Discussion

of Issues

Issue 1:

Should the Commission approve FPL's calculation of

the tax savings associated with the IRA for 2022?

Recommendation:

Yes. The Commission should approve FPL’s

calculations for the net tax savings of $25,043,705 for 2022 resulting from the

Company’s election to use PTCs instead of ITCs as allowed by the IRA. (D. Buys,

Mouring)

Staff Analysis:

Effective January 1, 2022, the IRA expanded federal

income tax benefits for renewable energy by allowing owners of solar projects

which begin construction before 2025 the option to elect to receive Production

Tax Credits (PTCs) instead of Investment Tax Credits (ITCs). FPL has elected to

use PTCs instead of ITCs because it provides a greater tax benefit and customer

savings. The application of PTCs to FPL’s six rate base solar facilities

results in a tax savings of $31,195,561. In comparison, the amortization of

ITCs is $1,773,277 per year. The ITC amortization, and a $3,155,569 adjustment

to account for the impact to the capital structure due to a net decrease of

unamortized ITCs and accumulated deferred income taxes (ADITs), is deducted

from the PTC balance. In addition, State income tax expense increased by

$1,223,010 due to the removal of the ITCs and is also offset against PTC tax

savings. In total, the net change in FPL’s jurisdictional adjusted base revenue

requirement is a reduction of $25,043,705.[2]

Staff reviewed FPL’s calculations in the direct testimony of Ina P. Laney filed

on September 23, 2022, in the instant docket, and believes they are reasonable

and appropriate. FPL’s calculations are summarized in Table 1-1. Based on the

aforementioned, staff recommends the Commission approve FPL’s calculations of

net tax savings of $25,043,705 for 2022 resulting from the Company’s election

to use PTCs instead of ITCs as allowed by the IRA.

|

Table 1-1

|

|

Calculation

of PTC impact on 2022 Revenue Requirement

|

|

Production Tax Credits

|

$31,195,561

|

|

ITC Amortization Removal

|

(1,773,277)

|

|

State Income Tax Expense

|

(1,223,010)

|

|

ITC Capital Structure Impact

|

(3,155,569)

|

|

Net Reduction in 2022 Revenue Requirement

|

$25,043,705

|

Source: DN 07679-2022.

Issue 2:

Should the Commission approve FPL’s request to flow

back to customers the full 2022 tax reform impact through a one-time reduction

to its Capacity Cost Recovery Clause (CCR) factors in January 2023?

Recommendation:

Yes. Staff recommends the Commission approve a

refund of $25,043,705 in January 2023 through a one-time reduction to FPL’s CCR

factors. (Cordell)

Staff Analysis:

As discussed in Issue 1, FPL’s application of PTCs

has reduced its 2022 jurisdictional adjusted revenue requirement by

$25,043,705. Paragraph 13(a) of the 2021 Settlement states: “[a]ny effects of

tax reform on the retail revenue requirements (but no earlier than January 1,

2022) through the date of the base rate adjustment shall be flowed back to, or

collected from, customers through the [CCR] Clause on the same basis as used in

any base rate adjustment.”[3]

The impact of this refund on the capacity cost portion of

a 1,000 kilowatt-hour (kWh) residential bill for January 2023 will be a credit

of $0.75 on the 1,000 kWh residential bill. The Company believes applying the

entire 2022 refund to a single month, with a commensurate one-month rate

impact, will provide a more noticeable reduction to customers’ bills than

spreading the refund over a full twelve months. After January, or from February

through December 2023, the proposed residential capacity charge will be $2.12

per 1,000 kWh. Staff

has reviewed the Company’s calculation of the net tax savings from the

effective date of the IRA, through the base rate adjustment, and recommends the Commission approve a refund of

$25,043,705 in January 2023 through a one-time reduction to FPL’s CCR factors.

Issue 3:

Should the Commission approve FPL's calculation of

the projected tax savings associated with the IRA for 2023?

Recommendation:

Yes. The Commission should approve FPL’s

calculations of net tax savings of $69,743,460 for 2023 resulting from the

Company’s election to use PTCs instead of ITCs as allowed by the IRA. (D. Buys,

Mouring)

Staff Analysis:

As discussed in Issue 1, FPL has selected the option

to receive PTCs instead of ITCs as allowed by the IRA. The application of PTCs

to FPL’s ten solar facilities results in a tax savings of $82,432,142, which is

offset by a reduction to the ITC amortization balance of $12,688,682, for a net

tax savings of $69,743,460. The incremental change in 2023 jurisdictional

adjusted base revenue requirement is a reduction of $44,699,755, in addition to

the 2022 net tax savings of $25,043,705, for a total reduction in base revenue

requirement of $69,743,460.[5] FPL will

not finalize its 2023 Forecast Earnings Surveillance Report until early 2023,

and consequently, did not take into account the impacts to the capital

structure which would likely decrease the 2023 tax savings. FPL did not include

the 2023 State income tax impact which may also slightly decrease the tax savings

similar to its effect on the 2022 calculation. The projected change in FPL’s

base revenue requirements is comprised of a $82.4 million reduction due to

lower operating income tax expense resulting from the inclusion of PTCs

associated with the Company’s base rate solar plants, offset by a $12.7 million

increase due to the removal of ITC amortization associated with the 2022 and

2023 solar plants. FPL’s calculations are summarized in Table 3-1. Staff

reviewed FPL’s calculations in the direct testimony of Ina P. Laney filed on

September 23, 2022, in the instant docket, and believe they are reasonable and

appropriate. Based on the aforementioned, staff recommends the Commission

approve FPL’s calculations of net tax savings of $69,743,460 for 2023 resulting

from the Company’s election to use PTCs instead of ITCs as allowed by the IRA.

|

Table

3-1

|

|

Calculation

of PTC impact on 2023 Revenue Requirement

|

|

Production Tax

Credits

|

$82,432,142

|

|

ITC Amortization

Removal

|

(12,688,682)

|

|

Net Reduction in 2023

Revenue Requirement

|

$69,743,460

|

|

Decrease in 2022

Revenue Requirement

|

(25,043,705)

|

|

Incremental Reduction

in 2023 Revenue Requirement

|

$44,699,755

|

Source: DN 07679-2022.

