|

State of Florida

|

Public Service Commission

Capital Circle Office Center ● 2540 Shumard

Oak Boulevard

Tallahassee, Florida 32399-0850

-M-E-M-O-R-A-N-D-U-M-

|

|

DATE:

|

September 20, 2019

|

|

TO:

|

Office of Commission Clerk (Teitzman)

|

|

FROM:

|

Office of the General Counsel (Harper, A. King)

Division of Economics

(Coston, Draper, Galloway, Guffey, McNulty)

Division of Engineering

(Doehling, Graves, L. King)

Office of Industry

Development and Market Analysis (Breman, Crawford, Eichler)

|

|

RE:

|

Docket No. 20190131-EU – Proposed adoption

of Rule 25-6.030, F.A.C., Storm Protection Plan and Rule 25-6.031, F.A.C.,

Storm Protection Plan Cost Recovery Clause.

|

|

AGENDA:

|

10/03/19 – Regular Agenda – Rule Proposal – Interested Persons May

Participate

|

|

COMMISSIONERS ASSIGNED:

|

All Commissioners

|

|

PREHEARING OFFICER:

|

Fay

|

|

RULE STATUS:

|

Proposal May Not Be Deferred.

Rules must be proposed by October 31, 2019.

|

|

SPECIAL INSTRUCTIONS:

|

None

|

|

|

|

|

Case Background

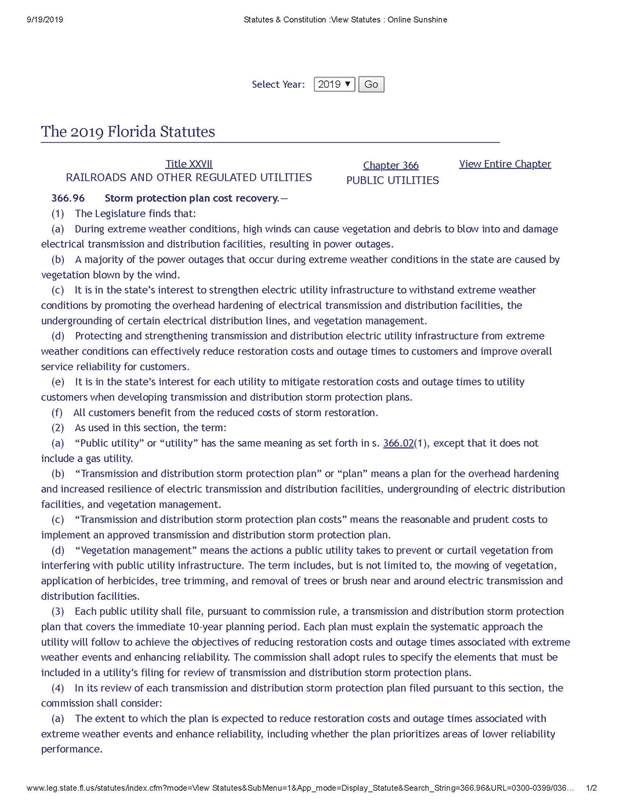

The 2019 Florida Legislature passed SB 796 to enact Section

366.96, Florida Statutes (F.S.),

entitled “Storm protection plan cost recovery.” Section 366.96, F.S., requires

each investor-owned electric utility (IOU) to

file a transmission and distribution storm protection plan (storm protection plan)

for the Commission’s review and directs the Commission to hold an annual proceeding

to determine the IOU’s prudently incurred costs to implement the plan and allow

recovery of those costs through a Storm Protection Plan Cost Recovery Clause

(SPPCRC).

Section 366.96(3), F.S., requires the Commission to adopt

rules to specify the elements that must be included in an IOU’s filing for the

Commission’s review of its storm protection plan. Section 366.96(11), F.S.,

further requires that the Commission adopt rules to implement and administer

the section and mandates that the Commission propose a rule for adoption as

soon as practicable after the effective date of the act, but not later than

October 31, 2019.

In furtherance of the Legislature’s directive, the

Commission’s Notice of Development of Rulemaking was published in Volume 45,

No. 11, of the Florida Administrative Register on June 7, 2019. The notice

included two new rules: Rule 25-6.030, Florida Administrative Code (F.A.C.),

which would specify the elements that must be included in an IOU’s storm

protection plan; and Rule 25-6.031, F.A.C., which would establish the SPPCRC.

Staff held rule development workshops to obtain

stakeholder comments on the draft rules on June 25, 2019, and August 20, 2019. Representatives

from Florida Power & Light Company (FPL), Tampa Electric Company (TECO),

Duke Energy Florida, LLC (DEF), Gulf Power Company (Gulf), Florida Public Utilities

Company (FPUC), Florida Retail Federation (FRF), Florida Industrial Power Users

Group (FIPUG), and the Office of Public Counsel (OPC) participated at the

workshops and submitted post-workshop comments. Additionally, representatives

from Florida Electric Cooperatives Association, Inc., (FECA) and Florida

Municipal Electric Association (FMEA) submitted post-workshop comments.

The Notice of Development of Rulemaking also included a

number of existing Commission rules that staff identified as potential

candidates for amendment or repeal in order to fully implement the new

legislation. Several stakeholders opined that it would be difficult to

determine any effects on existing rules until Rules 25-6.030 and 25-6.031, F.A.C.,

were adopted and effective. Staff agrees. Thus, whether any other existing

rules should be amended or repealed will be addressed in a future staff

recommendation for the Commission’s consideration after Rules 25-6.030 and

25-6.031, F.A.C., become effective.

Storm Protection Plans

Prior to the enactment of Section 366.96, F.S., IOUs submitted

storm hardening plans pursuant to Rule 25-6.0342, F.A.C., Electric

Infrastructure Storm Hardening, and recovered storm hardening costs through

base rate proceedings. Section 366.96, F.S., changes this process.

Section 366.96, F.S., finds that it is in the state’s

interest for IOUs to protect and strengthen the state’s transmission and

distribution systems in order to reduce outage times and restoration costs

associated with extreme weather conditions and enhance overall reliability. In

furtherance of this interest, Section 366.96(3), F.S., requires each IOU to

file a storm protection plan that covers the immediate 10-year planning period

and explains the systematic approach the utility will follow to reduce

restoration costs and outage times associated with extreme weather events. The

statute requires the Commission to adopt rules to specify the elements that

must be included in each utility’s storm protection plan. The intent of Rule

25-6.030, F.A.C., Storm Protection Plan, is to meet this statutory mandate.

