Changes in appearance and in display of formulas, tables, and text may have occurred during translation of this document into an electronic medium. This HTML document may not be an accurate version of the official document and should not be relied on.

For an official paper copy, contact the Florida Public Service Commission at contact@psc.state.fl.us or call (850) 413-6770. There may be a charge for the copy.

|

|

|

||

|

DATE: |

|||

|

TO: |

Office of Commission Clerk (Stauffer) |

||

|

FROM: |

Office of the General Counsel (Page) Division of Economics (Higgins, McNulty, Ollila, Rome, Wu) |

||

|

RE: |

|||

|

AGENDA: |

03/01/16 – Regular Agenda –Rule Proposal - Interested Persons May Participate |

||

|

COMMISSIONERS ASSIGNED: |

|||

|

PREHEARING OFFICER: |

|||

|

SPECIAL INSTRUCTIONS: |

|||

Rules 25-6.0436, Depreciation, and 25-6.04364, Electric Utilities Dismantlement Studies, Florida Administrative Code (F.A.C.), set forth accounting principles for the calculation of depreciation by electric utilities. Rules 25-7.045, F.A.C., Depreciation, and 25-7.046, F.A.C., Subcategories of Gas Plant for Depreciation, establish the accounting principles for the calculation of depreciation by gas utilities. The rules implement Section 366.06(1), Florida Statutes, (F.S.), which states that the Commission shall have authority to investigate and determine the actual legitimate costs of the property of each utility less depreciation.

The Commission’s Notice of Development of Rulemaking was published in the Florida Administrative Register (F.A.R.), on April 30, 2015, in Volume 41, Number 84. On May 22, 2015, May 29, 2015, and July 7, 2015, respectively, comments were received from Tampa Electric Company (TECO), Peoples Gas, Florida Public Utilities Company, and Florida Power & Light Company (FPL). No rulemaking workshop was requested and no workshop was held.

This recommendation addresses whether the Commission should propose the amendment of electric and gas utility depreciation Rules 25-6.0436, 25-6.04364, 25-7.045, and 25-7.046, F.A.C. The Commission has jurisdiction pursuant to Sections 120.54 and 366.06(1), F.S.

Issue 1:

Should the Commission propose the amendment of Rules 25-6.0436, 25-6.04364, 25-7.045, and 25-7.046, F.A.C.?

Recommendation:

Yes. The Commission should propose the amendment of Rules 25-6.0436, 25-6.04364, 25-7.045, and 25-7.046, F.A.C., as set forth in Attachment A. (Page, Ollila, Higgins, McNulty, Rome, Wu)

Staff Analysis:

This rulemaking was initiated to update, clarify, and streamline Commission depreciation rules for investor-owned electric utilities and gas utilities, and to provide more consistency between the electric depreciation and gas depreciation rules. Staff is recommending that the Commission propose the amendment of the rules, as set forth in Attachment A. Below is a more detailed explanation of the rule amendments staff is recommending.

Electric Utilities

Rule 25-6.0436, F.A.C., Depreciation

Rule 25-6.0436, F.A.C., provides definitions of depreciation terms and describes the requirements for categories of depreciable plant, depreciation rate, and accounts and subaccounts. Subsection 25-6.0436(1), F.A.C., defines the terms used in calculating the remaining life and whole life depreciation rates for electric utilities. Staff recommends the amendment of subsection 25-6.0436(1), F.A.C., to clarify these terms.

Staff also recommends amendments to subsection 25-6.0436(4)(a), F.A.C., which requires each electric utility to file a depreciation study for Commission review at least once every four years from the submission date of the previous study. TECO, Peoples Gas, and FPL suggested that “unless otherwise required by the Commission,” be added to make clear that the Commission has the authority to require a depreciation study at a time set by the Commission. Staff agrees and recommends that “or pursuant to Commission order and within the time specified in the order” be added to subsection 25-6.0436(4)(a), F.A.C.

Subsection 25-6.0436(4)(a), F.A.C., states that electric utilities shall submit six copies of the information required for a depreciation study and at least three copies of the numerical data required when filing a depreciation study. Staff recommends amendments removing the requirement to file numerous copies of the information required in a depreciation study. Staff recommends that subsection 25-6.0436(4)(a), F.A.C., be amended to specify that depreciation studies shall be filed in electronic format. The electronic filing requirement is consistent with the Commission’s requirement for electronic filings. Staff also recommends amendments stating that annual depreciation status reports shall be provided in electronic format for subsection 25-6.0436(9), F.A.C. The electronic filing requirement updates subsection 25-6.0436(9), F.A.C., and reflects the current Commission practice to require electronic filings.

Staff recommends amendments to 25-6.0436(5)(a), F.A.C., specifying that components of a depreciation study shall include average service life, age, curve shape, net salvage, and average remaining life. Staff recommends amendments to subsection 25-6.0436(5)(b), F.A.C., stating that a depreciation study shall also include a comparison of current and annual depreciation rates and expenses.

Subsection 25-6.0436(3)(a), F.A.C., references subsection 25-6.014(1), F.A.C., but does not directly refer to the Uniform System of Accounts (USOA). Staff recommends a specific reference to the USOA in the subsection stating that the USOA is incorporated by reference in subsection 25-6.014(1), F.A.C.

Rule 25-6.04364, F.A.C., Electric Utilities Dismantlement Studies

Rule 25-6.04364, F.A.C., states that each utility owning a fossil fuel generating unit is required to establish a dismantlement accrual as approved by the Commission to accumulate a reserve that is sufficient to meet all expenses at the time of dismantlement. Staff recommends the deletion of the phrase “fossil fuel” so that Rule 25-6.04364(1), F.A.C., may encompass other forms of electric generation such as certain renewable generating facilities. Language was also added to the rule to indicate that Rule 25-6.04364, F.A.C., is not applicable to nuclear generating plants which are addressed in Rule 25-6.04365, F.A.C.

Subsection 25-6.04364(3), F.A.C., states that each electric utility shall file a dismantlement study for each generating site once every four years from the submission date of the previous study. Staff recommends that “or pursuant to Commission order and within the time specified in the order,” be added to the rule. This amendment makes clear that the Commission has the authority to require a depreciation study at a time set by the Commission. This amendment also makes the language in section 25-6.04364(3), F.A.C., similar to that recommended for Rule 25-6.0436(4)(a), F.A.C.

Gas Utilities

Rule 25-7.045, Depreciation

Section 25-7.045(1), F.A.C., does not contain a definition of the term, “Net Book Value,” and staff recommends defining this term in subsection 25-7.045(1)(d), F.A.C. Rule 25-7.045(1), F.A.C., does not contain a definition of “Reserve,” and staff recommends the inclusion of this definition in subsection 25-7.045(1)(f), F.A.C.

