Discussion

of Issues

Issue 1:

Should the Commission propose the adoption of Rule 25-30.4575,

F.A.C., Operating Ratio Methodology?

Recommendation:

Yes, the Commission should propose the adoption of

Rule 25-30.4575, F.A.C., as set forth in Attachment A. The Commission should

certify Rule 25-30.4575, F.A.C., as a minor violation rule. (Harper, Galloway)

Staff Analysis:

In a staff-assisted rate

case (SARC), a calculation is made to determine the utility’s revenue

requirement. The revenue requirement reflects the monies a utility needs to

recover its operating expenses and provide it with an opportunity to earn a

fair rate of return on its investment.

The traditional calculation of

revenue requirement for smaller water and wastewater utilities is achieved by

adding the operation and maintenance (O&M) expenses to the net depreciation

expense, amortization expense, taxes other than income taxes, income taxes, and

a return on investment. The “return on investment” for SARCs is the overall

rate of return multiplied by the amount of rate base. All of these components

added together make up the revenue requirement in a SARC through traditional

ratemaking. However, in some SARCs, traditional ratemaking, also referred to as

the rate of return methodology, does not always provide sufficient revenue to

protect against potential variances in revenue and expenses. In these cases,

the utility may qualify for the operating ratio methodology.

When the operating ratio

methodology is applied, instead of calculating the revenue requirement by

including the return on investment (rate of return x rate base), the “return on

investment” has been replaced by an operating margin. The operating margin is

calculated by multiplying a defined percentage by the amount of O&M

expenses. As stated in the Lake Osborne Order, the operating ratio methodology

substitutes O&M expenses for rate base in calculating the amount of return

(or margin).

The table below shows the

difference between the two methodologies, the use of a rate of return times

rate base (traditional rate base methodology), as compared to the margin percentage

times operation and maintenance expenses (operating ratio methodology).

Table 1-1

Comparison of

Traditional and Operating Ratio Methodologies

|

Traditional Revenue

Requirement Calculation

|

Operating Ratio

Methodology

|

|

Operation and Maintenance

Expense

|

Same

|

|

Net Depreciation Expense

|

Same

|

|

Amortization

|

Same

|

|

Taxes Other than Income Taxes

(less RAFs)

|

Same

|

|

Income Taxes

|

Same

|

|

Rate of Return percent x

Rate Base

|

Margin percent x

O&M expense

|

|

= Revenue Requirement before

RAFs

|

= Revenue Requirement before RAFs

|

Many utilities that apply for a

SARC are financially troubled systems. Many times, these are not utilities that

are simply earning below the bottom of their authorized rate of return range;

these are utilities that are losing money. Often, these are utilities that have

been losing money on a consistent basis over a prolonged period of time. The

operating ratio methodology is intended to act as a bridge for these troubled

systems to become financially viable and return to the traditional revenue

requirement calculation. The operating ratio methodology also provides a

lifeline for them to stay in business and remain viable entities that can

provide safe and reliable water and wastewater services to their customers.

At the staff workshop and in its

post-workshop comments, OPC indicated its preference for the proposed Commission

rule to codify the operating ratio methodology set forth in the Lake Osborne

Order. OPC stated that because the proposed rule does not incorporate the exact

same criteria set forth in the Lake Osborne Order, it defies the purpose of

rulemaking and allows for the development of new policy based on non-existent

difficulties. OPC further stated that the Commission’s policy on the operating

ratio methodology had been clearly and consistently applied over 21 years.

The Lake Osborne Order recognized

that determining whether to utilize the operating ratio methodology required a

great deal of judgement. In keeping with the spirit of the Lake Osborne Order,

staff considered whether to include each of the five criteria from the Lake

Osborne Order in the proposed rule. However, because the Lake Osborne Order

states that the Commission “may” consider the factors listed in the order, this

would give the Commission too much discretion in the context of rulemaking

under Section 120.545(1), F.S. Therefore, staff began the process of

scrutinizing each criteria in hope of finding a way to enable the same

understanding that judgement is critical in determining which SARCs should

qualify for the operating ratio methodology.

