting Attendance & Speakers |

|||

|

Date |

Location |

Customers Attended |

Customer Speakers |

|

October 14, 2010 |

Chipley |

27 |

8 |

|

October 20, 2010 |

New Port Richey |

450 |

38 |

|

October 21, 2010 |

Gainesville |

9 |

7 |

|

October 22, 2010 |

Palatka |

9 |

9 |

|

October 27, 2010 |

Sebring |

30 |

21 |

|

October 28, 2010 |

Lakeland |

135 |

36 |

|

October 29, 2010 |

Eustis |

58 |

24 |

|

November 4, 2010 |

Greenacres |

13 |

10 |

|

November 18, 2010 |

Ft. Myers |

3 |

3 |

|

Total |

|

734 |

156 |

At each of the customer meetings, staff gave opening remarks, and AUF and OPC were given an opportunity to provide comments. A Utility representative explained the company’s efforts to improve its customer service. The Utility’s speaker noted that, over the last two and a half years, $8.4 million has been spent on infrastructure improvements around the state, with an additional $3.7 million planned for capital improvements. AUF asserted that the improvements were necessary to comply with DEP regulations and to improve water and wastewater quality and service reliability. Generally, the improvements dealt with water meter replacements and non-growth related water and wastewater treatment plant modifications, such as well rehabilitations, electrical upgrades, structural repairs, pumps, motors, and hydropneumatic tank replacements. In the water distribution and wastewater collection systems, improvements were made to reduce inflow and infiltration and improve water pressure and fire flow.

OPC also provided comments with respect to customer concerns. According to OPC’s analysis of complaints from customer meetings, docket correspondence, and AUF’s Final Report filed in Docket No. 080121-WS, the Utility’s quality of service “has not improved in any meaningful way,” and the Utility still has serious ongoing quality of service issues to be addressed. Of the 243 specific complaints received, presented by meeting location in Attachment 1 and summarized in Table 1-5, OPC identified water quality and customer service as the most prevalent categories. The majority of the 62 water quality complaints provided during customer meetings were raised during the New Port Richey and Sebring meetings, with 22 and 20 complaints, respectively. The majority of the 50 customer service complaints were raised during the same meetings, with 15 and 10 complaints, respectively.

|

Table 1-5 Customer Meeting Complaints by Category |

|

|

Type of Complaint |

Total |

|

Water Quality |

62 |

|

Customer Service |

50 |

|

Billing |

34 |

|

Plant Issues |

42 |

|

Boil Water Noticing |

14 |

|

Rate Increase Noticing |

14 |

|

Slow Emergency Reponses |

14 |

|

Insufficient Line Flushing |

3 |

|

Other |

10 |

|

Total |

243 |

Staff attended the customer meetings and reviewed the recordings of the customer comments from the meetings. The majority of those who attended the meetings repeatedly expressed concern over the justification for the proposed rate increases. Most of the comments made by the 156 customers who spoke were about affordability and the economic burden placed on them in paying for essential water and wastewater services. They complained that AUF’s rates are predatory, punishing large families, and causing significant lifestyle changes.

Customers also complained about the quality of their water and wastewater service and indicated a desire to receive service from other providers. They described concerns with respect to numerous issues, including taste, sediment, odor, color, low pressure, stained fixtures and clothes, damage to internal plumbing fixtures, outages, boil water notices, billing, and customer service. The billing issues involved backbilling, consumption variations and meter accuracy, discontinuance of service, and billing adjustments. The comments related to customer service concerned rude treatment by the Utility’s customer services representatives and being put on hold for lengthy periods of time. There were also comments about Utility property being neglected and private property being damaged as a result of Utility activity. Staff reviewed and followed up on approximately 150 individual complaints presented by customers during the meetings.

The Utility attempted to respond to individual customer comments made at each of the meetings by researching its customer records and responding directly to many of the customers. AUF also responded to staff’s requests for additional information related to individual customer comments. The Utility provided staff with customer billing histories and details related to cut-offs due to non-payment, backbilling, payment plans, AUF’s bill adjustment policy, estimated billings, late fees, boil water noticing information, and quality of product issues. At staff’s request, the Utility performed field investigations to address customer concerns related to meter accuracy. The following is a summary of many of the concerns raised at the customer meetings and AUF’s responses to those issues.

AUF has 241 customers in the Fairways system in Lake County who currently receive separate bills for water and irrigation services at the same location. According to AUF, the current billing system cannot produce a combined bill for these customers; however, customers are allowed to pay both bills with one payment. In response to a staff inquiry, AUF indicated that a new billing system would have to be installed in order to provide a single bill for both water and irrigation service to the same customer.