Subsection 25-7.045(4)(a), F.A.C., states that each gas utility shall file a depreciation study for Commission review at least once every five years from the submission date of the previous study. Staff recommends that subsection 25-7.045(4)(a), F.A.C., be amended to state “or pursuant to Commission order and within the time specified in the order,” acknowledging the Commission’s authority to require such a depreciation study at any time set by the Commission.

Subsection 25-7.045(4)(a), F.A.C., states that electric utilities shall submit six copies of the information required for a depreciation study and at least three copies of the numerical data required when filing a depreciation study. Staff recommends amendments removing the requirement to file numerous copies of the information required in a depreciation study. Staff recommends that subsection 25-7.045(4)(a), F.A.C., be amended to specify that depreciation studies shall be filed in electronic format. The electronic filing requirement is consistent with the Commission’s requirement for electronic filings.

Staff recommends amendments to subsection 25-7.045(9), F.A.C., stating that annual depreciation status reports shall be provided in electronic format. This electronic filing requirement updates Rule 25-7.045, F.A.C., and reflects the current Commission practice to require electronic filings.

Staff recommends amendments to Rule 25-7.045, F.A.C., which would add subsection 25-7.045(2)(c), F.A.C., setting forth the appropriate parameters for the calculation of depreciation reserve when plant investments are booked as a transfer. Staff recommends adding these parameters in subsection 25-7.045(2)(c), F.A.C., to clarify the required elements for the comparison.

Staff recommends amendments to subsections 25-7.045(5)(a) and (b), F.A.C., to clarify requirements for a comparison of current and proposed annual depreciation rates and the criteria for such a comparison. These amendments will also make Rule 25-7.045(5)(a), F.A.C., consistent with subsections 25-6.0436(5)(a) and (c), F.A.C.

Subsection 25-7.045(3)(a), F.A.C., references subsection 25-7.014, F.A.C., but does not directly refer to the USOA. Staff recommends a specific reference to the USOA in the subsection stating that the USOA is incorporated by reference in subsection 25-7.014(1), F.A.C.

Rule 25-7.046, Subcategories of Gas Plant for Depreciation

Rule 25-7.046, F.A.C., states that depreciation accounts for gas utilities, as listed in the rule, follow the primary plant accounts established by the USOA prescribed by the Federal Energy Regulatory Commission in the Code of Federal Regulations, revised April 1, 1981. Staff recommends an amendment to Rule 25-7.046, F.A.C., to reflect that the USOA for Natural Gas Companies as found in the Code of Federal Regulations is incorporated by reference in Rule 25-7.014, F.A.C., Records and Reports in General.

Staff recommends that “shall” be substituted for “should” making all sub-accounts prescribed by the rule mandatory when calculating depreciation. Staff also recommends that paragraph 25-7.046(4)(c), F.A.C., be amended to remove discretionary language and state that where any existing accounts are compatible with those listed in subsection (3) for depreciation purposes, those existing accounts shall be deemed to be in compliance with Rule 25-7.046, F.A.C.