For smaller water and wastewater

utilities whose resources are very limited, a SARC is a daunting process, even

though staff provides the expertise. Staff notes that some utilities that apply

for a SARC have never been before the Commission for a rate case or applied for

a rate increase, despite having been in existence for decades. Because many

SARCs are financially troubled systems, staff believes the suggestion that

there is no evidence of a need to make the proposed adjustments contained in

the proposed rule is misplaced.

Staff believes the attached

proposed rule is an opportunity to be proactive rather than reactive. Staff

disagrees with OPC’s assertion that provisions of the proposed rule address

“non-existent difficulties.” Instead, staff believes if the Commission codifies

the practice in a rule, the proposed rule should reflect the Commission

practice that has applied for over 20 years, the Commission’s experience gained

from implementing the operating ratio methodology, and the current economic and

operational conditions that small water and wastewater utilities face. Staff’s

analysis below discusses in more detail the areas where the Commission’s policy

on the operating ratio methodology should be refined from the Commission’s

policy set forth in the Lake Osborne Order.

Subsection (1) of the

Rule – How the Operating Ratio Methodology Should be Calculated

Subsection (1) of Rule

25-30.4575, F.A.C., provides that the operating ratio methodology will

calculate the water or wastewater utility’s revenue requirement based on the

utility’s operating expenses plus a margin of 15 percent of the utility’s

operation and maintenance expenses.

15 Percent Margin and No $10,000 Cap

OPC commented that the margin

percentage should be 10 percent with a $10,000 cap, consistent with the Lake

Osborne Order. OPC alleged there is no evidence that the Commission’s current

practice is ineffective or causing harm.

Again, staff disagrees with OPC’s

suggestion that there is no evidence to support an increase in the margin

percentage and the removal of $10,000 cap. While the Commission has never

applied a margin greater than 10 percent in any of the cases where operating

ratio has been approved, staff believes the rule should promote a policy that

allows utilities to provide the safest and most reliable service to customers.

Staff believes that changes in circumstances have occurred since the Lake Osborne

Order and the changes must be considered and evaluated. U.S. Water Services

stated in its comments that:

Many of the

utilities that I manage have little to no rate base through no fault of the

acquiring utility and are faced with financial difficulties meeting day-to-day

operations. Just as many of these utilities were financially non-viable,

distressed utilities that were acquired in order to turn them around and

provide safe and reliable service to customers. Without the operating margin,

several of these utilities would either not have been acquired and/or would

remain financially non-viable.

U.S. Water also stated that the

10 percent margin that was established more than 20 years ago in the Lake

Osborne Order should be further evaluated. Staff agrees, and believes that the

proposed rule’s 15 percent margin represents a natural evolution of the practice

addressed in the Lake Osborne Order.

Other states’ policies regarding

use of an operating ratio and the associated percentage applied to achieve a

margin were analyzed in the Lake Osborne Order. As part of this rule docket,

staff sent out a request through the National Association of Regulatory Utility

Commissioners (NARUC) to learn what other states have been doing since the

Commission’s initial decision in 1996. The specific states referenced in the

Lake Osborne Order included Kentucky, North Carolina, South Carolina,

California, and Michigan. With the exception of Michigan, which no longer

regulates water and wastewater utilities, and California, which did not respond

to the request, the states referenced in the Lake Osborne Order have not

changed from their 1995-1996 alternative rate setting policies. These states

are very interested in what the Florida Commission will decide. Below is a

synopsis of current policies for these states:

·

Kentucky

has been using a 12 percent margin since 1995-1996 and also allows a

dollar-for-dollar coverage for short-term interest expense.

·

North

Carolina continues to use a margin based on the yield on the 5 year U.S.

Treasury Bond plus 3 percent for risk.

·

South

Carolina sets operating margins for each water and wastewater utility

regardless of size and recent rulings have been above the 15 percent margin

level. However, the typical range is 10 – 15 percent. Two cases in 2018 were

settled with one margin of 12.32 percent and the other margin was 14.99

percent.