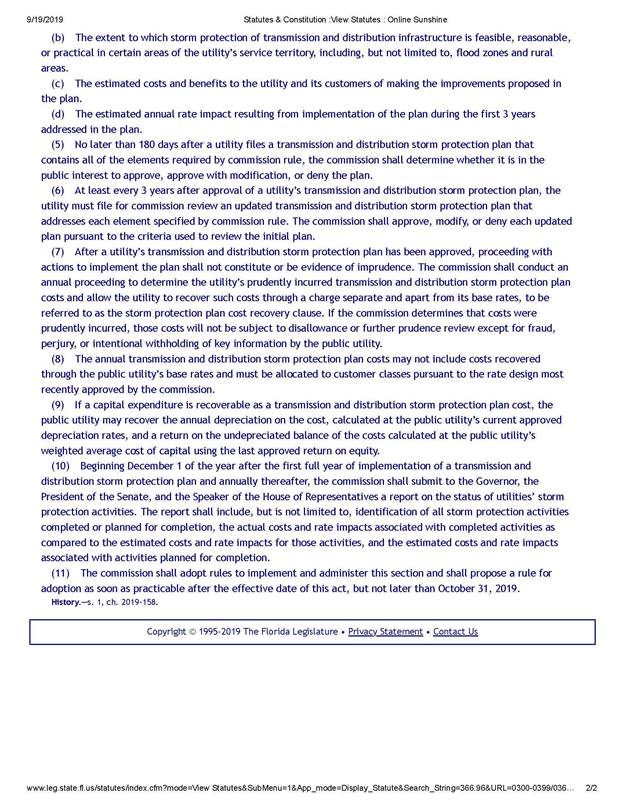

Section 366.96(5), F.S., requires that no later than 180

days after an IOU files a storm protection plan that contains all of the

elements required by the Commission rule, the Commission must determine whether

it is in the public interest to approve, approve with modification, or deny the

plan. The statute requires that in reviewing the storm protection plan, the

Commission must consider the following four criteria:

1.

The extent to which the plan is expected to reduce

restoration costs and outage times associated with extreme weather events and

enhance reliability, including whether the plan prioritizes areas of lower

reliability performance.

2.

The extent to which storm protection of transmission

and distribution infrastructure is feasible, reasonable, or practical in

certain areas of the utility’s service territory, including, but not limited to, flood zones

and rural areas.

3.

The estimated costs and benefits to the utility and its

customers of making the improvements proposed in the plan.

4.

The estimated annual rate impact resulting from implementation

of the plan during the first 3 years addressed in the plan.

Thus, the information required by the Commission in Rule

25-6.030, F.A.C., Storm Protection Plan, must enable the Commission to review

each utility’s storm protection plan under the above criteria and ultimately

determine whether the plan is in the public interest.

Staff envisions that after Rule 25-6.030, F.A.C., becomes

effective, the Commission will open dockets to review each utility’s storm protection

plan. The Prehearing Officer will issue an Order Establishing Procedure (OEP)

to set all the controlling dates in the dockets, including the date by which

the IOUs must submit their plans and the hearing dates. Although separate dockets

will be opened to address each IOU’s storm protection plan, staff envisions

that one hearing will be held to address all of the dockets. As mentioned

above, the Commission will have 180 days after the IOU files its plan to

approve, approve with modifications, or deny the plan.

Additionally, Section 366.96(6), F.S., mandates that at

least every 3 years after approval of an IOU’s storm protection plan, the

utility must file for Commission review an updated storm protection plan that

addresses each element specified by Commission rule. The Commission must approve,

modify, or deny each updated plan pursuant to the criteria used to review the

initial plan. Staff envisions that the Commission will open dockets every 3

years to review each utility’s updated storm protection plan and that the

Prehearing Officer will issue an Order Establishing Procedure to set all

controlling dates in the dockets.

Section 366.96(10), F.S., also requires that beginning

December 1 of the year after the first full year of implementation of a storm

protection plan and annually thereafter, the Commission must submit a report on

the status of IOUs’ storm protection activities to the Governor, the President

of the Senate, and the Speaker of the House of Representatives. The report must

include, but is not limited to, identification of all storm protection

activities completed or planned for completion, the actual costs and rate

impacts associated with completed activities as compared to the estimated costs

and rate impacts for those activities, and the estimated costs and rate impacts

associated with activities planned for completion. Staff is recommending

requirements in Rule 25-6.030, F.A.C., to gather the information that the Commission

will need to develop its report pursuant to the statute. Staff envisions that

approval of this report will take place at a Commission Internal Affairs

meeting.

Storm Protection Plan Cost Recovery Clause

Section 366.96(7), F.S., directs the Commission to conduct

an annual proceeding, the “storm protection plan cost recovery clause,” to

determine an IOU’s prudently incurred storm protection plan costs and allow the

utility to recover such costs through a charge separate and apart from its base

rates. Rule 25-6.031, F.A.C., is intended to establish the SPPCRC, pursuant to

the statute.

Section 366.96(9), F.S., specifically includes in those

recoverable costs the depreciation costs associated with eligible capital

expenditures, as well as a return on the undepreciated portions of capital

expenditures at the company’s weighted average cost of capital. If the Commission

determines that costs were prudently incurred, those costs will not be subject

to disallowance or further prudence review except for fraud, perjury, or

intentional withholding of key information by the public utility. Section

366.96(8), F.S., provides that costs may be recovered through the clause only

if they are not recovered through base rates.

Once Rule 25-6.031, F.A.C., becomes effective, staff

envisions that the Commission will open a docket to establish the SPPCRC and

that like the Commission’s other cost recovery clause dockets, the Prehearing

Officer will issue an OEP to set forth all the controlling dates in the docket,

including the dates by which any requests for cost recovery for the year must

be filed. Staff also envisions that the SPPCRC will become a “roll-over” docket

like the Commission’s other cost recovery clause dockets.

There was discussion at the workshop and in post-workshop

comments from stakeholders as to when the hearing in the SPPCRC should be held.

Section 366.96, F.S., does not mandate IOUs to file for cost recovery each year

under the new clause, nor does the section contain any dates by which the

Commission must render its decision on any requests for cost recovery. Thus,

staff believes that the Commission has the discretion to determine the hearing

dates for this clause proceeding, and like the other cost recovery clauses any

controlling dates for the proceeding should be determined by the Prehearing

Officer, in conjunction with the Chairman’s Office.

The

Process for Storm Plan Approval and Cost Recovery

Staff

envisions that once Rules 25-6.030 and 25-6.031, F.A.C., become effective, the Commission

will open dockets simultaneously to address the plans and establish the SPPCRC.

While each IOU will have a docket to address its storm protection plan, one

hearing will be held to address all the plans. There will be a single docket and

single hearing for the SPPCRC, which will address IOUs’ recovery of costs

incurred implementing the storm protection plans. The hearing on an IOU’s

petition for cost recovery will be held only after the Commission has approved

the utility’s storm plan. Accordingly,

staff envisions that the process will work as follows: First, an electric utility will submit to the Commission a storm

protection plan; then the Commission will hold a hearing in the plan

docket to determine if the utility’s storm protection

plan is reasonable. If the utility’s storm protection

plan is approved, the utility’s petition for cost recovery for that plan

will be addressed in the hearing in the clause docket. If the utility’s

petition for cost recovery is approved in the SPPCRC, factors will be set and

go into effect at a date determined by the Commission. Though storm protection

plan cost recovery factors will be calculated separately, they will be

incorporated in the energy charge line item that includes the other clauses on

customers’ bills.