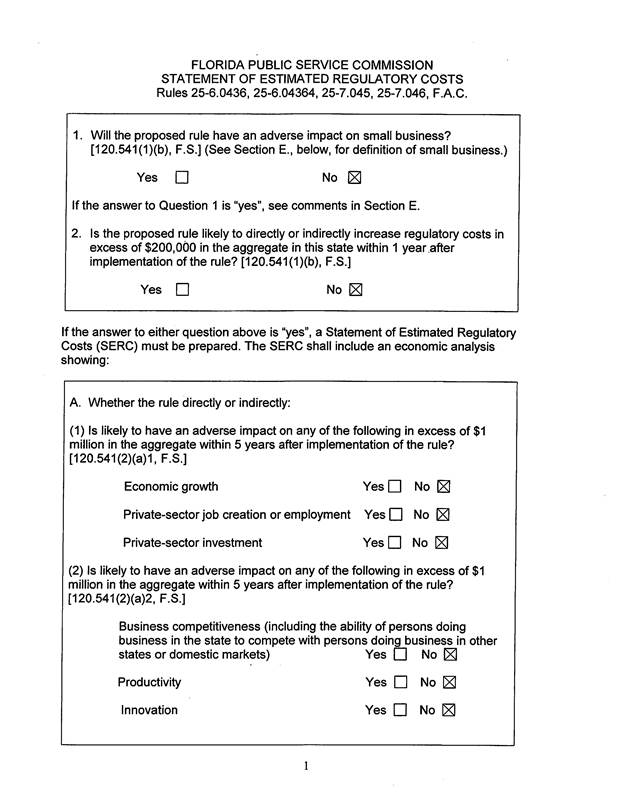

Statement of Estimated Regulatory Costs

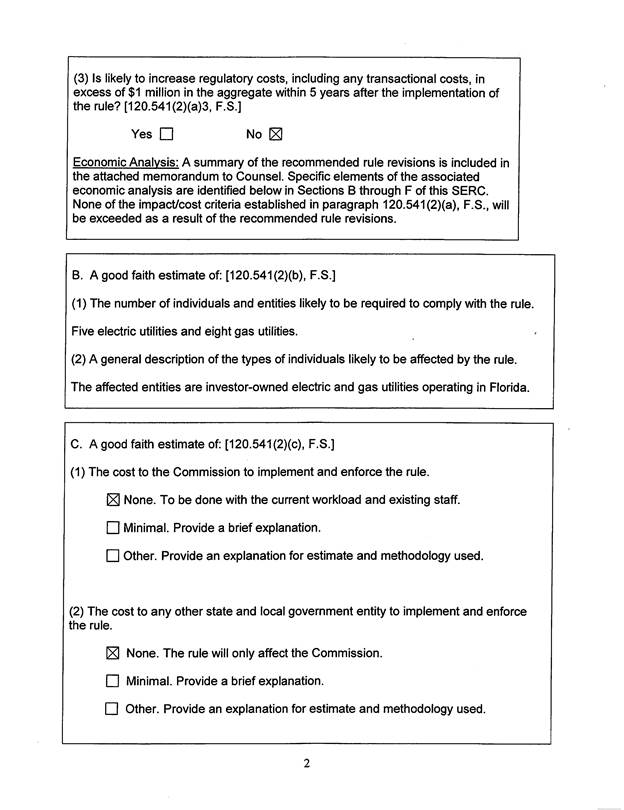

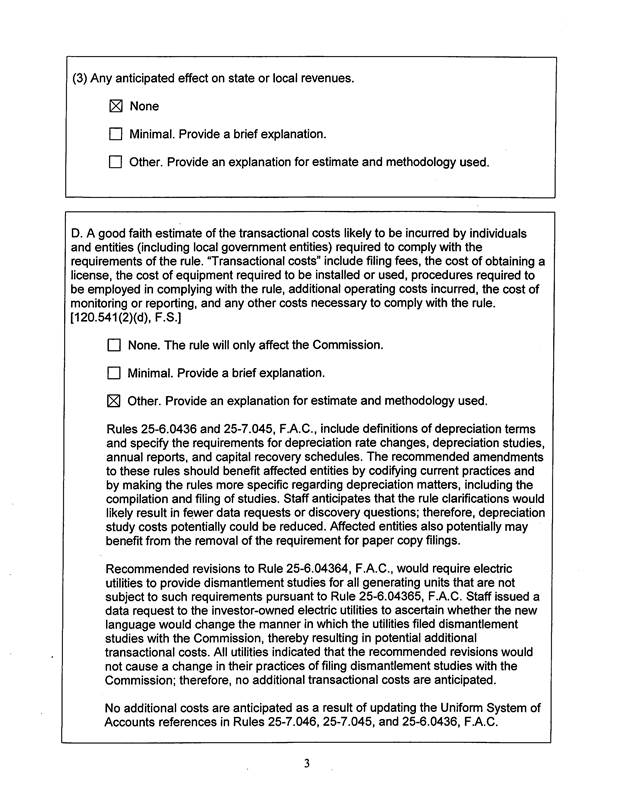

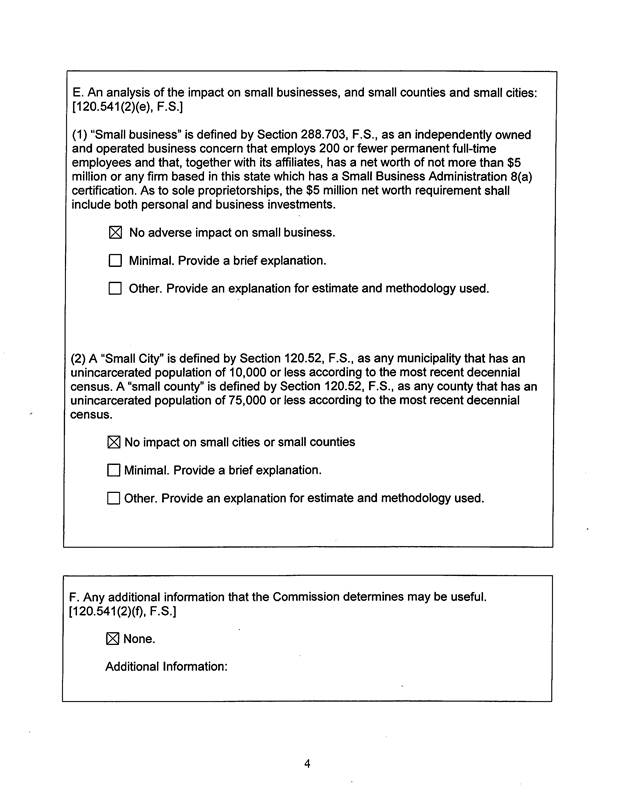

Pursuant to Section 120.54, F.S., agencies are encouraged to prepare a statement of estimated regulatory costs (SERC) before the adoption, amendment, or repeal of any rule. The SERC is appended as Attachment B to this recommendation. The SERC analysis also includes whether the rule amendment is likely to have an adverse impact on growth, private sector job creation or employment, or private sector investment in excess of $1 million in the aggregate within five years after implementation.

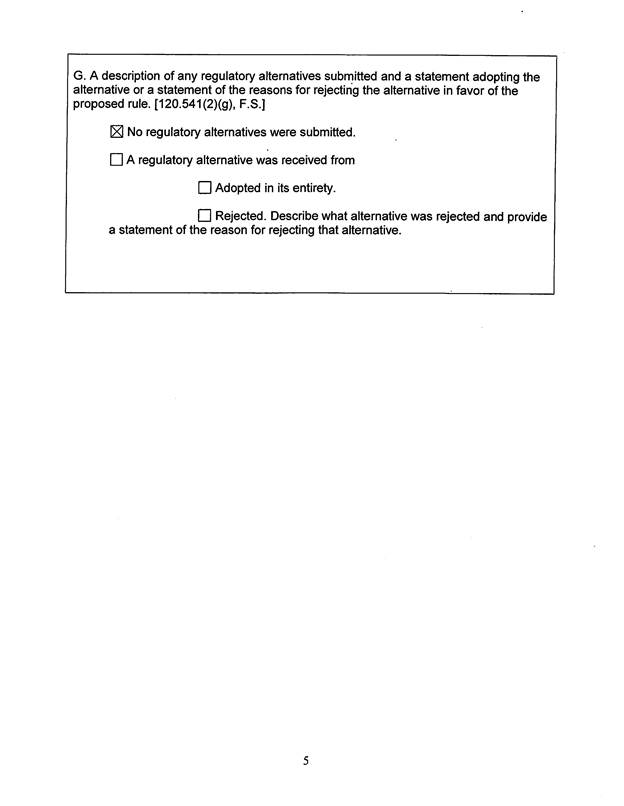

The SERC concludes that the rule amendments will not likely directly or indirectly increase regulatory costs in excess of $200,000 in the aggregate in Florida within one year after implementation. Further, the SERC concludes that the rule amendments will not likely have an adverse impact on economic growth, private-sector job creation or employment, private sector investment, business competitiveness, productivity, or innovation in excess of $1 million in the aggregate within five years of implementation. Thus, the rule amendments do not require legislative ratification pursuant to Section 120.541(3), F.S. In addition, the SERC states that the rule amendments will not have an adverse impact on small business and will have no impact on small cities or small counties. No regulatory alternatives were submitted pursuant to paragraph 120.541(1)(a), F.S. None of the impact/cost criteria established in paragraph 120.541(2)(a), F.S., will be exceeded as a result of the recommended revisions.

Conclusion

Based on the foregoing, staff recommends the amendment of Rules 25-6.0436, 25-6.04364, 25-7.045, and 25-7.046, F.A.C.

Issue 2:

Should this docket be closed?

Recommendation:

Yes. If no requests for hearing or comments are filed, the rules may be filed with the Department of State, and this docket should be closed. (Page)

Staff Analysis:

If no requests for hearing or comments are filed, the rules may be filed with the Department of State, and this docket should be closed.