While it is important to be

informed about what other states are doing with regard to alternative rate

making, staff believes that Florida is in a unique situation with respect to

regulation of water and wastewater utilities. For example, water and wastewater

utilities operating in Florida must contend with a seasonal customer base, saltwater

intrusion, sinkholes, and hurricanes. Therefore, while consideration of other states’ policies is

informative, it is not necessarily conclusive for the Commission’s

determination of what is appropriate for this proposed rule.

OPC commented that the 10 percent

margin is not a fixed dollar amount, and that it increases as expenses

increase. OPC also asserts the proposed rule should include the same $10,000

cap that was in the Lake Osbourne Order. Staff disagrees. Docket No. 160176-WS,

Application for staff assisted rate case

in Polk County by Four Lakes Golf Club, Ltd., is a recent example of a

utility being negatively impacted by the limitation of the $10,000 cap.

Due to the cap, the utility’s allowed margin was reduced from 10 percent to

5.41 percent. Had the 10 percent margin been used, an operating margin of

$18,476 would have been included in the revenue requirement rather than only

$10,000. In this case, even if the full 10 percent margin had been used when

the operating ratio methodology was applied, the utility’s ability to provide

safe and reliable service was still compromised as evidenced by the $64,000 operating

loss it reported for the year.

Thus, contrary to OPC’s argument, to include a $10,000 cap and 10 percent

margin in the proposed rule would be harmful to the utilities and their ability

to provide safe and reliable service.

Docket No. 160165-WS, In re: Application for staff assisted rate case in

Gulf County by ESAD Enterprises, Inc. d/b/a Beaches Sewer Systems, Inc., is

another recent example of a utility being negatively impacted by the limitation

of the $10,000 cap. Due to the cap, the utility’s allowed margin was reduced

from 10 percent to 7.25 percent.

Had the 10 percent margin been used, an operating margin of $13,801 would have

been included in the revenue requirement rather than only $10,000.

The Lake Osborne Order stated

that it may be appropriate to apply a margin greater than 10 percent in the

case of a fully depreciated system where there would be an expectation of

greater than average volatility in operation and maintenance costs. However, of

the 23 cases where the operating ratio methodology was recommended, staff did

not pursue a margin greater than 10 percent in any of them. The caveat

contained in the Lake Osborne Order served to discourage application of a

higher margin by the instruction to prove “an expectation of greater than average

volatility in operation and maintenance costs.” Staff has found that it has

been a difficult task to prove “greater than average volatility” prior to the

volatility occurring.

Recently, in Order No.

PSC-2018-0327-PAA-WS, the Commission recognized that smaller water and

wastewater utilities are more risky than other utilities. In the order, the

Commission listed a variety of reasons that make smaller water and wastewater

utilities more risky in nature:

(1) WAW

utilities are more capital intensive than electric or natural gas utilities;

(2) WAW utilities experience lower relative depreciation rates than other

utilities, thereby providing less cash flow; (3) WAW utilities experience

consistently negative free cash flow, thereby increasing their financing

requirements; (4) WAW utilities’ credit metrics are inferior to those of

electric and natural gas utilities; (5) Florida WAW utilities are substantially

smaller than electric and natural gas utilities by virtually any measure

including total revenues, total assets, and market capitalization; (6) WAW

utilities’ earnings are much more volatile (uncertain) than electric and

natural gas utilities’ earnings; and (7) WAW utilities experience many more

business failures than electric and natural gas utilities.

Staff disagrees with OPC’s

opinion that the margin should remain unaffected by the Consumer Price Index

(CPI) or other inflationary factors. Staff believes that the percentage

increase from 10 percent to 15 percent reflects not only inflationary factors,

but also compensates for the riskier nature and true plight of smaller water

and wastewater utilities that qualify and apply for a SARC. Regarding any

underlying argument of potential overearnings, staff believes the Commission’s

annual in-house review of Annual Reports, which are required to be filed by all

regulated water and wastewater utilities, will alert the Commission of any

potential overearnings.

