|

State of Florida

|

Public Service Commission

Capital Circle Office Center ● 2540 Shumard

Oak Boulevard

Tallahassee, Florida 32399-0850

-M-E-M-O-R-A-N-D-U-M-

|

|

DATE:

|

April 22, 2021

|

|

TO:

|

Office of Commission Clerk (Teitzman)

|

|

FROM:

|

Office of the General Counsel (Harper) SMC

Division of Accounting

and Finance (Fletcher, Mouring) ALM

Division of Economics

(Coston, Guffey) JGH

|

|

RE:

|

Docket No. 20210062-OT – Proposed amendment

of Rule 25-6.0143, F.A.C., Use of Accumulated Provision Accounts 228.1,

228.2, and 228.4 and proposed new Rule 25-7.0143, F.A.C., Use of Accumulated

Provision Accounts 228.1, 228.2, and 228.4.

|

|

AGENDA:

|

05/04/21 – Regular Agenda – Rule Proposal – Interested Persons May

Participate

|

|

COMMISSIONERS ASSIGNED:

|

All Commissioners

|

|

PREHEARING OFFICER:

|

Fay

|

|

RULE STATUS:

|

Proposal May Be Deferred

|

|

SPECIAL INSTRUCTIONS:

|

None

|

|

|

|

|

Case Background

Rule 25-6.0143, Florida

Administrative Code (F.A.C.), Use of Accumulated Provision Accounts 228.1,

228.2, and 228.4., provides the

standards for the application of Accumulated Provision Accounts 228.1, 228.2,

and 228.4 for investor-owned electric

utilities. The Commission does not currently have a corresponding rule on this

subject for investor-owned natural gas utilities. Adoption of new Rule

25-7.0143, F.A.C., Use of Accumulated Provision Accounts 228.1, 228.2,

and 228.4, would create a new rule for

the standards for the application of Accumulated Provision Accounts 228.1,

228.2, and 228.4 for natural gas utilities.

The focus of this rulemaking is to amend Rule 25-6.0143, F.A.C., for clarity and specificity. Rule

25-7.0143, F.A.C., is being

created to provide an industry-specific standard for the application of

Accumulated Provision Accounts 228.1, 228.2, and 228.4 for the natural gas

utilities. In general, the

amendment of Rule 25-6.0143, F.A.C., and the adoption of new Rule 25-7.0143,

F.A.C., is intended to provide requirements for the application of

Accumulated Provision Accounts 228.1, 228.2, and 228.4, specifically as they apply to storm-related

damages.

The

Notice of Development of Rulemaking for Rule 25-6.0143, F.A.C., was published in the June 7, 2019 edition of the

Florida Administrative Register, Volume 45, No. 111, in conjunction with the

Commission’s rulemaking on Rules 25-6.030 and 25-6.031, F.A.C., the storm

protection plan and storm protection plan cost recovery clause rulemaking.

During the development of those rules, staff determined that Rule 25-6.0143, F.A.C., needed to be updated.

In

the course of considering potential amendments to Rule 25-6.0143, F.A.C., staff

determined that the gas industry needed a rule similar to Rule 25-6.0143, F.A.C.

Accordingly, a Notice of Development of Rulemaking for new Rule 25-7.0143, F.A.C., was published

in the June 10, 2020 edition of the Florida Administrative Register, Volume 46, No. 113.

A

rule development workshop on both rules was held on June 29, 2020.

Representatives from Florida Power & Light Company (FPL), Tampa Electric

Company (TECO), Duke Energy Florida, LLC (DEF), Gulf Power Company (Gulf),

Florida Public Utilities Company (FPUC), Florida City Gas (FCG), Peoples Gas

System (PGS), and the Office of Public Counsel (OPC) participated at the

workshop and submitted post-workshop comments.

This

recommendation addresses whether the Commission should propose the amendment of

Rule 25-6.0143, F.A.C.,

and propose the adoption of new Rule 25-7.0143, F.A.C. The Commission

has jurisdiction pursuant to Section 366.05(1), Florida

Statutes (F.S.).

Discussion

of Issues

Issue 1:

Should the Commission propose the amendment of Rule 25-6.0143, F.A.C., Use of Accumulated

Provision Accounts 228.1, 228.2, and 228.4., and propose the adoption of Rule

25-7.0143, F.A.C., Use of Accumulated Provision Accounts 228.1, 228.2, and

228.4?