25-6.0436 Depreciation.

(1) For the purposes of this rule part, the

following definitions shall apply:

(a) Category or Category of Depreciable Plant – A grouping

of plant for which a depreciation rate is prescribed. At a minimum it shall

should include each plant account prescribed in subsection 25-6.014(1),

F.A.C.

(b) Embedded Vintage – A vintage of plant in service as of the date of study or implementation of proposed rates.

(c) Mortality Data – Historical data by study category

showing plant balances, additions, adjustments and retirements, used in

analyses for life indications or calculations of realized life. Preferably,

Tthis is aged data in accord with the following:

1. The number of plant items or equivalent units (usually expressed in dollars) added each calendar year.

2. The number of plant items retired (usually expressed in dollars) each year and the distribution by years of placing of such retirements.

3. The net increase or decrease resulting from purchases, sales or adjustments and the distribution by years of placing of such amounts.

4. The number that remains in service (usually expressed in dollars) at the end of each year and the distribution by years of placing of such amounts.

(d) Net Book Value – The book cost of an asset or group of assets minus the accumulated depreciation or amortization reserve associated with those assets.

(e) Remaining Life Technique Method – The

method of calculating a depreciation rate based on the unrecovered plant

balance, the less average future net salvage, and the

average remaining life. The formula for calculating a Remaining Life Rate

is:

|

|

Remaining Life Rate |

= |

100% - Reserve % - Average Future Net Salvage % __________________________________ Average Remaining Life in Years |

(f) Reserve (Accumulated Depreciation) – The amount of depreciation/amortization expense, salvage, cost of removal, adjustments, transfers, and reclassifications accumulated to date.

(g) Reserve Data – Historical data by study category showing reserve balances, debits and credits such as booked depreciation, expense, salvage and cost of removal and adjustments to the reserve utilized in monitoring reserve activity and position.

(h) Reserve Deficiency – An inadequacy in the reserve of a category as evidenced by a comparison of that reserve indicated as necessary under current projections of life and salvage with that reserve historically accrued. The latter figure may be available from the utility’s records or may require retrospective calculation.

(i) Reserve Surplus – An excess in the reserve of a category as evidenced by a comparison of that reserve indicated as necessary under current projections of life and salvage with that reserve historically accrued. The latter figure may be available from the utility’s records or may require retrospective calculation.

(j) Salvage Data – Historical data by study category showing bookings of retirements, gross salvage and cost of removal used in analysis of trends in gross salvage and cost of removal or for calculations of realized salvage.

(k) Theoretical Reserve or Prospective Theoretical Reserve – A calculated reserve based on components of the proposed rate using the formula:

Theoretical Reserve = Book Investment - Future Accruals - Future Net Salvage

(l) Vintage – The year of placement of a group of plant items or investment under study.

(m) Whole Life Technique Method – The method of

calculating a depreciation rate based on the wWhole lLife

(aAverage sService lLife) and the aAverage

nNet sSalvage. Both life and salvage components are

the estimated or calculated composite of realized experience and expected

activity. The formula is:

|

|

Whole Life Rate |

= |

100% - Average Net Salvage % __________________________ Average Service Life in Years |

(2)(a) No utility shall change any existing depreciation rate or initiate any new depreciation rate without prior Commission approval.

(b) No utility shall reallocate accumulated depreciation reserves among any primary accounts and sub-accounts without prior Commission approval.

(c) When plant investment is booked as a transfer from a

regulated utility depreciable account to another or from a regulated company to

an affiliate, its associated an appropriate reserve amount shall

also be booked as a transfer. When plant investment is sold from one regulated

utility to an affiliate, the an appropriate associated reserve

amount shall also be determined to calculate the net book value of the utility

investment being sold. Appropriate Mmethods for

determining the appropriate reserve amount associated with plant

transferred or sold are as follows:

1. Where vintage reserves are not maintained,

synthetization using the currently prescribed curve shape shall may

be required. The same reserve percent associated with the original placement

vintage of the related investment shall then be used in determining the appropriate

amount of reserve to transfer.

2. Where the original placement vintage of the investment

being transferred is unknown, the reserve percent applicable to the account in

which the investment being transferred resides may be assumed as appropriate

for determining the reserve amount to transfer.

3. Where the age of the investment being transferred is known and a history of the prescribed depreciation rates is known, a reserve can be determined by multiplying the age times the investment times the applicable depreciation rate(s).

4. The Commission shall consider any additional methods

submitted by the utilities for determining the appropriate reserve

amounts to transfer.

(3)(a) Each utility shall maintain depreciation rates and

accumulated depreciation reserves in accounts or subaccounts

in accordance

with the Uniform System of Accounts for

Public

Utilities and Licensees as found in the Code of Federal Regulations, Title 18,

Subchapter C, Part 101, for Major Utilities as revised

April 1, 2013,

which is incorporated by reference in Rule 25-6.014, F.A.C.

as

prescribed by subsection 25-6.014(1), F.A.C.

Utilities may maintain further

sub-categorization.

(b) Upon establishing a new account or subaccount

classification, each utility shall request Commission approval of a

depreciation rate for the new plant category.

(4)

(a) Each company shall file a depreciation study for

each category of depreciable property for Commission review at least once every

four years from the submission date of the previous study or pursuant to

Commission order and within the time specified in the order.

A utility

filing a depreciation study, regardless if a change in rates is being requested

or not, shall submit to the Office of Commission Clerk six copies of

the information required by paragraphs (5)(6)(a) through (g)(f)

of this rule in electronic format with formulas intact and unlocked

and

at least

three

copies of the information required by paragraph

(6)(g)

.

(b) A utility proposing an effective date of the beginning of its fiscal year shall submit its depreciation study no later than the mid-point of that fiscal year.

(c) A utility proposing an effective date coinciding with the expected date of a revenue change initiated through a rate case proceeding shall submit its depreciation study no later than the filing date of its Minimum Filing Requirements.

(d) The plant balances may include estimates. Submitted data including plant and reserve balances or company planning involving estimates shall be brought to the effective date of the proposed rates.

(e) The possibility of corrective reserve transfers shall be investigated by the Commission prior to changing depreciation rates.

(f)(5) Upon Commission approval by final

order establishing an effective date, the utility shall reflect on its books

and records the implementation of the depreciation proposed rates

approved by the Commission

subject to adjustment when final

depreciation rates are approved

.

(5)(6) A depreciation study shall include:

(a) A comparison of current and proposed depreciation

rates

and

components for each category of depreciable plant.