Several AUF customers complained about receiving a single large bill representing several months of usage after not receiving a bill for several months. Consistent with Rule 25-30.350, F.A.C., AUF allowed customers to pay for the unbilled service over the same time period as the period during which the underbilling occurred or some other mutually agreeable time period. Some customers complained they had not originally been billed for wastewater service and subsequently received a bill for several months of service once AUF identified the error. When this issue was brought to AUF’s attention, the Utility provided a payment plan to the customers.

Customers also complained about consumption variations and meter accuracy. If a leak is suspected by an AUF employee, the Utility attempts to notify the customer of a possible leak on the customer’s property. When a customer contacts a service representative with questions about water consumption, the representative informs the customer of ways to check for leaks. When a customer identifies and reports a leak on the customer side of the meter, AUF notifies the customer that repairing the leak is the customer’s responsibility. The customer is offered an opportunity to provide the Utility with a copy of the paid repair bill (or some other documentation if the leak was self-repaired). AUF reviews the customer’s documentation and grants bill adjustments on a case-by-case basis. Adjustments are based upon a comparison between the customer's highest usage during the period the leak was detected and the customer's average usage.

If a leak is not detected, pursuant to Rule 25-30.266, F.A.C., upon the customer’s request, AUF will perform a field test of the meter to determine its accuracy at no cost to the customer. If the customer is not satisfied with the results of the field test, the customer may request that the meter be removed and tested by a laboratory. The utility may require a deposit to defray the cost of the bench test. If the meter is found to register accurately or below accuracy standards, the utility may retain the deposit. Five customers who spoke at the customer meetings requested that AUF perform a field test on their meter. AUF performed the field tests and reported the results to be within accuracy limits prescribed by Rule 25-30.262, F.A.C.

Several customers complained that their water service had been improperly shut off. According to AUF, once a customer receives a bill, the customer has 21 days to make a payment before being considered delinquent, pursuant to Rule 25-30.320, F.A.C. Once the account becomes delinquent, AUF sends the customer a notice indicating that service will be discontinued within 10 days if payment is not received. Rule 25-30.320, F.A.C., requires a utility to provide 5 working days’ written notice, separate and apart from a bill for service. In addition to providing the shut-off notice, AUF calls the customer prior to discontinuing service. This phone call is not required but is offered as a courtesy to the customer. Additionally, in the event of hardship or financial troubles, AUF offers a payment plan for outstanding bills. The Utility’s policy is to offer two opportunities for a payment plan per account.

A few customers complained about the cost of using an online payment facilitator, such as Western Union. AUF does not currently have the ability to allow customers to make payments directly to the Utility online; however, its website has a Speedpay link which allows customers to connect to a Western Union site to make a payment to AUF. This service is made available to customers in other regulated industries. Western Union charges a fee for this service; the Utility does not receive any portion of this fee. However, AUF is working to implement a new program, known as Aqua Online, which will allow the Utility’s customers to view and pay bills online. According to AUF, the new program is expected to be available in the second quarter of 2011 and will be provided at no cost to customers.

Several customers with pools expressed concern that their bills for wastewater service were based on water usage during those months when a significant portion of their water usage was due to filling their pools. While residential wastewater bills are based on water usage, there is a 6,000-gallon cap on the amount of water used to calculate the wastewater bills for all rate bands. However, for customers whose typical monthly water usage is below the cap, their water usage exceeds the cap in those months when their pools are filled. AUF implemented a pool credit policy in May 2009, which allows the Utility’s customers to receive a credit on their wastewater bill for the water used to fill the customers' pools. The credit is based on the difference in their typical monthly water usage and the cap used to calculate the wastewater bill.

Customers also described concerns related to boil water notices, which are issued when water pressure drops below the minimum pressure required by DEP or a county health department. When there is a significant drop in water pressure due to a line break or some other event (whether planned or unplanned), AUF posts notices at individual homes in the affected area. The information is also posted on the Utility’s internal website, which is used by customer service representatives (CSRs) to relay important information to customers. All boil water notices remain in effect until testing finds the water to be safe and satisfactory. The Utility’s field staff then hand-delivered rescind notices to all affected customers. In addition, AUF indicated that it has begun using a telephonic relay system called SwiftReach to contact the affected customers more expeditiously.