This recommendation addresses whether the Commission

should propose new Rules 25-6.030 and 25-6.031, F.A.C. The Commission has

jurisdiction pursuant to Sections 120.54 and 366.96, F.S.

Discussion

of Issues

Issue 1:

Should the Commission propose the adoption of Rule

25-6.030, F.A.C., Storm Protection Plan, and Rule 25-6.031, F.A.C., Storm

Protection Plan Cost Recovery Clause?

Recommendation:

Yes. The Commission should propose the adoption of

Rules 25-6.030 and 25-6.031, F.A.C., as set forth in Attachment A. The

Commission should also certify Rules 25-6.030 and 25-6.031, F.A.C., as minor

violation rules. (Breman, Eichler, Harper, A. King, Graves, Guffey)

Staff Analysis:

The purpose of this rulemaking is to create Rule

25-6.030. F.A.C., to specify the elements that must be included in an

investor-owned utility’s storm protection plan, and Rule 25-6.031, F.A.C., to

establish the SPPCRC. Staff is recommending that the Commission propose the

rules as set forth in Attachment A.

Overarching Themes That Emerged During Rule

Development

Staff held two rule development workshops on Rules 25-6.030

and 25-6.031, F.A.C. Three overarching themes seemed to drive the bulk of the

stakeholder’s comments. The first is whether Section 366.96, F.S., permits the

Commission to allow recovery of projected costs in the SPPCRC. The second is

when and through what filing should IOUs provide project-level detail to the

Commission. The third is what the approval of a storm protection plan means for

approval of costs in the SPPCRC. Before staff discusses its recommended

language for each rule, staff believes that it is important to discuss these

overarching issues.

Allowing for Projected Costs vs.

Actual/Incurred Costs Only

Staff envisions the SPPCRC mirroring other Commission cost

recovery clauses. In the Nuclear Cost Recovery Clause (NCRC), Energy Conservation

Cost Recovery Clause (ECCR), and Environmental Cost Recovery Clause (ECRC), the

Commission projects the costs the utility will incur in the next year and sets

a factor that will allow the company to recover those costs from customers as

the costs are incurred. Because the costs and the sales used to set the factor

are estimated, the amount of money the utility actually recovers may be more or

less than the actual costs. During the year the costs are incurred and the year

after the costs are incurred, the Commission performs a true-up of the costs

and the recovered amounts so that the utility ultimately recovers only those

costs actually incurred.

OPC asserts that Section 366.96, F.S., only permits IOUs

to recover their prudently incurred costs through the new cost recovery clause.

OPC argues that the Commission can allow IOUs to recover projected costs that

are later trued-up through the NCRC and ECRC because the statutes creating

those clauses specifically reference “projected” costs. According to OPC, because

Section 366.96, F.S., does not specifically provide for this same mechanism, it

therefore prohibits it. In support of this argument, OPC points to earlier

versions of SB 796 that contained language referring to the recovery of

projected costs—language that was almost identical to the language used in the

ECRC statute—and notes that the specific language on projected costs was

removed as the bill made its way through legislative committees.

Staff disagrees with OPC’s reading of the statute. While

the terms “projected costs” and “true-up” are not in Section 366.96, F.S., the

statute does not specifically bar the recovery of incurred costs through the

recovery of projected costs that are later trued-up. The statute is silent on

the matter; it only says that the Commission must allow the IOUs to recover

their prudently incurred costs. Additionally, the fact that language explicitly

providing for the recovery of projected costs was removed by the Senate proves

nothing about the meaning of the final version of the bill that became law.

“[O]ur legislatures speak only through statutes,”

not the legislative history underlying them. Declaring the meaning of a statute

based on speculation about why specific language was removed from the bill

during the legislative process is improper.

The IOUs state that storm protection plan cost recovery

should be based on projected costs and that OPC’s reading of Section 366.96,

F.S., is unduly restrictive. FPL states that this mechanism has worked well for

a wide variety of costs in other clause proceedings “because it allows IOUs to

begin recovery of costs as the costs are projected to be incurred, while

providing staff and intervenors with essentially three opportunities to review

the costs before their recovery is finalized.” FPL also points out that the

Commission has allowed recovery of projected costs subject to true-up with

actual costs under Section 366.93(2), F.S., the NCRC, which provides generally

for recovery of “costs incurred” and only refers to projected costs in

connection with carrying costs on an IOU’s projected construction cost balance.

Staff believes Section 366.96, F.S., gives the Commission

discretion to determine the mechanism by which IOUs can recover their prudently

incurred costs, including allowing IOUs to recover projected costs and

truing-up those projections when actual cost data becomes available. First and

foremost, by using this method, IOUs would ultimately recover only their actual

prudently incurred costs. This not only comports with the current procedure in

the NCRC and ECRC clauses, but it is also consistent with Section 366.96(7),

F.S., which directs the Commission to allow the IOUs to recover “prudently

incurred . . . storm protection plan costs . . . through a charge separate and

apart from its base rates.”

Second, allowing for the recovery of projected costs

enables the IOUs to recover costs as they are incurred. This reduces regulatory

lag and, ultimately, the costs passed on to customers, which is the purpose of

cost recovery clauses. Staff believes IOUs will be entitled to recover carrying

costs associated with the lag between when they incurred costs and when they

recover them. Under OPC’s interpretation, an IOU would incur costs in one year

but couldn’t request recovery of those costs until the next year’s SPPCRC. If

the Commission approved those costs in the SPPCRC, the utility could not begin

recovering the costs until the year after. This leaves customers paying

carrying costs for two years. Thus, using a cost recovery mechanism that should

minimize that regulatory lag, as staff is recommending in draft Rule 25-6.031,

F.A.C., should also minimize the carrying costs customers have to pay.

Third, allowing for the timely recovery of costs

incentivizes IOUs to undertake capital-intensive projects that will achieve the

purpose of the statute: hardening the state’s electric transmission and

distribution infrastructure to better withstand extreme weather conditions.

Fourth, the new statute is forward thinking as it

emphasizes planning in its objective—the statute requires the IOUs to come up

with a 10-year plan, not an annual one. Staff believes that consideration of

projected costs would be consistent with the requirement of long-term planning to

ensure infrastructure is hardened. Allowing projected costs to be included in

storm plan petitions gives the Commission a comprehensive view over the IOUs’

long-term storm protection projects. This is in the public interest because it

allows for transparency and review of the projects before the projects are

completed and costs are incurred. Staff believes that the approval of a storm

protection plan means it is reasonable for an IOU to continue to go forward

with the scope of activities and to incur costs consistent with the approved

plan.

Staff believes it is in the consumers’ interest for IOUs

to recover their incurred costs as near in time to when they were incurred as

possible. For the reasons set forth above, staff’s recommended rules provide

that projected costs are eligible for cost recovery.

When and Where Project-Level Details Should be

Provided

Staff’s recommended rules require IOUs to provide in their

storm protection plan project-level data for each of the first three years of

the plan. All of the IOUs commented that such a requirement is neither

“feasible” nor “desirable.” FPL asserts that the initiation of specific

projects within a program is subject to change until shortly before initiation

due to a host of factors. It argues that, as a consequence, accurately

projecting project-level data two or more years in the future is difficult, if

not impossible. Therefore, FPL suggests that the rules should only require the storm

protection plan to contain project-level data for the first year of the plan.