Components include

average service life, age, curve shape, net salvage, and average remaining

life.

Current rates shall be identified as to the effective date and

proposed rates as to the proposed effective date.

(b) A comparison of current and proposed annual depreciation

rates and expenses

as of the proposed effective date, resulting

from current rates with those produced by the proposed rates for each category

of depreciable plant

.

The comparison of current and proposed rates

shall identify the proposed effective date for the proposed rates. The

comparison of current and proposed annual expenses shall be calculated using

current and proposed rates for each category of depreciable plant. Plant balances,

reserve balances and percentages, remaining lives, and net salvage percentages

shall be included in this comparison for each category of plant.

The

plant balances may involve estimates. Submitted data including plant and

reserve balances or company planning involving estimates shall be brought to

the effective date of the proposed rates.

(c) Each recovery and amortization schedule currently in

effect shall should be included with any new filing showing total

amount amortized, effective date, length of schedule, annual amount amortized

and reason for the schedule.

(d) A comparison of the accumulated book reserve to the prospective theoretical reserve based on proposed rates and components for each category of depreciable plant to which depreciation rates are to be applied.

(e) A general narrative describing the service environment of the applicant company and the factors, e.g., growth, technology, physical conditions, necessitating a revision in rates.

(f) An explanation and justification for each study

category of depreciable plant defining the specific factors that justify the

life and salvage components and rates being proposed. Each explanation and

justification shall include substantiating factors utilized by the utility in

the design of depreciation rates for the specific category, e.g., company

planning, growth, technology, physical conditions, trends. The explanation and

justification shall discuss any proposed transfers of reserve between

categories or accounts intended to correct deficient or surplus reserve

balances. It shall should also state any statistical or

mathematical methods of analysis or calculation used in design of the category

rate.

(g) The filing shall contain Aall calculations,

analysis and numerical basic data used in the design of the depreciation rate

for each category of depreciable plant. Numerical data shall include plant

activity (gross additions, adjustments, retirements, and plant balance at end

of year) as well as reserve activity (retirements, accruals for depreciation

expense, salvage, cost of removal, adjustments, transfers and reclassifications

and reserve balance at end of year) for each year of activity from the date of

the last submitted study to the date of the present study. When available,

To the degree possible, retirement data involving retirements

shall should be aged.

(h) The mortality and salvage data used by the company in the depreciation rate design must agree with activity booked by the utility. Unusual transactions not included in life or salvage studies, e.g., sales or extraordinary retirements, must be specifically enumerated and explained.

(i)(7)(a) Utilities shall provide Ccalculations

of depreciation rates using both the whole life technique method

and the remaining life technique method. The use of these techniques

methods is required for all depreciable categories. Utilities may submit

additional studies or methods for consideration by the Commission.

(b) The possibility of corrective reserve transfers

shall be investigated by the Commission prior to changing depreciation rates.

(8)(a) Each company shall file a study for each category

of depreciable property for Commission review at least once every four years

from the submission date of the previous study unless otherwise required by the

Commission.

(b) A utility proposing an effective date of the

beginning of its fiscal year shall submit its depreciation study no later than

the mid-point of that fiscal year.

(c) A utility proposing an effective date coinciding

with the expected date of additional revenues initiated through a rate case

proceeding shall submit its depreciation study no later than the filing date of

its Minimum Filing Requirements.

(6)(9) As part of the filing of the annual

report pursuant to Rule 25-6.135, F.A.C., each utility shall include an annual depreciation

status report. The annual depreciation status reports

shall be

provided in electronic format. In the electronic format, the formulas must be

intact and unlocked.

The annual depreciation status report shall

include booked plant activity (plant balance at the beginning of the year,

additions, adjustments, transfers, reclassifications, retirements and plant

balance at year end) and reserve activity (reserve balance at the beginning of

the year, retirements, accruals, salvage, cost of removal, adjustments,

transfers, reclassifications and reserve balance at year end) for each category

of investment for which a depreciation rate, amortization, or capital recovery

schedule has been approved. The report shall indicate for each category that:

whether there has been a change of plans or utility experience since the

filing of the last annual depreciation status report requiring a revision of

rates, amortization or capital recovery schedules. For any category where

current conditions indicate a need for revision of depreciation rates,

amortization, or capital recovery schedules and no revision is sought, the

report shall explain why no revision is requested.

(a) There has been no change of plans or utility

experience requiring a revision of rates, amortization or capital recovery

schedules; or

(b) There has been a change requiring a revision of

rates, amortization or capital recovery schedules.

(7)

(10) For any category where current conditions

indicate a need for revision of depreciation rates, amortization or capital

recovery schedules and no revision is sought, the report shall explain why no

revision is requested.

(a) Prior to the date of retirement of major installations, the Commission shall approve capital recovery schedules to correct associated calculated deficiencies where a utility demonstrates that (1) replacement of an installation or group of installations is prudent and (2) the associated investment will not be recovered by the time of retirement through the normal depreciation process.

(b) The Commission shall approve a special capital recovery schedule when an installation is designed for a specific purpose or for a limited duration.

(c) Associated plant and reserve activity, balances and the annual capital recovery schedule expense must be maintained as subsidiary records.

Rulemaking Authority 350.115, 350.127(2), 366.05(1), FS. Law Implemented 350.115, 366.04(2)(f), 366.06(1) FS. History–New 11-11-82, Amended 1-6-85, Formerly 25-6.436, Amended 4-27-88, 12-12-91, 12-11-00, 5-29-08, _____________.

25-6.04364 Electric Utilities Dismantlement Studies.

(1) Each utility that owns a fossil fuel generating

unit is required to establish a dismantlement accrual as approved by the

Commission to accumulate a reserve that is sufficient to meet all

expenses at the time of dismantlement. The purpose of the study required by

subsection (3) is to obtain sufficient information to update cost

estimates based on new developments, additional information, technological

improvements, and forecasts; to evaluate alternative methodologies; and to

revise the annual accrual needed to recover the costs. This

rule does

not apply to nuclear generating plants, which are addressed in Rule 25-6.04365,

F.A.C.

(2) For the purpose of this rule, the following definitions shall apply:

(a) “Contingency Costs.” A specific provision for unforeseeable elements of cost within the defined project scope.

(b) “Dismantlement.” The process of safely managing,

removing, demolishing, disposing, or converting for reuse the materials and

equipment that remain at the fossil fuel generating unit following its

retirement from service and restoring the site to a marketable or useable

condition.

(c) “Dismantlement Costs.” The costs for the ultimate physical removal and disposal of plant and site restoration, minus any attendant gross salvage amount, upon final retirement of the site or unit from service.