Recommendation:

Yes. The Commission should propose the amendment of

Rule

25-6.0143, F.A.C., and propose

the adoption of Rule 25-7.0143, F.A.C., as set forth in Attachment

A. The Commission should also certify Rules 25-6.0143 and 25-7.0143, F.A.C.,

as minor violation rules. (Mouring, Harper, Guffey)

Staff Analysis:

Staff

recommends that the Commission amend Rule 25-6.0143, F.A.C., and adopt new Rule 25-7.0143, F.A.C., as set forth

in Attachment A. Staff’s recommended language for Rule 25-7.0143, F.A.C.,

generally mirrors the Commission’s current use of accumulated provision accounts

rule for investor-owned electric utilities. Both rules

address the categories of storm-related costs eligible for certain accounting.

As such, the

recommended amendments discussed below for Rule 25-6.0143, F.A.C., are also

reflected in staff’s recommended language for Rule 25-7.0143, F.A.C.

Rule

25-7.0143, F.A.C.

Draft

Rule 25-7.0143, F.A.C., is virtually identical to the electric rule, Rule

25-6.0143, F.A.C., in that both rules address the storm related costs that will

be allowed to be charged to the reserve under the Incremental Cost and

Capitalization Approach (ICCA) methodology.

Also, draft Rule 25-7.0143, F.A.C., provides an accounting mechanism for

probable liability that is not covered by insurance and a “catch-all” account

for operating provisions that are not covered elsewhere in the rule. This

account must be maintained in such a manner as to show the amount of each

separate provision established by the utility and the nature and amounts of the

debits and credits.

In

addition, draft Rule 25-7.0143, F.A.C., requires the utility to show the level

and annual accrual rate for each account listed in the rule so it can be

evaluated at the time of a rate proceeding and adjusted as necessary. Pursuant

to the draft rule, a utility may petition the Commission for a change in the

provision level and accrual of a certain account outside a rate proceeding

under certain, specified circumstances, but a utility may not fund any account

listed in the rule unless the Commission approves such funding.

Subsection

(1) of Both Rules

Subsection

(1) of draft Rules 25-6.0143 and 25.7.0143, F.A.C., contain provisions for an

account to provide for losses through accident, fire, flood, storms, nuclear

accidents and similar type hazards to the utility’s own property or property

leased from others, which is not covered by insurance. Staff recommends

updating this subsection of the rules to require a utility to notify the

Commission Clerk in writing for each incident expected to exceed 1.5 percent of

jurisdictional revenues for the most recent calendar year.

Staff also recommends updating subsection

(1) in Rule 25-6.0143, F.A.C., and including a provision in new Rule 25-7.0143,

F.AC., for the storm-related costs that will be allowed to be charged to the

reserve under the ICCA methodology. For each of the identified accounts, a

calculation is made to compare the actual average costs for a specific calendar

month to the actual average costs of that same month for each of the previous

three years. The actual costs for a specific calendar month that are in excess

of actual average costs of that same month for each of the previous three

years, would be identified as incremental costs.

For example, staff recommends that rule language be included to address

contract labor and payroll expenses incurred in storm restoration activities

and that such costs must be incurred in any month in which storm damage

restoration activities are conducted. Staff recommends similar clarifications

and rule language be added to address the fuel costs for both company and

contractor vehicles used in storm restoration activities, as well as the

vegetation management costs that are specifically related to storm restoration

activities for the utilities. For all of these cost categories, staff’s

recommended rule language requires that the costs must be greater than the

actual monthly average of contract labor or payroll costs charged to operation

and maintenance expense for the same month in the three previous calendar

years, and each adjustment must be accompanied by a detailed explanation of the

nature of the adjustment. Finally, staff is also recommending an added

“catch-all” provision to the rules, which provides that for any other costs or

expenses not specifically identified in the rules but that are directly and

solely attributable to a storm restoration event, such costs must be explained.

With

regard to the payroll costs, DEF commented that staff’s draft language in

Subsection (1) of Rule 25-6.0143, F.A.C., is unclear as to which payroll

expenses were eligible. It is staff’s intention that the rule language allow

for all payroll and payroll-related

costs, including overtime payroll, to be eligible. Staff believes the rule as

reflected in Attachment A is sufficient to address this point. The other stakeholders

agreed that staff’s recommended language was sufficient and clear in this

regard.

Minor Violation Rules Certification

Pursuant

to Section 120.695, F.S., as of July 1, 2017, the agency head shall certify

whether any part of each rule filed for adoption is designated as a minor

violation rule. A minor violation rule is a rule that would not result in

economic or physical harm to a person or an adverse effect on the public

health, safety, or welfare or create a significant threat of such harm when

violated. Staff recommends that the Commission certify Rule 25-6.0143, F.A.C., and

Rule 25-7.0143, F.A.C., as minor violation rules.