For the second and third years, it suggests that the data required be “more

general” than the data required for the first year yet still “sufficiently

detailed” to develop rate-impact estimates. FPL further suggests that

project-level detail should be required annually in the clause docket for the

subsequent planning year.

OPC and FRF assert that detailed project and spending

information is needed to ensure the prevention of double recovery by IOUs. OPC

states that “[a]t a minimum, year-by-year project and cost detail should be

required on a basis that allows the Commission and customers to determine what

costs, activities[,] and projects are being recovered in base rates at the time

recovery is sought” in the SPPCRC.

Staff believes that project-level information for each of

the first three years is necessary to provide a baseline for the Commission’s

review and comparison of costs sought in the SPPCRC. Additionally, without this level of detail,

the Commission could not adequately address the legislative requirement of

Section 366.96(4), F.S., as to rate impact, nor would it have enough

information to make an informed decision to modify a plan pursuant to Section

366.96(5), F.S. For these reasons, staff’s recommended rules require

project-level detail for each of the first three years. This is further discussed

in the sections of this recommendation pertaining to subsection (3) of Rule

25-6.030, F.A.C., and subsections (3) and (7) of Rule 25-6.031, F.A.C.

How the Storm

Rules Will Work Together

The third theme that arose from the rule development

workshops was how the approval process for storm protection plans and the clause

process would work together, if an IOU chooses to recover costs through the

clause. In other words, what does approval of a storm protection plan actually

mean in terms of cost recovery later on in the clause?

OPC raised concerns about whether it would have the opportunity

to challenge the costs of a project that was part of program and plan that was

previously approved by the Commission. Pursuant to Section 366.96, F.S., an electric utility may submit to the Commission a storm

protection plan that includes the utility’s proposed programs, projects, and

activities that are designed to meet the objectives of the statute, i.e., reducing

restoration costs and outage times associated with extreme weather events and enhancing

reliability. This is similar to the planning process

in the ECRC. If the utility’s storm protection plan is deemed to be in the

public interest and is approved, the IOUs are authorized to go forward in

implementing the approved plan. Approval of the plan (and programs and projects

within the plan), however, does not constitute a de facto approval of the

costs. Plan approval means the Commission has deemed the utility’s plan

reasonable and the utility may go forward with actions to implement the plan.

The prudence determination is

made later in the clause process. As part of the cost recovery clause, an IOU

seeking recovery for costs made pursuant

to its approved storm protection plan would file its petition at the times

directed by the Commission, pursuant to the OEP in the annual cost recovery

proceeding. As part of its petition, the IOU would submit a list of projects it

anticipates undertaking in the next year, including projected costs for those

projects. The Commission would determine whether the anticipated projects and programmatic

activity are consistent with the utility’s storm protection plan as well as the

reasonableness of the projected costs for those activities. As part of its

petition, the utility would also include available actual cost data for the

current year’s activities as well as actual cost data for the previous year’s activities.

The Commission would determine the prudence of those actual incurred costs and,

using the methods already used in other clauses, set factors for the recovery

of the projected costs and true-up the recovery of costs actually incurred.

Rule 25-6.030,

F.A.C., Storm Protection Plan

Rule 25-6.030, F.A.C., requires each IOU to file a petition

with the Commission for approval of a storm protection plan. The rule describes

the information that must be included in the storm protection plan, as well as

information needed for the Commission to satisfy its duty to file an annual report

with the executive and legislative branches detailing the IOUs’ planned and

completed storm protection projects and the related rate impacts.

Subsection (1): Application and Scope

This subsection requires each investor-owned electric

utility to file a petition with the Commission for approval of a storm

protection plan. It also mandates that the plan cover the utility’s immediate

10-year planning period and must be updated every 3 years.

OPC suggests that language be added to this subsection to

require each utility to file its plan on the third Monday of January of each

year the plan update is to be considered for Commission approval. TECO states

that it plans to prepare a storm protection plan and file it with the

Commission within 4 to 5 months of the storm rules being adopted, e.g., no

later than March 1, 2020. TECO suggests it would be more efficient for all of

the IOUs to file their plans at the same time given that the timing of the

Commission’s approval must be within the 180 day limit provided by Section

366.96, F.S.

The Commission will have 180 days after the utility files

its plan to approve, approve with modifications, or deny the plan; however,

there is no requirement in the statute that the Commission must review the

plans at a particular time of the year. Thus, staff does not recommend that the

Commission include the language offered by OPC, as this language will remove

some Commission discretion as to when the Commission wants to conduct its

review of plans. As discussed in the Case Background, staff envisions that

after Rule 25-6.030, F.A.C., becomes effective, the Commission will open a

docket to review each utility’s storm protection plan. The Prehearing Officer

will issue an Order Establishing Procedure to set all the controlling dates in

the docket, including the date by which investor-owned electric IOUs must

submit their plans and the hearing dates. Staff envisions that this same

procedure will be used to review future utility storm protection plans as well.

Subsection (2): Definitions

A storm protection plan is comprised of storm protection

programs. A program may include specific projects. Paragraph (2)(a) defines a

program as a category, type, or group of related storm protection projects that

is undertaken to enhance the utility’s existing infrastructure for the purpose

of reducing restoration costs and outage times and improving overall service

reliability. Paragraph (2)(b) defines a project as a specific activity designed

to enhance a specified portion of existing electric transmission or

distribution facilities for the purpose of reducing restoration costs and

outage times, and improving overall service reliability.

Paragraph (2)(c) identifies the “Transmission and

distribution facilities” that will be eligible for storm protection plans.

“Transmission and distribution facilities” are defined as “all utility owned

poles and fixtures, towers and fixtures, overhead conductors and devices,

substations and related facilities, land and land rights, roads and trails,

underground conduits, and underground conductors.”

FPL and Gulf

argue that the definition of “transmission and distribution facilities” should

be expanded to include additional types of assets, such as structures and

improvements, station equipment, underground conductors and devices, battery

storage equipment, meters and services. FPL also suggests the removal of

“substations and related facilities” from the definition because these assets

are included within the station equipment accounts.

TECO, DEF, and FPUC echo FPL’s suggestions to expand the

definition of “transmission and distribution facilities.” FPUC argues that

meters should be specifically enumerated in the definition of “transmission and

distribution facilities,” and DEF specifically suggests a change that would

explain the definition by including the language “and associated facilities.”

OPC comments that the definition of “transmission and

distribution facilities” should be narrowed to track the Federal Energy

Regulatory Commission’s Uniform System of Accounts (USOA) definitions of

“transmission and distribution facilities.” OPC argues the USOA definition

excludes meters, because the primary purpose of a meter is to measure

electricity delivery. According to OPC, a meter is therefore incidental and

ancillary to storm protection. Also, OPC argues battery storage assets should

not be included as transmission and distribution facilities for purposes

of storm protection because they are broadly categorized under the USOA as

production plant. Thus, OPC argues storage assets are not solely for resilience

against extreme weather.