(3) Each utility shall file a dismantlement study for each

generating site once every 4 years from the submission date of the previous

study or pursuant to unless otherwise required by Commission order.

and within the time specified in the order. The study shall be

site-specific unless a showing is made by the utility that a site-specific

study is not possible. A utility may file a study sooner than 4 years. Each

utility’s dismantlement study shall include:

(a) A narrative describing each fossil fuel

generating unit, including the in-service date and estimated retirement date.

(b) A list of all entities owning an interest in each generating unit and the percentage of ownership by each entity.

(c) The dismantlement study methodology.

(d) A summary of the major assumptions used in the study.

(e) The methodology selected to dismantle each generating unit and support for the selection.

(f) The methodology and escalation rates used in converting the current estimated dismantlement costs to future estimated dismantlement costs and supporting documentation and analyses.

(g) The total utility and jurisdictional dismantlement cost estimates in current dollars for each unit.

(h) The total utility and jurisdictional dismantlement cost estimates in future dollars for each unit.

(i) For each year, the estimated amount of dismantlement expenditures.

(j) The projected date each generating unit will cease operations.

(k) For each site, a comparison of the current approved annual dismantlement accruals with those proposed. Current accruals shall be identified as to the effective date and proposed accruals to the proposed effective date.

(l) A summary and explanation of material differences between the current study and the utility’s last filed study including changes in methodology and assumptions.

(m) Supporting schedules, analyses, and data, including the contingency allowance, used in developing the dismantlement cost estimates and annual accruals proposed by the utility. Supporting schedules shall include the inflation analysis.

(4) The dismantlement annual accrual shall be calculated using the current cost estimates escalated to the expected dates of actual dismantlement. The future costs less amounts recovered to date shall then be discounted in a manner that accrues the costs over the remaining life span of the unit.

(5) Dismantlement accruals shall be recorded monthly to assure that the costs for dismantlement have been provided for at the time the production unit or site ceases operations.

(6) A utility shall not establish a new annual dismantlement accrual, revise its annual dismantlement accrual, or transfer a dismantlement reserve without prior Commission approval.

(7) The annual dismantlement accrual shall be a fixed dollar amount and shall be based on a 4-year average of the accruals related to the years between the dismantlement study reviews.

(8) The accumulated dismantlement reserve and accruals shall be maintained in a subaccount of Account 108 “Accumulated Depreciation” and separate from the accumulated depreciation reserve and expenses. Subsidiary records shall include sufficient detail to allow for separate site or unit reporting.

Rulemaking Authority 350.115, 350.127(2), 366.05(1) FS. Law Implemented 366.041, 366.05(1), 366.06(1) FS. History–New 12-30-03, Amended _____________.

25-7.045 Depreciation.

(1) For the purpose of this rule part, the

following definitions shall apply:

(a) Category or Category of Depreciable Plant – A grouping

of plant for which a depreciation rate is prescribed. At a minimum it shall

should include each plant account prescribed in Rule 25-7.046, F.A.C.

(b) Embedded Vintage – A vintage of plant in service as of the date of study or implementation of proposed rates.

(c) Mortality Data – Historical data by study category

showing plant balances, additions, adjustments and retirements, used in

analyses for life indications or for calculations of realized life. Preferably

Tthis is aged data in accord with the following:

1. The number of plant items or equivalent units (usually expressed in dollars) added each calendar year.

2. The number of plant items retired (usually expressed in dollars) each year and the distribution by years of placing of such retirements.

3. The net increase or decrease resulting from purchases, sales or adjustments and the distribution by years of placing of such amounts.

4. The number that remains in service (usually expressed in dollars) at the end of each year and the distribution by years of placing of such amounts.

(d) Net Book Value - The book cost of an asset or group of assets minus the accumulated depreciation or amortization reserve associated with those assets.

(e)(d) Remaining Life Technique Method

– The method of calculating a depreciation rate based on the unrecovered plant

balance, the less average future net salvage and the average

remaining life. The formula for calculating a Remaining Life Rate is:

Remaining Life Rate = 100% - Reserve % - Average Future Net Salvage %

Average Remaining Life in Years

(f) Reserve (Accumulated Depreciation) – The amount of depreciation/amortization expense, salvage, cost of removal, adjustments, transfers, and reclassifications accumulated to date.

(g)(e) Reserve Data – Historical data by

study category showing reserve balances, debits and credits, such as booked

depreciation expense, salvage and cost of removal, and adjustments to the

reserve utilized in monitoring reserve activity and position.

(h)(f) Reserve Deficiency – An inadequacy in

the reserve of a category as evidenced by a comparison of that reserve

indicated as necessary under current projections of life and salvage with that

reserve historically accrued. The latter figure may be available from the

utility’s records or may require retrospective calculation.

(i)(g) Reserve Surplus – An excess in the

reserve of a category as evidenced by a comparison of that reserve indicated as

necessary under current projections of life and salvage with that reserve

historically accrued. The latter figure may be available from the utility’s

records or may require retrospective calculation.

(j)(h) Salvage Data – Historical data by

study category showing bookings of retirements, gross salvage and cost of

removal used in analysis of trends in gross salvage and cost of removal or for

calculations of realized salvage.

(k)(i) Theoretical Reserve or Prospective

Theoretical Reserve – A calculated reserve based on components of the proposed

rate using the formula:

Theoretical Reserve = Book Investment – Future Accruals – Future Net Salvage.

(l)(j) Vintage – The year of placement of a

group of plant items or investment under study.

(m)(k) Whole Life Technique Method

– The method of calculating a depreciation rate based on the wWhole

lLife (aAverage sService lLife)

and the aAverage nNet sSalvage. Both

life and salvage components are the estimated or calculated composite of

realized experience and expected activity. The formula is:

Whole Life Rate = 100% - Average Net Salvage %

Average Service Life in Years

(2)(a) No utility shall may change any

existing depreciation rate or initiate any new depreciation rate without prior

Commission approval.

(b) No utility shall may reallocate

accumulated depreciation reserves among any primary accounts and sub-accounts

without prior Commission approval.

(c) When plant investment is booked as a transfer from a regulated utility depreciable account to another or from a regulated company to an affiliate, its associated reserve amount shall also be booked as a transfer. When plant investment is sold from one regulated utility to an affiliate, the associated reserve amount shall also be determined to calculate the net book value of the utility investment being sold. Methods for determining the reserve amount associated with plant transferred or sold are as follows:

1. Where vintage reserves are not maintained, synthesization using the currently prescribed curve shape shall be required. The same reserve percent associated with the original placement vintage of the related investment shall then be used in determining the amount of reserve to transfer.