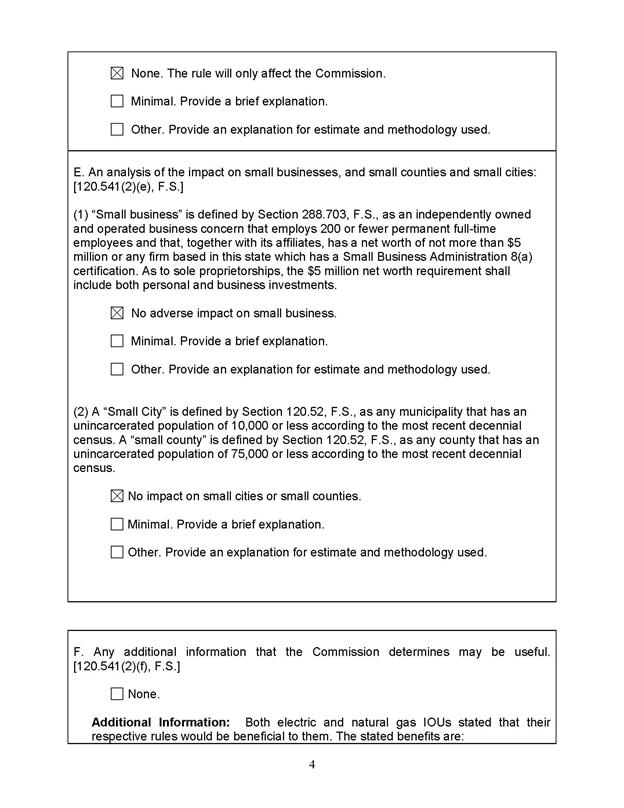

Statement of Estimated Regulatory Costs

Pursuant to Section

120.54(3)(b)1., F.S., agencies are encouraged to prepare a statement of

estimated regulatory costs (SERC) before the adoption, amendment, or repeal of

any rule. A SERC was prepared for this

rulemaking and is appended as Attachment B. As required by Section

120.541(2)(a)1., F.S., the SERC analysis includes whether the rule amendments and

rule adoption are likely to have an adverse impact on economic growth, private

sector job creation or employment, or private sector investment in excess of $1

million in the aggregate within five years after implementation. Staff notes

that none of the impact/cost criteria will be exceeded as a result of the

recommended amendments to Rule 25-6.0143 or the adoption new Rule 25-7.0143.

Based

on the utilities’ responses to data requests and discussions with technical

staff that oversee the accumulated provision rules, the recommended proposed

rule amendments and proposed new rule will not likely increase regulatory

costs, as contemplated by Section 120.541, F.S., including any transactional

costs or have an adverse impact on business competitiveness, productivity, or

innovation in excess of $1 million in the aggregate within five years of

implementation. The proposed new rule and rule amendments would not potentially

have adverse impacts on small businesses, would have no implementation cost to

the Commission or other state and local government entities, and would have no

negative impact on small cities or counties.

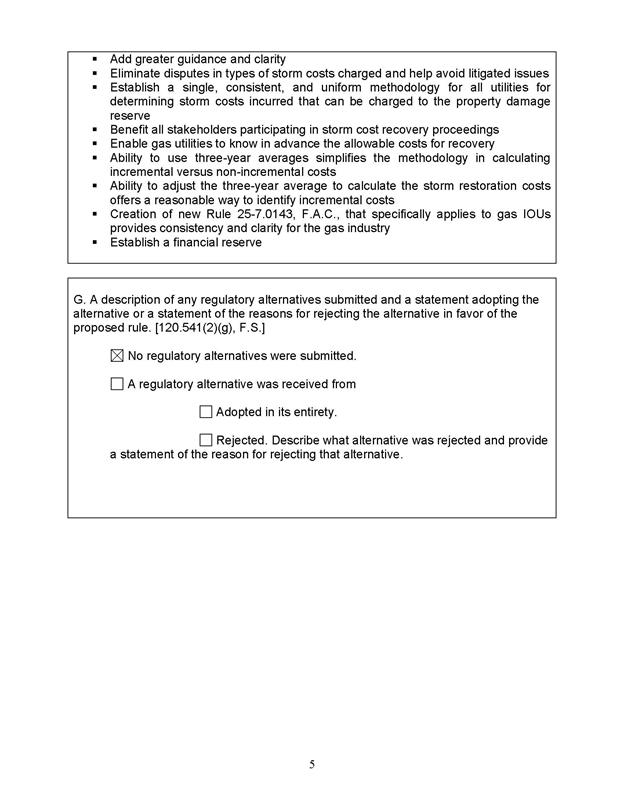

No

regulatory alternatives were submitted pursuant to Section 120.541(1)(g), F.S.