Rule 25-6.030(3)(j), provides that the IOUs can submit in

its plan “[a]ny other factors the utility requests the Commission to consider.”

FPUC expresses concerns that this language could be narrowly construed to include

only factors pertaining to programs and projects consistent with the definition

of “transmission and distribution facilities.” FPUC’s concerns appear to be

based on a misunderstanding of the statute. The purpose of the statute is to

encourage programs and projects that protect the utility’s transmission and

distribution system. It does not require that every program or project entail a

physical change to the transmission and distribution system itself. Said

differently, staff intends for paragraph (3)(j) to be interpreted to encompass

factors pertaining to programs and projects that are designed to protect the

utility’s transmission and distribution facilities as that term is defined in

the rule.

Subsection (3): Contents of the Storm

Protection Plan

Subsection (3) provides the specific information that must

be provided in each storm protection plan, including descriptions of the

utility’s service area, the areas prioritized for enhancement, and any areas

where the utility has determined that enhancement of the utility’s existing

transmission and distribution facilities would not be feasible, reasonable, or

practical.

Subsection (3) also requires the utility to provide certain

cost estimates, such as an estimate of the annual jurisdictional revenue

requirements for each year of the storm protection plan and an estimate of rate

impacts for each of the first three years of the storm protection plan for

residential, commercial, and industrial customers. Paragraph (3)(e) requires that

for each of the first three years in an IOU’s storm protection plan the utility

provide a description of each proposed storm protection project that includes:

1.

The actual or estimated construction start and

completion dates;

2.

A description of the affected existing facilities,

including number and type(s) of customers served, historic service reliability

performance during extreme weather conditions, and how this data was used to

prioritize the proposed storm protection project; and

3.

A cost estimate including capital and operating

expenses; and

4.

A description of the criteria used to select and

prioritize proposed storm protection projects.

Paragraph (3)(f) requires the utility to provide a

description of its proposed vegetation management activities. The utility’s

description must include the projected frequency (trim cycle), the projected

miles of affected transmission and distribution overhead facilities, the

estimated annual labor and equipment costs for both utility and contractor

personnel, and a description of how the vegetation management activity will

reduce outage times and restoration costs due to extreme weather events.

Level of Project Detail Required in Storm

Protection Plans

The IOUs take issue with the requirement for project-level

information in years 2 and 3, arguing that it is not feasible or desirable for

the specific projects for years 2 and 3 to be detailed in the plan. Because projects

inevitably change due to a host of issues including access, customer

acceptance, and changing priorities, the IOUs argue that years 2 and 3 are

sufficiently detailed if the IOUs provide the type and number of projects and

program costs to support the development of annual rate-impact estimates for

the first 3 years. FPL suggests the following rule language in paragraph (3)(e)

instead of staff’s recommended rule language:

(e) For each of the first

three years in a utility’s Storm Protection Plan, the utility must provide the

following information:

1. For the first year of the

plan, a description of each proposed storm protection project that

includes:

i. 1. The actual or estimated

construction start and completion dates;

ii. 2. A description

of the affected existing facilities, including the number and type(s) of customers

served, historic service reliability performance during extreme weather events,

and how this data was used to prioritize the proposed storm protection project;

and

iii. 3. A cost

estimate including capital and operating expenses, both fixed and variable;

and

iv. 4. A description

of the criteria used to select and prioritize proposed storm protection

projects.

2. For the second and third

years of the plan, project related information such as estimated number and

cost of projects under a specific program, in sufficient detail, to allow the

development of preliminary estimates of rate impacts as required under

subsection 3(h) of this rule.

FPL suggests that project-level detail be provided

annually for the current year in the actual/estimated true-up filings under

Rule 25-6.031, F.A.C.

TECO also opposes project-level detail in years 2 and 3 in

the plan and suggests that the Commission consider the level of cost detail

found in the Demand-Side Management Plans as a benchmark for the cost detail

necessary in the storm protection plans. Likewise, DEF specifically cautioned

against rule language requiring project-level information in each of the first

3 years because such a requirement may result in petitions for rule waiver. According

to DEF, the requirement for 3 years of project-level data would force it to

either “create data that will be subject to extensive revision and [is without]

business purpose—an inefficient use of resources to both create and review—or

file for a rule waiver.” Moreover, all of the IOUs believe that project-level

shifts within an approved program should not constitute a modification that

requires Commission action.

FRF expresses support of project-level detail to ensure costs

are not double recovered. FRF commented at the workshop that the rule

should require extensive accounting data and more than just a description of

selection and prioritization. FRF suggests IOUs should be required to

demonstrate that selection and prioritization of all projects are based on

objective principles and benefits to customers.

OPC states that project-level details are necessary to

ensure that the costs being recovered through base rates are not also recovered

through the SPPCRC. OPC further states that “[g]iven the public interest in

protecting against storm damage, all IOUs should have specific plans with

detailed cost-tracking that comports with representations made to the

Commission and all stakeholders regarding what they have done, are continuing

to do and will do to continue storm protection efforts.” It also believes that

the Commission should “require each utility to submit information for the last

three years detailing all storm hardening projects that have been included in

the IOUs construction budgets including status completion.”

OPC suggests edits to the rule that allow for detailed

information for the first 3 years of any 10-year plan. OPC states that the

initial plan approval in particular should contain detailed project-by-project

information for amounts slated for recovery and include detail along the same

lines for the historical periods and for current and future periods covered by

the approved storm hardening plans that are in effect. According to OPC,

without sufficient detail in the plan and the clause filings, it will be difficult

to identify and differentiate the approved storm costs the IOUs are recovering

in base rates with current storm hardening plans versus the storm related costs

IOUs ask for cost recovery for in the SPPCRC. OPC also suggests that detailed

data is necessary to understand what costs are tied to settlement agreements

and thus necessary to ensure customers do not pay twice for the same costs.

FPL takes issue with OPC’s assertion that costs projected

under an IOU’s storm hardening plan that was previously approved prior to these

new storm protection plan rules should be treated automatically as already

recovered in base rates and thus excluded from cost recovery under the SPPCRC. FPL

states that it takes no position on whether the rules need a detailed mechanism

or protocol for determining a baseline to measure costs in the SPPCRC. However,

costs initially projected to be incurred pursuant to an approved storm protection

plan should be eligible for cost recovery under the SPPCRC.

The IOUs have the burden to prove that costs being

requested through the SPPCRC are not being recovered in base rates. As such, staff

believes that any petition for costs filed in the SPPCRC must evidence that the

utility is not seeking double recovery and therefore OPC’s concerns are more

appropriately addressed by the filing requirements in Rule 25-6.031, F.A.C.,

Storm Protection Plan Cost Recovery Clause, which is further discussed below.