OPC made reference to untimely boil water notices. In response, AUF states that it strictly enforces and follows DEP guidelines on issuing boil water notices. Staff’s review of a report prepared by AUF indicated that during the test year, boil water notices were issued at more than 40 of the Utility’s water systems as a result of unplanned events, such as main breaks or other system failures, as well as planned system improvements, such as line replacements and tank inspections and replacements. Some events affected only a street or two within a system and lasted for a few hours, while other events were system-wide and remained in effect for 48 hours. Some systems, like Peace River in Hardee County, had multiple boil water events in a single year. Each of these events lasted one day; three of the events resulted from either equipment failure or a line break, and one of the events was a planned flushing event.

Most of AUF’s distribution and collection lines are located in roadside easements, while some lines are located in the back of customers’ properties, which often results in access problems. These lines were in place prior to AUF’s acquisition of the systems. Although this is not the preferred method of installation, AUF has not relocated these existing lines due to significant relocation costs. Prior to the installation of remote read meters in 2007 and 2008, the Utility had considerable access challenges in several systems due to fencing, guard dogs, and customers who would not allow access to read meters. Since remote read meters have been installed throughout AUF’s service territory, gaining access to meters for meter reading is no longer a problem. In addition, AUF has easement rights for repairs if needed. According to the Utility, its policy is to minimize disruption and reduce any and all property damage to the surrounding area.

In early 2010, there was a house fire within the Lake Gibson system in Polk County. This fire occurred in the general vicinity of two fire hydrants that AUF had identified and tagged as inoperable while replacement hydrants were being ordered. AUF asserts in its April 2010 letter that the hydrants were tagged in January 2010; however, its Fire Hydrant Inspection Reports indicate that operational issues were discovered in January 2008. Pursuant to Rule 25-30.231 F.A.C., each utility shall operate and maintain all of its facilities and equipment in a safe, efficient, and proper condition. According to AUF, the hydrants were tested and found to be inoperable during a routine inspection. The Polk County Fire Department was then contacted about the fire hydrants being out-of-service. Three months after the hydrants were tagged, the replacement hydrants were installed. AUF has stated that it tests its hydrants on an annual basis in accordance with American Water Works Association standards. Any hydrant found to be inoperative or difficult to operate is marked out-of-service and reported for repair or replacement. This information is then logged and reported to the local fire department. In this instance, based on the Utility’s reports, this process took approximately two years. Staff would expect that any repairs deemed necessary during AUF’s inspections would be completed more timely in the future. Since the hydrants have been replaced, staff does not believe that this incident rises to the level of requiring enforcement action.

There was also concern over a replacement hydropneumatic tank in the Lake Gibson system that was left on private property for an extended period of time and remained uninstalled for approximately four years. According to AUF, the replacement tank was larger than the original tank, requiring redesign and replacement of portions of the fittings to accommodate the larger tank as well as a new permit from DEP. The tank was recently installed, and the cost associated with its installation is included in the Utility’s pro forma plant improvements.

As an unintended by-product of AUF’s attempt to control the high sulfur level of the raw water in the Highlands County systems, customers periodically experience extremely high dosages of chlorine. The Utility reported that it requires both the use of chlorine and continued flushing to maintain water quality. As part of its secondary aesthetic water quality project, AUF is currently in the process of having filtering systems designed and installed. Once the filtering systems are installed, the extreme levels of chlorine that these customers currently experience should diminish. Staff’s recommendation regarding AUF’s requested inclusion of this project as pro forma plant is discussed in Issue 3.

Customers expressed concern over an erosion problem that they believe was caused by AUF’s failure to properly maintain its facilities in Putnam County. The Utility’s Palm Port water treatment plant is located on a lot that adjoins a navigable canal. Customers pointed out that use of this canal is being threatened by unwanted sediment flowing into it from the Utility’s property. The Utility met with neighboring property owners to discuss possible corrective action. The area shows evidence of settling around a storm water culvert on Utility property. Repairs to the culvert and a sea wall will be needed to correct the erosion problem. AUF intends to complete these repairs, as well as re-grade and sod as needed, by this summer.

Customer Complaints and Correspondence

In its filing, AUF provided information regarding customer complaints that it received during the test year. Staff also reviewed complaints related to AUF in CATS and data on complaints received by AAI’s call centers filed in response to the Phase II Monitoring Plan requirements in Docket No. 080121-WS.