2. Where the original placement vintage of the investment being transferred is unknown, the reserve percent applicable to the account in which the investment being transferred resides shall be assumed for determining the reserve amount to transfer.

3. Where the age of the investment being transferred is known and a history of the prescribed depreciation rates is known, a reserve can be determined by multiplying the age times the investment times the applicable depreciation rate(s).

4. The Commission shall consider any additional methods submitted by the utilities for determining reserve amounts to transfer.

(3)(a) Each utility shall maintain depreciation rates and

accumulated depreciation reserves in accounts or subaccounts

in accordance

with the Uniform System of Accounts for Natural Gas Companies (USOA) as found

in the Code of Federal Regulations, Title 18, Subchapter F, Part 201, as

revised April 1, 2013, which is incorporated by reference in Rule 25-7.014(1),

F.A.C.

as prescribed by Rule 25-7.046, F.A.C. Utilities may

maintain further sub-categorization.

(b) Upon establishing a new account or subaccount classification, each utility shall request Commission approval of a depreciation rate for the new plant category.

(4)

(a) Each company shall file a study for each category

of depreciable property for Commission review at least once every five years

from the submission date of the previous study or pursuant to Commission order

and within the time specified in the order.

A utility filing a depreciation study, regardless if a change in rates is

being requested or not, shall submit to the Office of Commission Clerk six

copies of the information required by paragraphs (5)(6)(a)

through (g) (f) and (h) of this rule

in electronic format with

formulas intact and unlocked

and at

least three copies of the information required by paragraph (6)(g)

.

(b) A utility proposing an effective date of the beginning of its fiscal year shall submit its depreciation study no later than the mid-point of that fiscal year.

(c) A utility proposing an effective date coinciding with the expected date of additional revenues initiated through a rate case proceeding shall submit its depreciation study no later than the filing date of its Minimum Filing Requirements.

(d) The plant balances may include estimates. Submitted data including plant and reserve balances or company planning involving estimates shall be brought to the effective date of the proposed rates.

(e) The possibility of corrective reserve transfers shall be investigated by the Commission prior to changing depreciation rates.

(f)(5) Upon Commission approval by final

order establishing an effective date, the utility shall may

reflect on its books and records the implementation of the depreciation proposed

rates,approved by the Commission

subject to adjustment when

final depreciation rates are approved

.

(5)(6) A depreciation study shall include:

(a) A comparison of current and proposed depreciation

rates

and

components for each category of depreciable plant.

Components include

average service life, age, curve shape, net

salvage, and average remaining

life.

Current rates shall be identified as to the effective date and

proposed rates as to the proposed effective date.

(b) A comparison of current and proposed annual

depreciation rates and expenses

resulting from current rates

with those produced by the proposed rates for each category of depreciable

plant

.

The comparison of current and proposed rates shall identify the

proposed effective date for the proposed rates. The comparison of current and

proposed annual expenses shall be calculated using current and proposed rates

for each category of depreciable plant. Plant balances, reserve balances and

percentages, remaining lives, and net salvage percentages shall be included in

this comparison for each category of plant.

The plant balances may

involve estimates. Submitted data including plant and reserve balances or

company planning involving estimates should be brought to the effective date of

the proposed rates.

(c) Each recovery and amortization schedule currently in

effect shall should be included with any new filing showing total

amount amortized, effective date, length of schedule, annual amount amortized

and reason for the schedule.

(d) A comparison of the accumulated book reserve to the prospective theoretical reserve based on proposed rates and components for each category of depreciable plant to which depreciation rates are to be applied.

(e) A general narrative describing the service environment of the applicant company and the factors, e.g., growth, technology, physical conditions, leading to the present application for a revision in rates.

(f) An explanation and justification for each study

category of depreciable plant defining the specific factors that justify the

life and salvage components and rates being proposed. Each explanation and

justification shall include substantiating factors utilized by the utility in

the design of the depreciation rates for the specific category, e.g., company

planning, growth, technology, physical conditions, trends. The explanation and

justification shall discuss any proposed transfers of reserve between

categories or accounts intended to correct deficient or surplus reserve

balances. It shall should also state any statistical or

mathematical methods of analysis or calculation used in design of the category

rate.

(g) The filing shall contain Aall calculations,

analysis and numerical basic data used in the design of the depreciation rate

for each category of depreciable plant. Numerical data shall include plant

activity (gross additions, adjustments, retirements, and plant balance at end

of year) as well as reserve activity (retirements, accruals for depreciation

expense, salvage, cost of removal, adjustments, transfers and reclassifications

and reserve balance at end of year) for each year of activity from the date of

the last submitted study to the date of the present study. When available,

To the degree possible, retirement data involving retirements

shall should be aged.

(h) The mortality and salvage data used by the company in the depreciation rate design must agree with activity booked by the utility. Unusual transactions not included in life or salvage studies, e.g., sales or extraordinary retirements, must be specifically enumerated and explained.

(i)(7)(a) Utilities shall provide Ccalculations

of depreciation rates using both the whole life technique and the

remaining life technique method. The use of these techniques

methods is required for all depreciable categories. Utilities may submit

additional studies or methods for consideration by the Commission.

(b) The possibility of corrective reserve transfers

shall be investigated by the Commission prior to changing depreciation rates.

(8)(a) Each company shall file a study for each category

of depreciable property for Commission review at least once every five years

from the submission date of the previous study unless otherwise required by the

Commission.

(

b) A utility proposing an effective date of the

beginning of its fiscal year shall submit its depreciation study no later than

the mid-point of that fiscal year.

(c) A utility proposing an effective date coinciding

with the expected date of additional revenues initiated through a rate case

proceeding shall submit its depreciation study no later than the filing date of

its Minimum Filing Requirements.

(6)(9) As part of the filing of the annual

report under subsection 25-7.014(3), F.A.C., each utility shall include an

annual depreciation status report.

The annual depreciation status

report shall be provided in electronic format. In

the electronic format, the formulas must be intact and unlocked.

The

annual

depreciation status

report shall include booked plant activity (plant

balance at the beginning of the year, additions, adjustments, transfers,

reclassifications, retirements and plant balance at year end) and reserve

activity (reserve balance at the beginning of the year, retirements, accruals,

salvage, cost of removal, adjustments, transfers, reclassifications and reserve

balance at end of year) for each category of investment for which a

depreciation rate, amortization schedule, or capital recovery schedule has been

approved. The report shall indicate for each category that:

whether there

has been a change of plans or utility experience since the filing of the last

annual depreciation status report requiring a revision of the rates,

amortization, or capital recovery schedules. For any category where current

conditions indicate a need for revision of depreciation rates, amortization, or

capital recovery schedules and no revision is sought, the report shall explain

why no revision is requested.