With regards to project-level detail for all 3 years and as

previously discussed in the overarching themes section of the case background,

staff believes that project-level detail for years 1, 2, and 3 provides a

baseline for the Commission’s review and comparison of costs sought in the SPPCRC

from projects that were previously approved in a storm protection plan. This

information is also relevant to comply with subsections (4) and (5) of Section

366.96, F.S. This level of detail is necessary for the Commission to adequately

address the legislative requirement of Section 366.96(4), F.S. Also, without

project-level detail for all 3 years, the Commission would not have enough

information to make an informed decision to modify a plan pursuant to Section

366.96(5), F.S.

Whether Franchise Agreement Information Should

be Included in Storm Protection Plans

OPC argues that the storm protection plan should include

Franchise Agreements to ensure that programs or projects are not proposed or

modified to influence renewals. In response, DEF states such a provision would

be beyond the scope of Section 366.96, F.S., and would be information more

appropriately sought through discovery rather than the rule.

Staff’s draft rule requires that each utility provide a

description of the criteria used to select and prioritize proposed programs and

projects. Staff believes that this requirement will provide sufficient

information for vetting the basis of proposed programs and projects, including

franchise agreements. Thus, such specific criteria in the rule are unnecessary.

Subsection (4): Annual Status Report

Subsection (4) requires that each utility submit to the

Commission Clerk an annual status report on the utility’s storm protection plan

programs and projects. The rule provides that the annual status report must

identify all storm protection plan programs and projects completed in the prior

calendar year or planned for completion, provide actual costs and rate impacts

associated with completed programs and projects as compared to the estimated

costs and rate impacts for those programs and projects, and provide estimated costs

and rate impacts associated with programs and projects planned for completion

during the next year of the storm protection plan.

Rule 25-6.031, F.A.C., Storm Protection Plan

Cost Recovery Clause

Rule 25-6.031, F.A.C., addresses how an IOU may file a petition

for recovery of prudently incurred costs through the SPPCRC. Specifically, the

rule creates an annual clause proceeding, which consists of a true-up of the

previous year’s costs, a true-up and estimation for the current year’s costs,

and a projection of next year’s costs. The rule provides that costs recovered

in base rates may not be recovered through the clause.

Subsection (2): Simultaneous Filings

Subsection (2) allows an IOU to file a petition for

recovery of prudently incurred costs and reasonable projected costs through the

SPPCRC after its storm protection plan is filed with the Commission. FPL argues

that allowing a petition for cost recovery to be filed simultaneously with the

storm protection plan reasonably allows for conducting the clause on an annual

basis. OPC stated in the workshop that it would oppose simultaneous plan and

clause filings the first time the rules are implemented because it would be too

difficult to analyze base rates and incremental costs the first time. Recovery

of storm protection plan costs through the SPPCRC is not required by the statute

and is discretionary to the IOU.

Staff believes a simultaneous plan and clause petition

would allow for administrative efficiency and reduce regulatory lag. Therefore,

the rule allows an IOU to file a petition once its storm protection plan is

filed with the Commission.

Subsection (2) also provides that if the Commission

approves the utility’s storm protection plan with modifications, the utility has

15 business days to file an amended cost recovery petition and supporting

testimony reflecting the modifications. FPL suggests rule language that requires

an IOU to “promptly file an amended” clause petition in the event that the

Commission approves its storm protection plan with modifications. While staff

agrees in concept with allowing for prompt filings, staff believes that FPL’s

language is too ambiguous. It is staff’s belief that a timeline of 15 business

days conveys urgency while recognizing that some time will be needed for the

utility to draft and file an amended clause petition.

Subsection (3): Annual Hearing to Determine

Reasonableness of Projected Costs and Prudence of Actual Costs

Subsection (3) addresses the role of the annual cost

recovery proceeding in determining the reasonableness of an IOU’s projected

costs and the prudence of its actual costs to implement an approved storm protection

plan. The rule provides that an annual hearing to address petitions for

recovery of storm protection plan costs will be held and will be limited to

determining the reasonableness of projected storm protection plan costs, the

prudence of actual storm protection plan costs incurred by the utility, and to

establish storm protection plan cost recovery factors consistent with the requirements

of this rule.

In line with its position that storm protection plans

should not require the level of detailed information for years 2 and 3 of the

plans as required for year 1, FPL

proposes that the actual/estimated true-up filing in the cost recovery clause include

the project-level information. To accomplish this, FPL suggests that the

following language be added to subsection (3) of Rule 25-6.031:

The Commission shall determine the reasonableness

of the lists of projects (by applicable program) filed by the utility pursuant

to section (7)(b) of this rule based on whether such projects are consistent

with the program criteria for such projects approved by the Commission under

the utility’s Storm Protection Plan.

Staff disagrees with FPL’s suggestion that additional

language is required to clarify the standard that will be applied in the SPPCRC

hearings. Subsection (3) already notes that the Commission will determine the

reasonableness of projected costs of the storm protection plan, which would

necessarily entail a determination that the projects generating those costs are

consistent with the plan. Moreover, FPL’s suggested language seems to limit the

Commission’s reasonableness determination to only one review at the actual/estimated

true-up stage. The current language allows the Commission the flexibility to

make reasonableness reviews when necessary throughout the cost recovery process.

In its comments, OPC expresses a “fundamental concern”

about the timing of the SPPCRC hearing, advocating that the hearing take place

in the first 6 months of the year. OPC suggests that language be added to

subsection (3) of the rule to specify that the annual hearing under the rule

will be conducted no later than July 31 of each year after the calendar year in

which the first phase of the plan was approved. OPC believes that the SPPCRC

must be separated out from the other cost recovery clauses due to the amount of

time that OPC anticipates it will take to determine whether storm protection plan

costs are included in base rates and how such costs are to be determined.

FPL notes in its comments that applying the new clause

factors on a mid-year cycle could lead to customer confusion and would

introduce unnecessary complexity in the billing process. Although it has no

objection to leaving the procedural detail out of the rule and using an Order

Establishing Procedure to set all controlling dates, FPL provides a schedule in

its comments that essentially mirrors that of the NCRC, with a hearing taking

place in August/September and factors going into effect on January 1.

Unlike the Commission’s determination on the utility’s

storm protection plan, Section 366.96, F.S., does not include statutory

deadlines for the annual SPPCRC hearing. Thus, the Commission has full discretion

to determine the hearing dates for this clause proceeding. Staff recommends

that hearing dates for the proceeding should be determined by the Prehearing

Officer working in conjunction with the Chairman’s Office similar to the other

cost recovery clauses.

As discussed in the Case Background, staff envisions that

once Rule 25-6.031, F.A.C., becomes effective, the Commission will open a

docket to establish the SPPCRC, and the Prehearing Officer will issue an Order

Establishing Procedure to set forth all the controlling dates in the docket,

including the dates by which any requests for cost recovery for the year must

be filed. Staff also envisions that the SPPCRC will become a “roll-over” docket

like the Commission’s other cost recovery clause dockets.

Subsection (4): Deferred Accounting Treatment

Subsection (4) of the rule provides that costs recovered

through the clause will be trued-up in the clause, and the clause true-up

amounts will be afforded deferred accounting treatment at the 30-day commercial

paper rate. FPUC suggests that the phrase “over and under-recovery” be inserted

after the phrase “cost recovery true-up.” Staff disagrees because the presence

of a true-up event means either an over- or under-recovery event has occurred.