AUF reported that an average of 86,699 calls per month were answered at AAI’s 3 call centers serving 11 states, with an average of 84 percent of calls being answered in less than 90 seconds. In addition, AUF reported receiving an average of 5,423 calls per month at the call centers from Florida customers during May 2010 through December 2010, with an average of 792 calls per month requiring assistance from a CSR. AUF reported that the majority of calls coming into the call centers were related to move ins/move outs, collections activity, payment inquiries, and bill explanations, many of which were handled by the Interactive Voice Response system.

During the test year, the Commission received 46 service complaints and 131 billing complaints, all of which have been closed. In addition, from the end of the test year until March 31, 2011 (11 months), 127 additional complaints were received, 91 of which were filed during the Phase II monitoring period. As of May 10, 2011, all of the additional complaints were closed except for 2 billing complaints.

As part of the Phase II Monitoring Plan, the May 2010 Final Order required that staff track complaints filed by AUF customers with the Commission’s call center as documented in CATS. Staff provided monthly reports to all parties that included the number of complaints received for the month, type of complaints, dates the complaints were opened and closed, and counties in which the customers reside. Between May 2010 and December 2010, the Commission received a total of 91 complaints from AUF customers, with an average of 11 complaints per month. As shown on Table 1-6, the majority of complaints pertained to improper billing, representing over 70 percent of AUF complaints filed with the Commission.

|

Table 1-6 AUF Complaints Received by the Commission’s Call Center May 2010 - December 2010 |

||

|

Type of Complaint |

Number of Complaints |

Percentage of Complaints |

|

Improper Bills |

64 |

70.3% |

|

Quality of Service |

9 |

9.9% |

|

Improper Disconnects |

7 |

7.7% |

|

Outages |

5 |

5.5% |

|

Repairs |

4 |

4.4% |

|

Delay in Connection |

2 |

2.2% |

|

Total |

91 |

100.0% |

Staff reviewed the 91 complaints to determine the timeliness of AUF’s response, as well as the length of time to close the complaints. Rule 25-22.032(6)(b), F.A.C., requires in part that a utility provide a written response to the customer’s complaint to staff within 15 working days after staff sends the complaint to the utility. Further, Rule 25-22.032(6)(e), F.A.C., requires in part that the utility respond in seven working days to each subsequent request by staff after the initial utility response. Staff’s review revealed that AUF responded to 90 of the 91 complaints within the required 15-day timeframe and to 1 complaint on the 16th day. Also, one complaint to which AUF filed an initial timely response, was later changed to untimely upon closing of the complaint because AUF responded to staff’s subsequent request for information within eight days rather than seven days as required by rule.

In addition, staff reviewed the length of time between the date each complaint was filed by the customer and then closed by the Commission as a resolved complaint. As shown in Table 1-7, most complaints were closed within five to six weeks. Specifically, 75 of the 91 complaints were closed in 6.5 weeks or less, representing 82.4 percent of the complaints. Additional time was needed to resolve complaints that involved meter bench tests or customer requests for additional review following the initial complaint resolution.

Table 1-7 AUF Complaint Response Time May 2010 - December 2010 |

||

|

Complaint Closed In |

Number of Complaints |

Percentage of Complaints |

|

3-1/2 weeks |

1 |

1.1% |

|

4-1/2 weeks |

5 |

5.5% |

|

5 to 5-1/2 weeks |

48 |

52.7% |

|

6 to 6-1/2 weeks |

21 |

23.1% |

|

7 to 8 weeks |

5 |

5.5% |

|

2 to 3 months |

5 |

5.5% |

|

Over 3 months |

6 |

6.6% |

|

Total |

91 |

100.0% |

Based on a review of AUF customer complaints received by the Commission, staff believes an average of 11 complaints per month is low when compared to AUF’s customer base of approximately 17,000 water customers and 6,900 wastewater customers. Further, the Commission’s records indicate that AUF has responded to customer complaints filed with the Commission in a timely manner and in accordance with Commission rules.

As of March 31, 2011, the Commission received approximately 415 letters and emails in which customers expressed concern regarding the current rate case. The majority of customers expressed opposition to the rate increase and frustration regarding the impact that increased rates would have on their finances. Customers described their overall dissatisfaction with the level of service they receive and their complaints about the quality of the water; they also asked specific questions about the AUF rate case and how it is being processed. Comments were also submitted by several local and state government officials expressing opposition to the Utility’s application for a rate increase, including letters from State Legislators, the Pasco County Legislative Delegation, Pasco County Commissioners, and Polk County Commissioners. Staff responded to the letters and e-mails offering information regarding the Commission’s process and responding to questions posed. In addition, staff reviewed over 900 petitions that were filed with the Commission on April 26 and May 5, 2011, by 2 Legislators who represent customers in Pasco County.