The SERC concludes that none of the impacts/cost criteria established in

Sections 120.541(2)(a), (c), (d), and (e), F.S., will be exceeded as a result

of the proposed rule amendments or the adoption of the new rule.

Conclusion

The Commission should propose the amendment of Rule

25-6.0143, F.A.C., and the adoption of Rule 25-7.0143, F.A.C., as set forth in

Attachment A. The Commission should certify Rule 25-6.0143, F.A.C., and Rule

25-7.0143, F.A.C., as minor violation rules.

Issue 2:

Should this docket be closed?

Recommendation:

Yes. If no requests for hearing, information

regarding the SERC, proposals for a lower cost regulatory alternative, or JAPC

comments are filed, the rules should be filed with the Department of State, and

the docket should be closed. (Harper)

Staff Analysis:

If no requests for hearing, information regarding

the SERC, proposals for a lower cost regulatory alternative, or JAPC comments

are filed, the rules should be filed with the Department of State, and the

docket should be closed.

25-6.0143 Use of Accumulated Provision

Accounts 228.1, 228.2, and 228.4.

(1)

Account No. 228.1 Accumulated Provision for Property Insurance.

(a)

This account may be established to provide for losses through accident, fire,

flood, storms, nuclear accidents and similar type hazards to the utility’s own

property or property leased from others, which is not covered by insurance.

This account would also include provisions for the deductible amounts contained

in property loss insurance policies held by the utility as well as

retrospective premium assessments stemming from nuclear accidents under various

insurance programs covering nuclear generating plants. A schedule of risks

covered must shall be maintained, giving a description of the

property involved, the character of risks covered and the accrual rates used.

(b)

Except as provided in paragraphs (1)(f), (1)(g) and (1)(h) charges to this

account must shall be made for all occurrences in accordance with

the schedule of risks to be covered which are not covered by insurance.

Recoveries, insurance proceeds or reimbursements for losses charged to this

account must shall be credited to the account.

(c)

A separate subaccount must shall be established for that portion

of Account No. 228.1 which is designated to cover storm-related damages to the

utility’s own property or property leased from others that is not covered by

insurance. The records supporting the entries to this account must shall

be so kept that the utility can furnish full information as to each storm event

included in this account.

(d)

In determining the costs to be charged to cover storm-related damages, the

utility must shall use an Incremental Cost and Capitalization

Approach methodology (ICCA). Under the ICCA methodology, the costs charged to

cover storm-related damages must shall exclude those costs that

normally would be charged to non-cost recovery clause operating expenses in the

absence of a storm. Under the ICCA methodology for determining the allowable

costs to be charged to cover storm-related damages, the utility will be allowed

to charge to Account No. 228.1 costs that are incremental to costs normally

charged to non-cost recovery clause operating expenses in the absence of a

storm. All costs charged to Account 228.1 are subject to review for prudence

and reasonableness by the Commission. In addition, capital expenditures for the

removal, retirement and replacement of damaged facilities charged to cover

storm-related damages must shall exclude the normal cost for the

removal, retirement and replacement of those facilities in the absence of a

storm. The utility must shall notify the Director of the

Commission Clerk in writing for each incident expected to exceed 1.5 percent

of jurisdictional revenues for the most recent calendar year $10 million.

(e)

The types of storm related costs allowed to be charged to the reserve under the

ICCA methodology include, but are not limited to, the following:

1.

Additional contract labor hired for storm restoration activities incurred in

any month in which storm damage restoration activities are conducted, that are

greater than the actual monthly average of contract labor costs charged to

operation and maintenance expense for the same month in the three previous

calendar years. The utility may adjust historical monthly contract labor costs

charged to operation and maintenance expense from calculated monthly average.

Each adjustment shall be accompanied by a detailed explanation of the nature

and derivation of the adjustment;

2.

Logistics costs of providing meals, lodging, and linens for tents and other

staging areas;

3.

Transportation of crews and other personnel for storm restoration;

4.

Vehicle costs for vehicles specifically rented for storm restoration activities;

5.

Waste management costs specifically related to storm restoration activities;

6.

Rental equipment specifically related to storm restoration activities;

7.