Thus, staff believes keeping only the phrase “true-up” adequately addresses the

occurrence of either an over- or under-recovery.

FPUC also suggests that additional language be added to

subsection (4) of the rule to address the regulatory treatment of deferred

capitalized expenses. Staff believes the rule does not need to address all

existing types of deferred accounting events. As currently drafted, the rule

requires information necessary to determine if a petition for cost recovery of

prudently incurred costs is consistent with an IOU’s approved storm protection plan.

The Commission must also receive enough information to ensure that the utility

is not recovering costs through the clause that it will also recover through

base rates. Staff believes the recommended rule language does this. Creating a

specific list of deferred capitalized expenses could only confuse rather than

clarify eligible expenses. Therefore, FPUC’s suggestion is not recommended.

Because OPC is opposed to any provisions in the rule which

allow cost recovery for projected costs as opposed to actually incurred costs, OPC

also took issue with subsection (4). OPC suggesting limiting the recovery of

costs related to variances caused by sales forecasting variances or changes in

the utility’s prices for services or equipment. Staff disagrees with OPC’s

suggestion for the reasons discussed in the first subsection in the section

discussing overarching themes.

Subsection (5): Treatment

of Subaccounts

Subsection (5) of the rule requires IOUs to maintain

subaccounts for costs subject to recovery to ensure separation of those costs

from costs not subject to recovery through the clause.

Subsection (6): Recoverable

Costs

Subsection (6) of the rule provides that an IOU’s petition

for recovery of costs prudently incurred to implement its storm protection plan

may include costs incurred after the filing of the utility’s storm protection plan.

The utility may recover the annual depreciation expense on capitalized storm

protection plan expenditures using the utility’s most recent

Commission-approved depreciation rates. Subsection (6) provides that the utility

may recover a return on the undepreciated balance of the costs calculated at

the utility’s weighted average cost of capital using the return on equity most

recently approved by the Commission. The rule requires that the utility submit

its final true-up of storm protection plan revenue requirements based on actual

costs for the prior year and previously filed costs and revenue requirements

for such prior year along with a description of the work actually performed

during such year.

DEF, TECO, and FPUC argue that subsection (6) should

specifically allow for the recovery through the SPPCRC of costs incurred

developing a storm protection plan. Read together, paragraph (2)(c) and

subsection (7) of Section 366.96, F.S., allow for the recovery of “reasonable

and prudent costs to implement an

approved transmission and distribution storm protection plan.” The plain language

of Section 366.96, F.S., allows an IOU to recover the costs of implementing a storm protection plan,

not developing it.

Paragraph (6)(b) of the rule states that the utility is

not permitted to recover costs through the SPPCRC that are included for

recovery through base rates or any other cost recovery mechanism. OPC suggests

adding language that states that the “utility must file detailed information

consistent with Rule 25-6.030(g), F.A.C., as a part of meeting its burden of

demonstrating that clause-eligible costs are not being recovered in base rates

or any other cost recovery mechanism.” Staff assumes that OPC’s rule reference

is for the purpose of requiring an estimate of the annual jurisdictional

revenue requirements for each year of the storm protection plan. Rule

25-6.030(3)(g), F.A.C., requires an IOU to provide an estimate of the annual

jurisdictional revenue requirements for each year of the storm protection plan,

so it is unnecessary for Rule 25-6.031, F.A.C., to restate that requirement.

Moreover, staff believes each utility’s demonstration that its costs are

excluded from other recovery mechanisms will be adequately vetted through the

clause hearing process pursuant to the filing requirements of Rule 25-6.031,

F.A.C.

OPC also suggests that the term “mid-point” be inserted

in paragraph (6)(c) after “equity” and

before “most recently approved by the Commission.” Staff believes this change

is not needed because the return on equity approved by the Commission is used

as the midpoint of a range of reasonableness.

In addition, FPL proposes the

following language as paragraph (6)(d): “The utility may request recovery

of cost of removal and any remaining investment associated with retirements of

Storm Protection Plan investments recovered under the clause.” Staff has two

concerns about the proposed language. First, staff is unsure how FPL or

other IOUs may determine remaining investment for any one asset. Under Rule

25-6.0436 Depreciation, F.A.C., and

Rule 25-6.04361 Subcategorization of Electric

Plant for Depreciation Studies and Rate Design, F.A.C., many assets,

especially transmission and distribution assets, are grouped in mass property

accounts, wherein asset age data for any single asset is unknown, thus the

remaining investment in that particular asset is also unknown. Staff believes

the methodology used to determine the net unrecovered investment amount for a

type of asset replaced in a storm protection plan project must take into

account the past recovery of both short and long lived assets relative to

average service life. Ideally, such a method would be reflective of both the IOUs’

gains received and losses incurred when such assets are removed, yielding net

unrecovered investment. Second, the cost of removal is reflected in current

depreciation rates for all assets, so some portion of removal costs for all

current assets have already been recovered in base rates. Staff is concerned

that this is not reflected in FPL’s proposed rule language, which appears to

allow for recovery of all removal costs through the clause. For these reasons,

staff does not recommend adding FPL’s recommended language.

Subsection (7): Cost Recovery Mechanism and Filing

Requirements

Subsection (7) addresses the filing requirements for the SPPCRC

and describes the mechanism used to project and true-up costs incurred to

implement the utility’s storm protection plan. Paragraphs (7)(a)–(c) describe the

same three-step mechanism used in other clauses. The three steps are referred

to in those paragraphs as the Final True-up for Previous Year, the Estimated

True-up for Current Year, and the Projected Costs for Subsequent Year. In other

words, the recovery of incurred costs is a moving three-year process that begins

with the projection of future costs and ends with the final true-up of those

projected costs. Paragraphs (7)(a)–(d) require the utility to submit data

sufficient to allow the Commission to project future costs and determine

incurred costs as that data becomes available. Paragraph (7)(d) also requires

the utility to submit data establishing sales forecasting variances and changes

in the utility’s price of service and equipment. Paragraph (7)(e) requires the

utility to submit its proposed factors and effective 12-month billing period.

OPC suggests striking paragraphs (7)(a), (7)(b), and

(7)(c) to remove the filing requirements that true-up projected costs to actual

incurred costs as well as the associated revenue requirements on a moving

three-year basis. In its comments, OPC asserted that there is a lack of

statutory authority for projected cost recovery as opposed to costs that have

been incurred. OPC recommends striking paragraphs (7)(a) through (c) to conform

the rule to that argument. As previously discussed, staff disagrees with OPC’s

premise that the rules should not allow for projected costs. Thus, staff

believes there is no need to change subsection (7).