(a) There has been no change of plans or utility

experience requiring a revision of the rates, amortization, or capital recovery

schedules; or

(b) There has been a change requiring a revision of

rates, amortization, or capital recovery schedules. For any category where

current conditions indicate a need for revision of depreciation rates,

amortization, or capital recovery schedules and no revision is sought, the

report shall explain why no revision is requested.

(7)(10)(a) Prior to the date of retirement of

major installations, the Commission may approve capital recovery schedules to

correct associated calculated deficiencies where a utility demonstrates that

(1) replacement of an installation or group of installations is prudent, and

(2) the associated investment will not be recovered by the time of retirement

through the normal depreciation process.

(b) The Commission shall may approve a

special capital recovery schedule when an installation is designed for a

specific purpose or for a limited duration.

(c) Associated plant and reserve activity, balances and the annual capital recovery schedule expense must be maintained as subsidiary records.

Rulemaking Authority 350.127(2), 350.115, 366.05(1) FS. Law Implemented 350.115, 366.04(2(f), 366.06, 366.06(1) FS. History–New 11-11-82, Amended 1-6-85, Formerly 25-7.45, Amended 4-27-88, 12-12-91, 5-29-08, ________.

25-7.046 Subcategories of Gas Plant for Depreciation.

(1) The accounts under subsection (3) below are to be used

in the design of depreciation rates. They are intended to group together items

which are relatively homogeneous in their expected life and salvage

characteristics. Reserve, mortality data, salvage and costs of removal shall

should be maintained accordingly for each depreciation category for which

a depreciation rate is to be applied. This shall should be done

on the books of the company, or as a side record for depreciation study use

only.

(2)(a) No company shall establish a new sub-account that would represent less than 10% of the original primary account unless it meets the following criteria:

1. Introduction of a new technology.

2. The present inclusion of an obsolescent/dying technology in a viable technology.

(b) Any company may further develop sub-accounts within the listed primary account as appropriate for its plant.

(3)

The depreciation accounts listed below shall be in

accordance with the Uniform System of Accounts for Natural Gas Companies (USOA)

as found in the Code of Federal Regulations, Title 18, Subchapter F, Part 201, as

revised April 1, 2013, which is incorporated by reference in Rule 25-7.014(1),

F.A.C. New depreciation subaccounts shall be established under these accounts

as listed in subsection 25-7.014(1), F.A.C.

The accounts listed

below directly follow the primary plant accounts prescribed in the Uniform

System of Accounts prescribed by the Federal Energy Regulatory Commission in

the Code of Federal Regulations, Title 18, Subchapter F, Part 201, as revised,

April 1, 1981, introducing sub-divisions within those accounts for the purpose

of uniformity among the companies in depreciation studies.

(a)I. Local Storage Plant.

1.A. Structures and Improvements – (Account

361)

2.B. Gas Holders – (Account 362)

3.C. Other – (Account 363) – Equipment such

as compressors, gauges and other instruments used in connection with the

storage of gas in holders.

(b)II. Distribution Plant.

1.A. Structures and Improvements – (Account

375)

2.B. Mains – (Account 376) – The following

sub-accounts shall should be used:

a.1. Plastic

b.2. Other – cast iron, steel, etc.

3.C. Compressor Station Equipment – (Account

377)

4.D. Measuring and Regulating Equipment –

General – (Account 378) – Equipment used in measuring and regulating gas in

connection with distribution systems other than the measurements of gas

deliveries to customers.

5.E. Measuring and Regulating Equipment –

City Gate – (Account 379) – Equipment used in measuring of gas at entry points

to distribution systems.

6.F. Services – (Account 380) – The following

sub-accounts shall should be used:

a.1. Plastic

b.2. Other – cast iron, steel, etc.

7.G. Meters – (Account 381)

8.H. Meter Installations – (Account 382)

9.I. Regulators – (Account 383)

10.J. Regulator Installations – (Account 384)

11.K. Industrial Measuring and Regulating

Equipment – (Account 385)

12.L. Other Property on Customer’s Premises –

(Account 386) – Investment of equipment owned by the company installed on the

customer’s premises that is not includible in other accounts.

13.M. Other Equipment – (Account 387) –

Investment in equipment used for the distribution system not included in any of

the above accounts such as fire protection equipment, leak detectors, pipe

locators. , etc.

(c)III. General Plant.

1.A. Structures and Improvements – (Account

390)

2.B. Office Furniture and Equipment –

(Account 391) – The following sub-accounts shall should be used:

a.1. Office Furniture – Regular office

furniture and furnishings and miscellaneous equipment such as lounge equipment.

b.2. Office devices such as typewriters,

calculating, reproducing, addressing, blueprinting, cash registers, check

writers and other office machines.

c.3. Computers and peripheral equipment

3.C. Transportation Equipment – (Account 392)

– The following sub-accounts shall should be used:

a.1. Passenger cars and light trucks (trucks

of one ton capacity or less)

b.2. Heavy trucks (trucks of greater than one

ton capacity)

c.3. Special purpose vehicles such as

trailers

d.4. Airplanes

4.D. Stores Equipment – (Account 393)

5.E. Tools, Shop and Garage Equipment –

(Account 394)

6.F. Laboratory Equipment – (Account 395)

7.G. Power Operated Equipment – (Account 396)

8.H. Communication Equipment – (Account 397)

9.I. Miscellaneous Equipment – (Account 398)

– Investment in miscellaneous equipment such as kitchen equipment, infirmary

equipment. , etc.

(4) The accounts under subsection (3) shall be implemented as of the beginning of the next fiscal year following the adoption of this rule. As of that point in time:

(a) Reserve activity data, mortality activity data, salvage and costs of removal are to be recorded to these accounts for subsequent activity.

(b) The separation of embedded investments and reserves under prior accounts into balances relating to accounts under subsection (3) may require estimation. For accounts where vintage data is to be maintained, development of the vintaged distributions of those investments may require synthesization. Vintaged distribution of the reserves is not required.

(c) Where any existing accounts are

, in the opinion of

the Commission, essentially

compatible with those listed in subsection (3)

for depreciation study purposes, those existing accounts shall be deemed to be

in compliance with this rule.

Rulemaking Authority 350.127(2), 366.05(1) FS. Law Implemented 366.05(1), 366.06(1) FS. History–New 11-7-85. Formerly 25-7.46. Amended, __________.