Materials and supplies used to repair and restore service and facilities to

pre-storm condition, such as poles, transformers, meters, light fixtures, wire,

and other electrical equipment, excluding those costs that normally would be

charged to non-cost recovery clause operating expenses in the absence of a

storm;

8.

Payroll Overtime payroll and payroll-related costs for utility

personnel included in storm restoration activities incurred in any month in

which storm damage restoration activities are conducted, that are greater than

the actual monthly average of payroll and payroll-related costs charged to

operation and maintenance expense for the same month in the previous three

calendar years. The utility may adjust historical monthly payroll and

payroll-related costs charged to operation and maintenance expense from

calculated monthly average. Each adjustment shall be accompanied by a detailed

explanation of the nature and derivation of the adjustment;

9.

Fuel cost for company and contractor vehicles used in storm restoration

activities incurred in any month in which storm damage restoration

activities are conducted, that are greater than the actual monthly average of fuel

costs charged to operation and maintenance expense for the same month in the

previous three calendar years. The utility may adjust historical monthly fuel

costs charged to operation and maintenance expense from calculated monthly

average. Each adjustment shall be accompanied by a detailed explanation of the

nature and derivation of the adjustment; and

10.

Cost of public service announcements regarding key storm-related issues, such

as safety and service restoration estimates;.

11.

Vegetation management costs specifically related to storm restoration

activities incurred in any month in which storm damage restoration activities

are conducted, that are greater than the actual monthly average of vegetation

management costs charged to operation and maintenance expense for the same

month in the previous three calendar years. The utility may adjust historical monthly

vegetation management costs charged to operation and maintenance expense from

calculated monthly average. Each adjustment shall be accompanied by a detailed

explanation of the nature and derivation of the adjustment; and

12.

Other costs or expenses not specifically identified in paragraph (1)(e)1.

through (1)(e)11. that are directly and solely attributable to a storm

restoration event.

(f)

The types of storm related costs prohibited from being charged to the reserve

under the ICCA methodology include, but are not limited to, the

following:

1.

Base rate recoverable regular payroll and regular-payroll related costs for

utility managerial and non-managerial personnel;

1.2.

Bonuses or any other special compensation for utility personnel not eligible

for overtime pay;

2.3.

Base rate recoverable Ddepreciation expenses, insurance costs

and lease expenses for utility-owned or utility-leased vehicles and aircraft;

3.

4. Utility employee assistance costs;

4.5.

Utility employee training costs incurred prior to 72 hours before the storm

event;

5.6.Utility

advertising, media relations or public relations costs, except for public

service announcements regarding key storm-related issues as listed above in

subparagraph (1)(e)10.;

6.7.

Utility call center and customer service costs, except for non-budgeted

overtime or other non-budgeted incremental costs associated with the storm

event;

8.

Tree trimming expenses, incurred in any month in which storm damage restoration

activities are conducted, that are less than the actual monthly average of tree

trimming costs charged to operation and maintenance expense for the same month

in the three previous calendar years;

7.9.

Utility lost revenues from services not provided; and

8.10.

Replenishment of the utility’s materials and supplies inventories.

(g)

Under the ICCA methodology for determining the allowable costs to be charged to

cover storm-related damages, certain costs may be charged to Account 228.1 only

after review and approval by the Commission. Prior to the Commission’s

determination of the appropriateness of including such costs in Account No.

228.1, the costs may be deferred in Account No. 186, Miscellaneous Deferred

Debits. The deferred costs must be incurred prior to June 1 of the year

following the storm event. By September 30 a utility must shall

file a petition for the disposition of any costs deferred prior to June 1 of

the year following the storm event giving rise to the deferred costs. These

costs include, but are not limited to, the following:

1.

Costs of normal non-storm related activities which must be performed by

employees or contractors not assigned to storm damage restoration activities

(“back-fill work”) or normal non-storm related activities which must be

performed following the restoration of service after a storm by an employee or

contractor assigned to storm damage restoration activities in addition to the

employee’s or contractor’s regular activities (“catch-up work”); and

2.

Uncollectible accounts expenses.

(h)

A utility may, at its own option, charge storm-related costs as operating

expenses rather than charging them to Account No. 228.1. The utility must

shall notify the Director of the Commission Clerk in writing and

provide a schedule of the amounts charged to operating expenses for each

incident exceeding 0.5 percent of jurisdictional revenues for the most

recent calendar year $5 million. The schedule must shall

be filed annually by February 15 of each year for information pertaining to the

previous calendar year.

(i)

If the charges to Account No. 228.1 exceed the account balance, the excess must

shall be carried as a debit balance in Account No. 182.3 228.1

and no request for a deferral of the excess or for the establishment of a

regulatory asset is necessary.