As discussed below, Subsection

(2) of the proposed rule includes limiting criteria. Subsection (2) would limit

the use of the operating ratio methodology to only those utilities that are

eligible for a SARC, and those utilities must continue to be eligible for a

SARC when the methodology is applied.

Water and Wastewater Utilities that

are Resellers

Subsection (1) of proposed Rule

25-30.4575, F.A.C., further provides that for water and wastewater utilities

that are resellers, purchased water and purchased wastewater expenses will be

removed from operation and maintenance expense before the 15 percent margin is

applied. As stated in the Lake Osborne Order, if a utility is a reseller, the

issue is whether or not purchased water and/or wastewater costs should be

excluded in the computation of the operating margin. Staff believes that this

qualification continues to remain valid, and thus, it is reflected in

Subsection (1) of proposed Rule 25-30.4575, F.A.C.

Subsection (2) of the Rule – Criteria

for Use of Operating Ratio Methodology

Subsection (2) of the proposed

rule addresses the criteria the Commission would use to determine whether to

use the operating ratio methodology.

125 Percent of O&M Expenses

Subsection (2)(a) of proposed Rule

25-30.4575, F.A.C., provides that the operating ratio methodology may only be

used for those utilities whose rate base is no greater that 125 percent of

operation and maintenance expenses. In its post-workshop comments, OPC takes

issue with this language in the proposed rule. While the Lake Osborne Order

limits eligibility to utilities with O&M expenses equal to or less than

rate base, the Commission also stated in the Order that the initial eligibility

criteria for the operating ratio methodology was purposely limited until more

experience was gained.

While this rule is designed for

small water and wastewater utilities, particularly those utilities where

investment in rate base is limited relative to the level of O&M expenses,

it is informative to compare what the typical relationship between rate base

and the level of O&M expenses is for larger, more financially viable

systems. For Class A water utilities in Florida, average rate base is three

times greater than the average level of O&M expenses. For Class A

wastewater systems, average rate base is five times greater than the average

level of O&M expenses. Staff believes that requiring the investment in rate

base to be less than the level of O&M expenses for purposes of this rule

appears overly restrictive when compared to the typical relationship between

rate base and the level of O&M expenses in this industry. Because the

exigent conditions that exist for water and wastewater utilities whose rate

base equals O&M expenses also exist for utilities with rate base marginally

greater than O&M expenses, staff recommends that the proposed rule should

modestly increase the threshold that was set forth in the Lake Osborne

Order.

Based on information from the

2017 Annual Reports, under the current practice, the operating ratio

methodology is available to 30 water and 29 wastewater systems. If the

threshold for rate base is increased to 125 percent of O&M expenses, an

additional 6 water and 8 wastewater systems will be eligible for the operating

ratio methodology. While this change represents a modest increase in the number

of eligible utilities, staff believes it is a reasonable evolution of the

eligibility criteria for use of the operating ratio methodology.

Limit on the Application of the

Operating Ratio Methodology to Only the Utilities that Qualify for a SARC

Subsection (2) of the proposed

rule provides that the operating ratio methodology may only be used for

utilities that qualify for a SARC under Rule 25-30.455, F.A.C. The current

threshold for SARC eligibility under Rule 25-30.455(1), F.A.C., applies to

water and wastewater utilities whose total gross annual operating revenues are

$300,000 or less per system, and $600,000 or less on a combined basis. At the

time of the Lake Osborne Order, the SARC threshold was for utilities with

revenue of $150,000 or less per system, which precluded any Class B utilities

from qualifying for a SARC.

OPC commented that the proposed

rule should remain consistent with the Lake Osborne Order and that only Class C

utilities should be eligible for the operating ratio methodology. However,

since the Lake Osborne Order, the Florida Legislature has amended Section

367.0814, F.S., to increase the SARC threshold and to add language providing

that the threshold for SARC eligibility must be adjusted on July 1, 2013, and

every five years thereafter. As a result, the SARC threshold increased to

$275,000 in July 2013 and then to $300,000 in July 2018. This means Section

367.0814, F.S., allows SARCs for utilities with revenue of $300,000 or less per

system, which may include some Class B utilities. Accordingly, staff believes

OPC’s position to exclude all Class B utilities for eligibility for the

operating ratio methodology is contrary to Section 367.0814, F.S. To be

consistent with the statute and because exigent conditions that exist for many

Class C utilities may also exist for smaller Class B utilities, staff believes

utilities with revenue of $300,000 or less per system that qualify for a SARC

should be eligible for the use of the operating ratio methodology.