FPL suggests that paragraph (7)(b) of the rule be revised

to show that this filing would include a listing of project-level information

for the current year, consistent with its position that storm protection plans

should not require the level of detailed information for years 2 and 3 of the

plans, as required for year 1 (see staff’s

discussion on subsection (3)(e) of Rule 25-6.030). However, FPL did not propose

comparable language for paragraph (7)(c) addressing projections or for true-up

filings in paragraph (7)(a). FPL did not state what was unique about the

current year filings of paragraph (7)(b) of the rule that necessitated the

added language. As previously noted in the analysis for the storm protection plan

rule, staff believes each utility’s respective petitions should require a

certain level of detail to support the utility’s respective requests in the

petitions for cost recovery in the clause. The recommended rule language of

paragraph (7)(b) adequately provides the filing requirements consistent with this

belief. Thus, the suggested changes are not necessary.

OPC also suggests editing paragraph (7)(e) to make the word “factors” singular. But each

utility has multiple rate classes, and each rate class has a unique factor. Therefore,

multiple factors will be set for each utility. Staff therefore does not

recommend incorporation of the editorial suggestion.

Subsection (8): Effect

on Subsequent Rate Proceeding

Subsection (8) provides that recovery of costs under this

rule does not preclude an IOU from proposing inclusion of unrecovered storm protection

plan implementation costs in base rates in a subsequent rate proceeding. FPUC and FPL suggest subsection (8) should

specifically identify or list for inclusion the “future revenue requirements

for existing storm protection plan investments” as eligible costs for future

base rate recovery. Staff disagrees. Subsections (2), (6), and (8) of the draft

rule allow for recovery of costs prudently incurred to implement an IOU’s storm

protection plan. The rule allows for recovery of costs prudently incurred after

the filing of the utility’s plan that implement the utility’s storm protection plan

and that were costs not previously approved in another proceeding. Because Rule

25-6.031, F.S., already covers all types of expenses appropriate for clause

recovery, there is no need for the rule to include a specific or enumerated

list of the types of costs as suggested by the IOUs. Listing types of costs could

confuse rather than clarify what is permitted for recovery under the rule.

Other Issues

FRF suggests that for transparency purposes, the rules

should require the storm protection plan cost recovery charges be shown as a

separate line item on customers’ bills. TECO recommends that to avoid customer

confusion, storm protection plan cost recovery charges be calculated separately

but incorporated in the energy charge line item that includes the other clauses

on customers’ bills.

Section 366.96, F.S., does not mandate that storm

protection plan cost recovery charges be shown as a separate line item on

customers’ bills. The statute is silent on the matter. Due to billing system

reprograming, the IOUs state they would incur additional costs, which would ultimately

be passed on to the customers if the Commission required that the storm

protection plan charges be a separate line item. On the other hand, the IOUs

say that no additional billing charges will be incurred as long as the storm

protection plan charges are incorporated into the non-fuel energy charge on

customers’ bills.

Staff believes each utility’s costs, and ultimately the

customers’ costs, would be higher if the Commission required a separate line

item on customers’ bills. The customers’ bills will include approved storm

protection plan cost recovery charges whether they are reflected as line items

or included in the energy charge line on the bill. Staff believes that adding

additional expenses for the sake of transparency is unnecessary and would be outweighed

by lower costs to the customers. Thus, staff believes the rules should not

mandate that the storm protection plan cost recovery charges be shown as a

separate line item on customers’ bills.

FRF also suggests adding a third rule, Rule 25-6.0301,

F.A.C., which would require an IOU to seek Commission approval for changes to

its storm protection plan that result in changes to the total cost of the plan of

more than a certain percentage of that total. Staff does not believe that such

a rule is necessary. Each utility will have to report and explain cost

variances in the SPPCRC proceedings. In these proceedings, the utility will

have to show cost changes and the cause of those changes. IOUs will also have

to show that all of their costs were prudently incurred to implement the

utility’s approved plan. In other words, requiring IOUs to seek the

Commission’s approval of a storm protection plan modification solely on the

basis of a cost variance is unduly duplicative of the scrutiny that will be a

part of the SPPCRC.

Minor Violation

Rules Certification

Pursuant to Section 120.695, F.S., beginning July 1, 2017,

for each rule filed for adoption, the agency head must certify whether any part

of the rule is designated as a rule the violation of which would be a minor

violation. Under Section 120.695(2)(b), F.S., a violation of a rule is minor if

it does not result in economic or physical harm to a person or adversely affect

the public health, safety, or welfare or create a significant threat of such

harm. Rule 25-6.030, F.A.C., and Rule 25-6.031, F.A.C., will be minor violation

rules, as a violation of these rules will not result in economic or physical

harm to a person or have an adverse effect on the public health, safety, or

welfare or create a significant threat of such harm. Therefore, for the

purposes of filing the rules for adoption with the Department of State, staff

recommends that the Commission certify proposed Rule 25-6.030 and 25-6.031,

F.A.C., as minor violation rules.

Statement of

Estimated Regulatory Costs

Pursuant to Section 120.54(3)(b), F.S., agencies are

encouraged to prepare a statement of estimated regulatory costs (SERC) before

the adoption, amendment, or repeal of any rule. The SERC is appended as

Attachment B to this recommendation. The SERC analysis also includes whether

the rules are likely to have an adverse impact on growth, private sector job

creation or employment, or private sector investment in excess of $1 million in

the aggregate within five years after implementation.

The SERC concludes that any economic impacts that might be

incurred by affected entities would be a result of the statute rather than the

rules. Staff believes that the new rules will not likely directly or indirectly

increase regulatory costs in excess of $200,000 in the aggregate in Florida

within one year after implementation. Staff notes that the IOUs, in response to

staff’s SERC data request, provided potential financial impacts resulting from

specific requirements of Chapter 366.96, F.S.

Further, the SERC concludes that the rules will not likely

have an adverse impact on economic growth, private-sector job creation or

employment, private sector investment, business competitiveness, productivity,

or innovation in excess of $1 million in the aggregate within five years of

implementation. Thus, the new rules do not require legislative ratification

pursuant to Section 120.541(3), F.S.

In addition, the SERC states that the rules will have no

adverse impact on small businesses, small cities, or small counties. The rules

will have minimal impact on state and local revenues and transactional costs. Any

implementation or enforcement costs on the Commission will be offset by the

additional staff positions and funding provided under the new law. No regulatory

alternatives were submitted pursuant to Section 120.541(1)(a), F.S. None of the

impact/cost criteria established in Section 120.541(2)(a), F.S., will be

exceeded as a result of the recommended rules.

Conclusion

Based on the foregoing, staff recommends the Commission

propose the adoption of Rules 25-6.030 and 25-6.031, F.A.C., as set forth in

Attachment A. Staff also recommends that the Commission certify Rules 25-6.030

and 25-6.031, F.A.C., as a minor violation rules.

Issue 2:

Should this docket be closed?

Recommendation:

Yes. If no requests for hearing or comments are

filed, the rules should be filed with the Department of State, and the docket

should be closed. (Harper, A. King)

Staff Analysis:

If no requests for hearing or comments are filed,

the rules may be filed with the Department of State and the docket closed. When

these rules become effective, staff will bring a recommendation in a separate

docket for the Commission’s consideration on any other existing Commission

rules that need to be amended or repealed.