(j)

A utility may petition the Commission for the recovery of a debit balance in

Account No. 182.3 discussed in paragraph (1)(i) 228.1 plus an

amount to replenish the storm reserve through a surcharge, securitization or

other cost recovery mechanism.

(k)

A utility must shall not establish or change an annual accrual

amount or a target accumulated balance amount for Account No. 228.1 without

prior Commission approval.

(l)

Each utility must shall file a Storm Damage Self-Insurance

Reserve Study (Study) with the Commission Clerk by January 15, 2011 and at

least once every 5 years thereafter from the submission date of the previously

filed study. A Study must shall be filed whenever the utility is

seeking a change to either the target accumulated balance or the annual accrual

amount for Account No. 228.1. At a minimum, the Study must shall

include data for determining a target balance for, and the annual accrual

amount to, Account No. 228.1.

(m)

Each utility must shall file a report with the Director of

the Commission Clerk providing information concerning its efforts to obtain

commercial insurance for its transmission and distribution facilities and any

other programs or proposals that were considered. The report must shall

also include a summary of the amounts recorded in Account 228.1. The report must

shall be filed annually by February 15 of each year for information

pertaining to the previous calendar year.

(2)

Account No. 228.2 Accumulated Provision for Injuries and Damages.

(a)

This account may be established to meet the probable liability, not covered by

insurance, for deaths or injuries to employees or others and for damages to

property neither owned nor held under lease by the utility. When liability for

any injury or damage is admitted or settled by the utility either voluntarily

or because of the decision of a Court or other lawful authority, such as a

workman’s compensation board, the admitted liability or the amount of the

settlement must shall be charged to this account.

(b)

Charges to this account must shall be made for all losses

covered. Detailed supporting records of charges made to this account must

shall be maintained in such a way that the year the event occurred which

gave rise to the loss can be associated with the settlement. Recoveries or

reimbursements for losses charged to the account must shall be

credited to the account.

(3)

Account No. 228.4 Accumulated Miscellaneous Operating Provisions.

(a)

This account may be established for operating provisions which are not covered

elsewhere. This account must shall be maintained in such a manner

as to show the amount of each separate provision established by the utility and

the nature and amounts of the debits and credits thereto. Each separate

provision must shall be identified as to purpose and the specific

events to be charged to the account to ensure that all such events and only

those events are charged to the provision accounts.

(b)

Charges to this account must shall be made for all costs or

losses covered. Recoveries or reimbursements for amounts charged to this

account must shall be credited hereto.

(4)(a)

The provision level and annual accrual rate for each account listed in

subsections (1) through (3) must shall be evaluated at the time

of a rate proceeding and adjusted as necessary. However, a utility may petition

the Commission for a change in the provision level and accrual outside a rate

proceeding.

(b)

If a utility elects to use any of the above listed accumulated provision

accounts, each and every loss or cost which is covered by the account must

shall be charged to that account and must shall not be

charged directly to expenses except as provided for in paragraphs (1)(f),

(1)(g) and (1)(h). Charges must shall be made to accumulated

provision accounts regardless of the balance in those accounts.

(c)

No utility must shall fund any account listed in subsections (1)

through (3) unless the Commission approves such funding. Existing funded provisions

which have not been approved by the Commission must shall be

credited by the amount of the funded balance with a corresponding debit to the

appropriate current asset account, resulting in an unfunded provision.

Rulemaking

Authority 366.05(1) FS. Law Implemented 350.115, 366.04(2)(a) FS. History–New

3-17-88, Amended 6-11-07,___________.

25-7.0143 Use of Accumulated Provision

Accounts 228.1, 228.2, and 228.4.

(1)

Account No. 228.1 Accumulated Provision for Property Insurance.

(a)

This account may be established to provide for losses through accident, fire,

flood, storms and similar type hazards to the utility’s own property or

property leased from others, which is not covered by insurance. A schedule of

risks covered must be maintained, giving a description of the property

involved, the character of risks covered and the accrual rates used.

(b)

Except as provided in paragraphs (1)(f), (1)(g) and (1)(h) charges to this

account must be made for all occurrences in accordance with the schedule of

risks to be covered which are not covered by insurance. Recoveries, insurance

proceeds or reimbursements for losses charged to this account must be credited

to the account.

(c)

A separate subaccount must be established for that portion of Account No. 228.1

which is designated to cover storm-related damages to the utility’s own

property or property leased from others that is not covered by insurance. The

records supporting the entries to this account must be so kept that the utility

can furnish full information as to each storm event included in this account.