Secondary Water Quality Task Force

For many of AUF’s water systems, the raw water source contains naturally occurring impurities, including iron and sulfides, which cause undesirable color, taste, and odor, as well as calcium and other minerals, which can lead to hard water. These aesthetic qualities are not considered health issues by DEP, and as such are considered secondary standards with less strictly enforced regulation. The impurities can often be difficult and expensive to remove. As discussed below, many AUF customers have expressed their displeasure with the quality of the water they receive from the Utility. The Commission’s May 2010 Final Order established a Joint Secondary Water Quality Task Force, consisting of representatives from AUF, OPC, other parties, and one or two designated customer representatives from each of seven system locations, including Lake Josephine, Sebring Lakes, Leisure Lakes, Rosalie Oaks, Tangerine, Tomoka View, and Zephyr Shores. These systems were chosen based on a review of customer complaints at public hearings held in Docket No. 080121-WS, customer complaints received by AUF, the results of an AUF customer survey, as well as input from the Utility’s staff and a review of water quality data.

During the summer of 2010, AUF conducted a series of meetings in each of the seven chosen locations to discuss each system’s unique aesthetic concerns, treatment options, and the associated costs. A meeting was held on January 20, 2011, with AUF, staff, OPC, and other interested persons to discuss the preliminary results.

Lake Josephine, Sebring Lakes, and Leisure Lakes (Highlands County)

Because the Lake Josephine and Sebring Lakes water systems are interconnected, the customer meetings for those systems were combined. The two systems, combined, have approximately 554 customers. Representatives from Lake Josephine were invited but did not attend. Two alternatives, including a filtering process and looping the distribution system, were considered to address the sulfur, taste, and odor in the water, which stem from naturally occurring hydrogen sulfide. AUF’s cost/benefit analysis showed that the cost of looping was considerably more expensive and less effective than the filtering option. AUF has proposed a filtering process for the Lake Josephine and Sebring Lakes water systems.

The Leisure Lakes system, with approximately 285 customers, has naturally occurring hydrogen sulfide, calcium, and sediment in the water. AUF implemented a flushing plan in 2009, which did not fully resolve the odor and taste issues. The Utility has also proposed a filtering process for the Leisure Lakes water systems.

According to AUF, the customer representatives of each of the systems seemed satisfied with the Utility’s proposed improvements to address the odor and taste of the water in the Lake Josephine, Sebring Lakes, and Leisure Lakes water systems. AUF is moving forward with the purchase of and permitting for the filters for those systems.

Rosalie Oaks (Polk County)

According to AUF, the Rosalie Oaks system experiences taste, odor, and clarity issues, which stem from sporadic flows and naturally occurring sediment in the water. The system’s 93 customers use the water service primarily on weekends and holidays. AUF evaluated the water quality, distribution system, and flushing frequency. Because the system lacked critical valves and flushing hydrants, the Utility devised a directional flushing program for Rosalie Oaks by installing a shorter water main extension and flushing hydrant to flush the system properly. A flushing protocol was developed to address the weekend and holiday customer usage pattern.

AUF met with several customer representatives, described the flushing protocol, and followed up with these representatives, as requested, when flushing occurred. AUF has continued the systematic flushing plan, which it believes is the most cost-effective solution for the Rosalie Oaks system.

Tangerine (Orange County)

The Tangerine water system, with approximately 277 customers, has naturally occurring iron, hydrogen sulfide, calcium, and sediment in the water. AUF met with customer representatives and described a process for sequestering the iron in the water as well as a looping project, which had previously been designed, permitted, and installed, to address the iron and hardness of the water. Water main extensions were installed to connect dead ends, diminish pressure problems, give the water a “softer” taste, and remove sediment. According to AUF, the customer representatives seemed satisfied with the Utility’s actions. In addition, in response to one of the customer representatives, AUF installed a fire hydrant in the customer’s vicinity.

Tomoka View (Volusia County)

Hydrogen sulfide, calcium, and sediment have created taste and odor concerns for many of the 190 customers of the Tomoka View system. The system also experienced a primary water quality issue involving TTHMs. In response to a Consent Order, AUF constructed a chloramination system that was placed into service, and a flushing program was implemented. AUF was required to sample monthly for TTHMs; and, after achieving six consecutive monthly samples for TTHMs below the MCL and maintaining a running annual average below the MCL, the Consent Order was closed.