Limit on the Use of the Operating

Ratio Methodology to Only Utilities that Continue to Qualify for a SARC

Subsection (2)(b) of the proposed

rule provides that if the application of the operating ratio methodology

changes the utilities' qualification for a SARC, the operating ratio

methodology may not be applied. Thus, this provision ensures that only

utilities that qualify for a SARC will benefit from the rule.

Quality of Service and Condition of

Plant

OPC also takes issue with the fact that the proposed rule

does not include the Lake Osborne Order’s considerations of the quality of

service and condition of the plant. OPC seems to suggest these considerations

should be included in the rule as a means to disqualify certain utilities from

the use of the operating ratio methodology. Staff disagrees. Staff believes

that the Lake Osborne Order recognized that quality of service or condition of

the plant are always considerations in a SARC and that, in fact, poor quality

of service or condition of the plant may be indicative of a utility that

would benefit from the use of the

operating ratio methodology. As stated in the Lake Osborne Order, “poor

condition of plant and/or unsatisfactory quality may be due to a variety of

factors such as age of the system, poor maintenance” and these factors may

“highlight the need for an adequate revenue stream to properly test and treat

the water and maintain/renovate the system.”

Because evaluation of the quality of service and condition

of the plant are standard considerations in every SARC, staff

believes it is unnecessary to include this criteria in the proposed rule.

Moreover, it stands to reason that unsatisfactory quality of service and

condition of the plant may be a result of insufficient revenues. To identify

poor quality of service or condition of the plant in the proposed rule may

cause a utility to be denied the opportunity to use the operating ratio

methodology, which would not be in the long-term interest of the utility or its

customers. If poor conditions are a direct result of the owner directly

contributing to the system’s decline, the Commission can pursue revocation of

the certificate and/or an escrow of operating ratio methodology funds when

improvements are needed to restore the utility system. Therefore, staff

believes that because quality of service and condition of the plant are

considered in every SARC, these factors do not need to be included and used as

disqualifying criteria in proposed Rule 25-30.4575, F.A.C.

Developer-Owned Utilities

OPC also took issue with the

proposed rule because it did not include the criteria from the Lake Osborne

Order regarding developer-owned water and wastewater utilities. In the Lake

Osborne Order, the Commission stated that being developer-owned should not

disqualify a utility from the operating ratio method. The Commission also

acknowledged in the Order that it may not be appropriate to use the operating

ratio if the development is in the early stages of growth. The Commission

stated:

Other factors that may be considered when determining

eligibility for the operating ratio method are customer growth, the developer’s

financial condition, the utility’s financial and operational condition,

government mandated improvements and/or other unanticipated expenses. The level

of CIAC collected by the utility may also be considered.

The points contemplated in this criteria are standard

considerations in every SARC. Therefore, staff believes it is duplicative and

unnecessary to include these criteria in the rule.

Summary

The proposed rule codifies the

Commission’s practice of applying the operating ratio methodology. As discussed

above, OPC expressed concerns about not seeing the long-standing Commission

practice of using the five criteria set forth in the Lake Osborne Order in the

attached proposed rule. However, staff believes the proposed rule sufficiently

and clearly addresses the necessary qualifications for implementing the

operating ratio methodology on a going forward basis. Simply restating the same

criteria and considerations of the Lake Osborne Order in the proposed rule as

OPC suggests ignores the discretionary nature of the Lake Osborne Order

criteria as well as the current requirements for rulemaking under Section

120.545(1), F.S., and the 20 years of Commission experience and practice in

implementing the operating ratio methodology. Simply put, shoehorning the same

discretionary criteria and considerations from the Lake Osborne Order into a

rule would be contrary to the rulemaking requirements. Moreover, the proposed

rule is not only well within the Commission’s delegated grant of legislative

authority but is also necessary to avoid violating the prohibition against

unadopted rules.