(d)

In determining the costs to be charged to cover storm-related damages, the

utility must use an Incremental Cost and Capitalization Approach methodology

(ICCA). Under the ICCA methodology, the costs charged to cover storm-related

damages must exclude those costs that normally would be charged to non-cost

recovery clause operating expenses in the absence of a storm. Under the ICCA

methodology for determining the allowable costs to be charged to cover

storm-related damages, the utility will be allowed to charge to Account No.

228.1 costs that are incremental to costs normally charged to non-cost recovery

clause operating expenses in the absence of a storm. All costs charged to

Account 228.1 are subject to review for prudence and reasonableness by the

Commission. In addition, capital expenditures for the removal, retirement and

replacement of damaged facilities charged to cover storm-related damages must

exclude the normal cost for the removal, retirement and replacement of those

facilities in the absence of a storm. The utility must notify the Commission

Clerk in writing for each incident expected to exceed 1.5 percent of

jurisdictional revenues for the most recent calendar year.

(e)

The types of storm related costs allowed to be charged to the reserve under the

ICCA methodology include the following:

1.

Additional contract labor hired for storm restoration activities incurred in

any month in which storm damage restoration activities are conducted, that are

greater than the actual monthly average of contract labor costs charged to

operation and maintenance expense for the same month in the three previous

calendar years. The utility may adjust historical monthly contract labor costs

charged to operation and maintenance expense from calculated monthly average.

Each adjustment must be accompanied by a detailed explanation of the nature and

derivation of the adjustment;

2.

Logistics costs of providing meals, lodging, and linens for tents and other staging

areas;

3.

Transportation of crews and other personnel for storm restoration;

4.

Vehicle costs for vehicles specifically rented for storm restoration

activities;

5.

Waste management costs specifically related to storm restoration activities;

6.

Rental equipment specifically related to storm restoration activities;

7.

Materials and supplies used to repair and restore service and facilities to

pre-storm condition, excluding those costs that normally would be charged to

non-cost recovery clause operating expenses in the absence of a storm;

8.

Payroll and payroll-related costs for utility personnel included in storm

restoration activities incurred in any month in which storm damage restoration

activities are conducted, that are greater than the actual monthly average of

payroll and payroll-related costs charged to operation and maintenance expense

for the same month in the three previous calendar years. The utility may adjust

historical monthly payroll and payroll-related costs charged to operation and

maintenance expense from calculated monthly average. Each adjustment must be

accompanied by a detailed explanation of the nature and derivation of the

adjustment;

9.

Fuel cost for company and contractor vehicles used in storm restoration

activities incurred in any month in which storm damage restoration activities

are conducted, that are greater than the actual monthly average of fuel costs

charged to operation and maintenance expense for the same month in the three

previous calendar years. The utility may adjust historical monthly fuel costs

charged to operation and maintenance expense from calculated monthly average.

Each adjustment must be accompanied by a detailed explanation of the nature and

derivation of the adjustment;

10.

Cost of public service announcements regarding key storm-related issues, such

as safety and service restoration estimates;

11.

Vegetation management expenses specifically related to storm restoration

activities incurred in any month in which storm damage restoration activities are

conducted, that are greater than the actual monthly average of vegetation

management costs charged to operation and maintenance expense for the same

month in the previous three calendar years. The utility may adjust historical

monthly vegetation management costs charged to operation and maintenance

expense from calculated monthly average. Each adjustment must be accompanied by

a detailed explanation of the nature and derivation of the adjustment; and

12.

Other costs or expenses not specifically identified in paragraph (1)(e)1.

through (1)(e)11. that are directly and solely attributable to a storm

restoration event.

(f)

The types of storm related costs prohibited from being charged to the reserve

under the ICCA methodology include the following:

1.

Bonuses or any other special compensation for utility personnel not eligible

for overtime pay;

2.

Depreciation expenses, insurance costs and lease expenses for utility-owned or

utility-leased vehicles and aircraft;

3.

Utility employee assistance costs;

4.

Utility employee training costs incurred prior to 72 hours before the storm

event;

5.

Utility advertising, media relations or public relations costs, except for

public service announcements regarding key storm-related issues as listed above

in subparagraph (1)(e)10.;

6.

Utility call center and customer service costs, except for non-budgeted

overtime or other non-budgeted incremental costs associated with the storm

event;

7.

Utility lost revenues from services not provided; and

8.

Replenishment of the utility’s materials and supplies inventories.