According to AUF, Tomoka View customer representatives were satisfied that the TTHM issue was resolved and that the water quality had improved since additional treatment and flushing programs were initiated. Customers expressed concerns about dark rings in toilet bowls and pink film in shower stalls and bath tubs. AUF explained that the rings and film were related to airborne bacteria, not poor water quality.

A temporary nitrification issue that occurred in July 2010 was also discussed with customer representatives. Nitrification occurs in drinking water systems that use chloramines as a means of disinfection. AUF noticed its customers, then converted from chloramines to free chlorine for disinfection for 30 days and directionally flushed its lines. After additional customer notification, the disinfection process was converted back to chloramines, and the distribution system has not had any subsequent nitrification issues. AUF is planning to convert to free chlorine again in June 2011 for 30 days as a preventative measure.

Zephyr Shores (Pasco County)

The Zephyr Shores system serves approximately 506 water customers. The raw water contains manganese, calcium, iron, and sediment, which results in aesthetic issues related to color, hardness, and turbidity. AUF met with customer representatives who expressed concerns about the Utility’s rates. The customers also expressed a desire for their system to be taken over by either the Florida Governmental Utility Authority or Pasco County. AUF designed, permitted, and installed a sequestering system and installed valves and flushing hydrants. In response to customer concerns regarding water pressure, several alternatives and the associated costs were considered, including installing a water main through an easement between two properties or installing the main along the roadway. According to AUF, the main along the roadway is being designed, and the Utility is preparing to meet with the homeowners association board to discuss easements. AUF did not provide a response regarding the request for it to sell its facilities.

Additional AUF Water and Wastewater System Improvements

AUF provided documentation in its application and in response to discovery identifying completed and proposed system improvements. The improvements are designed to repair and upgrade existing facilities to address compliance issues and to improve systems where customers have reported concerns about aesthetic issues, such as the pressure, taste, odor, and color of the water. All customer meters have been replaced with remote read meters. Improvements have been proposed or made at many AUF water treatment plants to update the treatment processes to address TTHMs, remove sulfur, sequester iron, and replace and upgrade hydropneumatic and storage tanks to address water pressure and supply issues. Several water distribution systems were improved by replacing undersized mains and installing flushing valves to address taste, odor, and pressure issues. Fire hydrants were also replaced in several systems.

AUF upgraded the wastewater treatment and disposal facilities at several systems and proposed improvements at others. The improvements address general maintenance, as well as compliance issues. Projects related to infiltration and inflow issues were proposed. In addition, the collection systems were upgraded.

YES’ April 11, 2011, Memorandum

In its April 11, 2011 Memorandum, YES indicated that the value of the quality of service provided by AUF to Arredondo Farms is unsatisfactory and inconsistent with the standards and norms of the local community. Arredondo Farms was not included in the Joint Secondary Water Quality Task Force. The Memorandum describes the customers’ dissatisfaction with respect to the color, odor, and taste of the water and the high levels of calcium and other minerals that degrade plumbing fixtures and appliances. According to YES, calcium carbonate, when heated (such as in a water heater or in small appliances), solidifies and destroys plumbing fixtures and appliances. They believe that AUF has not only failed to meet its statutory obligations, but also has failed to meet the spirit of the Monitoring Plan that was a condition set by the Commission.

In AUF’s April 28, 2011, response to YES’ Memorandum, the Utility asserts that the quality of service to the Arredondo Farms’ systems is satisfactory. AUF acknowledges that the system experiences hard water; however, no MCL has been established by DEP for hardness. Further, AUF states that this hard water is not exceptionally hard for Florida. The Utility references a 1996 rate case involving the system in which the Commission found that, while the water at the system was hard, it did not present a health hazard.[20]

The water system is in compliance with all applicable DEP primary and secondary water quality standards. Although Arredondo Farms was not included in the seven systems chosen for the Joint Secondary Water Quality Task Force, AUF states that it was placed in the next tier of systems to be addressed in the second phase of its aesthetic water quality program, which will also include the Hermit’s Cove, River Grove, and Arredondo Estates systems. Staff believes that AUF is appropriately addressing the customers’ concerns with regard to aesthetic water quality at Arredondo Farms.

In its April 11, 2011, Memorandum, YES also claims that AUF has poor billing practices. It asserts that AUF presents incorrect bills as a result of the Utility’s meter equipment and a lack of review or supervision to detect obvious billing errors. YES also finds fault in the way AUF handles backbilling in instances in which customers have not been billed for some period of time. In addition, YES submitted examples of customer billing errors.