Even with the adoption of the

rule, staff will continue to present to the Commission both the option of the

traditional and the operating ratio methodologies and the potential effect on

the revenue requirement. The ultimate decision to use the operating ratio

methodology will remain with the Commission. Staff believes the proposed rule

captures the purpose and criteria necessary for the use of the operating ratio

methodology for determining the revenue requirement and recommends that that

the proposed rule as set forth in Attachment A should be approved.

Minor Violation Rules Certification

Pursuant to Section 120.695, F.S., beginning July 1, 2017,

for each rule filed for adoption the agency head shall certify whether any part

of the rule is designated as a rule the violation of which would be a minor

violation. Rule 25-30.4575, F.A.C., is a rule for which a violation would be

minor because violation of the rule would not result in economic or physical

harm to a person or an adverse effect on the public health, safety, or welfare

or create a significant threat of such harm.

Thus, staff recommends that the Commission certify Rule 25-30.4575,

F.A.C., as a minor violation rule.

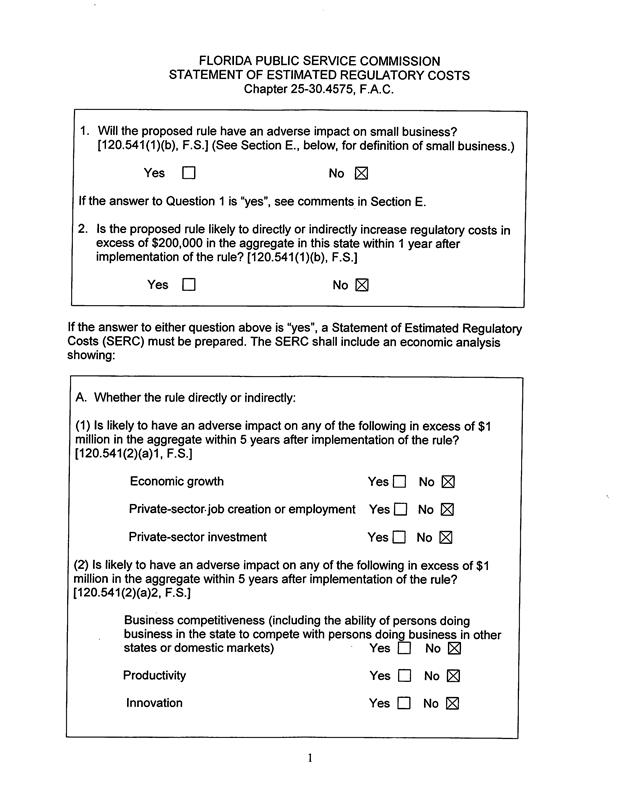

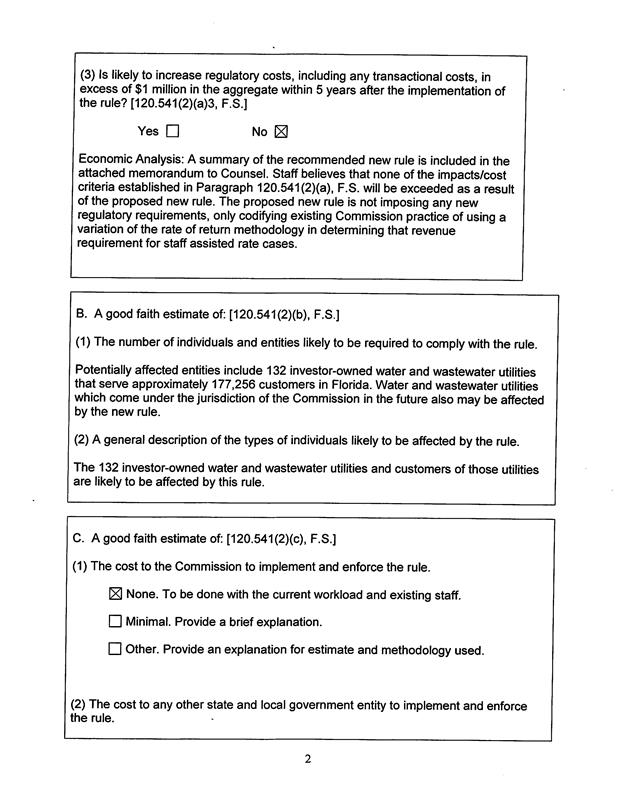

Statement of Estimated Regulatory Costs

Pursuant to Section 120.54, F.S., agencies are encouraged

to prepare a statement of estimated regulatory costs (SERC) before the

adoption, amendment, or repeal of any rule. The SERC is appended as Attachment C

to this recommendation. The SERC analysis also includes whether the rule is

likely to have an adverse impact on growth, private sector job creation or