(g)

Under the ICCA methodology for determining the allowable costs to be charged to

cover storm-related damages, certain costs may be charged to Account 228.1 only

after review and approval by the Commission. Prior to the Commission’s

determination of the appropriateness of including such costs in Account No.

228.1, the costs may be deferred in Account No. 186, Miscellaneous Deferred

Debits. The deferred costs must be incurred prior to June 1 of the year following

the storm event. By September 30 a utility must file a petition for the

disposition of any costs deferred prior to June 1 of the year following the

storm event giving rise to the deferred costs. These costs include the

following:

1.

Costs of normal non-storm related activities which must be performed by

employees or contractors not assigned to storm damage restoration activities

(“back-fill work”) or normal non-storm related activities which must be

performed following the restoration of service after a storm by an employee or

contractor assigned to storm damage restoration activities in addition to the

employee’s or contractor’s regular activities (“catch-up work”); and

2.

Uncollectible accounts expenses.

(h)

A utility may, at its own option, charge storm-related costs as operating

expenses rather than charging them to Account No. 228.1. The utility must

notify the Commission Clerk in writing and provide a schedule of the amounts

charged to operating expenses for each incident exceeding 0.5 percent of

jurisdictional revenues for the most recent calendar year. The schedule must be

filed annually by February 15 of each year for information pertaining to the

previous calendar year.

(i)

If the charges to Account No. 228.1 exceed the account balance, the excess must

be carried as a debit balance in Account No. 182.3 and no request for a

deferral of the excess or for the establishment of a regulatory asset is

necessary.

(j)

A utility may petition the Commission for the recovery of a debit balance in

Account No. 182.3 discussed in paragraph (1)(i) plus an amount to replenish the

storm reserve through a surcharge, securitization or other cost recovery

mechanism.

(k)

A utility must not establish or change an annual accrual amount or a target

accumulated balance amount for Account No. 228.1 without prior Commission

approval.

(l)

Each utility must file a Storm Damage Self-Insurance Reserve Study (Study) with

the Commission Clerk by January 15, 2022 and at least once every 5 years

thereafter from the submission date of the previously filed study. A Study must

be filed whenever the utility is seeking a change to either the target

accumulated balance or the annual accrual amount for Account No. 228.1. At a

minimum, the Study must include data for determining a target balance for, and

the annual accrual amount to, Account No. 228.1.

(2)

Account No. 228.2 Accumulated Provision for Injuries and Damages.

(a)

This account may be established to meet the probable liability, not covered by

insurance, for deaths or injuries to employees or others and for damages to

property neither owned nor held under lease by the utility. When liability for

any injury or damage is admitted or settled by the utility either voluntarily

or because of the decision of a Court or other lawful authority, such as a

workman’s compensation board, the admitted liability or the amount of the

settlement must be charged to this account.

(b)

Charges to this account must be made for all losses covered. Detailed

supporting records of charges made to this account must be maintained in such a

way that the year the event occurred which gave rise to the loss can be

associated with the settlement. Recoveries or reimbursements for losses charged

to the account must be credited to the account.

(3)

Account No. 228.4 Accumulated Miscellaneous Operating Provisions.

(a)

This account may be established for operating provisions which are not covered

elsewhere. This account must be maintained in such a manner as to show the

amount of each separate provision established by the utility and the nature and

amounts of the debits and credits thereto. Each separate provision must be

identified as to purpose and the specific events to be charged to the account

to ensure that all such events and only those events are charged to the

provision accounts.

(b)

Charges to this account must be made for all costs or losses covered.

Recoveries or reimbursements for amounts charged to this account must be

credited hereto.

(4)(a)

The provision level and annual accrual rate for each account listed in

subsections (1) through (3) must be evaluated at the time of a rate proceeding

and adjusted as necessary. However, a utility may petition the Commission for a

change in the provision level and accrual outside a rate proceeding.

(b)

If a utility elects to use any of the above listed accumulated provision

accounts, each and every loss or cost which is covered by the account must be

charged to that account and must not be charged directly to expenses except as

provided for in paragraphs (1)(f), (1)(g) and (1)(h). Charges must be made to

accumulated provision accounts regardless of the balance in those accounts.

(c)

No utility must fund any account listed in subsections (1) through (3) unless

the Commission approves such funding. Existing funded provisions which have not

been approved by the Commission must be credited by the amount of the funded

balance with a corresponding debit to the appropriate current asset account,

resulting in an unfunded provision.

Rulemaking

Authority 366.05(1) FS. Law Implemented 350.115, 366.04(2)(a) FS. History -

New______.