employment, or private sector investment in excess of $1 million in the

aggregate within five years of implementation.

The SERC concludes that the rule will not likely directly

or indirectly increase regulatory costs in excess of $200,000 in the aggregate

in Florida within one year after implementation. Further, the SERC concludes that the rule

will not likely have an adverse impact on economic growth, private sector job

creation or employment, private sector investment, business competitiveness,

productivity, or innovation in excess of $1 million in the aggregate within

five years of implementation. Thus, the rule does not require legislative

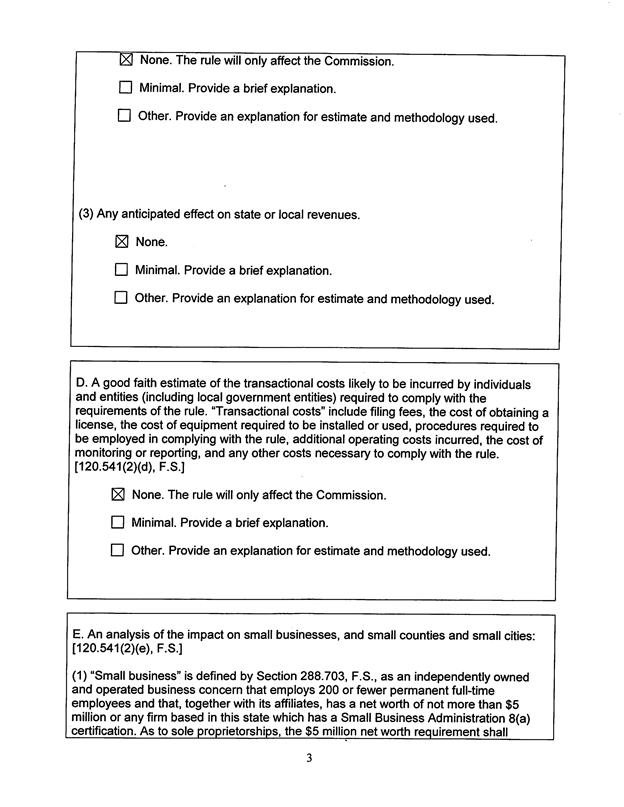

ratification pursuant to Section 120.541(3), F.S. In addition, the SERC states that the rule

will not have an adverse impact on small business and will have no impact on

small cities or counties. No regulatory alternatives were submitted pursuant to

paragraph 120.541(1)(a), F.S. None of

the impact/cost criteria established in paragraph 120.541(2)(a), F.S., will be

exceeded as a result of the recommended revision.

Conclusion

Based on the foregoing, staff recommends the Commission

propose the adoption of Rule 25-30.4575, F.A.C., as set forth in Attachment A. In

addition, staff recommends the Commission certify Rule 25-30.4575, F.A.C., as a

minor violation rule.

Issue 2:

Should this docket be closed?

Recommendation:

Yes. If no

requests for hearing or comments are filed, the rule may be filed with the

Department of State, and this docket should be closed. (Harper)

Staff Analysis:

If no requests for hearing or comments are filed,

the rule may be filed with the Department of State, and this docket should be

closed.