Issue 4:

Should the Commission approve FPL's request to flow

back to customers the projected 2023 tax savings through a reduction to base

rates beginning January 1, 2023?

Recommendation:

Yes. The Commission should approve FPL’s request to

flow back to customers the projected net $69,743,460 tax savings through a

reduction to base rates beginning January 1, 2023. (D. Buys, Mouring)

Staff Analysis:

As discussed in Issue 3, the Company’s election to

utilize PTCs instead of ITCs under the IRA has resulted in a projected net tax

savings of approximately $69.7 million. Under the provisions of Paragraph 13 of

the 2021 Settlement, the Company is required to quantify the impacts of federal

or state tax reform on its jurisdictional base revenue requirement as projected

in its Forecast Earnings Surveillance Report and adjust its jurisdictional base

revenue requirement through a uniform percentage decrease or increase to

customer, demand, and energy base rates for all retail customer classes. Staff

has reviewed the Company’s calculation of the projected net tax savings

associated with the IRA and the proposed method to flow back those tax savings

to customers and recommends that the proposed permanent reduction in

jurisdictional base rates is consistent with the terms of the 2021 Settlement

and should be approved.

Issue 5:

Should the Commission approve FPL’s revised tariffs

to implement the IRA base revenue decrease effective January 2023?

Recommendation:

Yes. The Commission should approve FPL’s revised

tariffs to implement the IRA base revenue decrease effective January 2023. The

revised tariffs are shown in Attachment A to the recommendation. (Draper)

Staff Analysis:

FPL’s petition includes the proposed tariff sheets

(Exhibit D to the petition) and the calculation of the IRA adjustment factor of

(0.775) percent (Exhibit C to the petition).

The IRA adjustment factor was calculated by dividing the $69.7 million

reduction in the 2023 base revenue requirement by the 2023 projected retail

base revenue sales of electricity ($8,999.9 million). The IRA adjustment factor

was applied to the base rates for all rate classes (Exhibit C to the petition,

Part 2).

In Order No. PSC-2021-0446-S-EI, the Commission approved

an increase of $560 million in FPL’s base rates effective January 2023. This

Commission-approved increase is also reflected in the revised tariffs, as both

the approved $560 million base rate increase and the proposed IRA base revenue

decrease are effective January 2023.

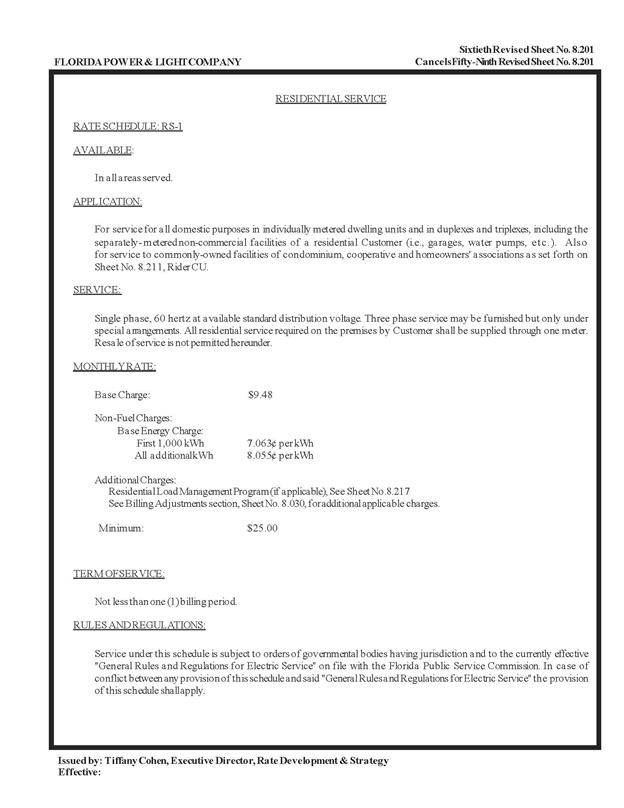

A residential customer who uses 1,000 kWh per month

currently pays $75.82 on the base rate portion of their monthly bill. Without

the IRA adjustment, the base rate portion on the 1,000 kWh residential bill

would be $80.73 effective January 2023. As a result of the IRA adjustment, the

base rate portion of the 1,000 kWh residential bill will be $80.11 effective

January 2023, an increase of $4.29 from the current $75.82.

Staff has reviewed FPL’s tariff sheets and supporting

documentation. The calculations are accurate.

The Commission should approve FPL’s revised tariffs to implement the IRA

base revenue decrease effective January 2023. The revised tariffs are shown in

Attachment A to the recommendation.

Issue 6:

Should this docket be closed?

Recommendation:

Yes. At the conclusion of the protest period, if no

protest is filed this docket should be closed upon the issuance of a

consummating order. If a protest is filed within 21 days of the issuance of the

order, the tariffs should remain in effect, subject to adjustment, pending the

resolution of the protest. (Brownless)

Staff Analysis:

At the conclusion of the protest period, if no

protest is filed this docket should be closed upon the issuance of a

consummating order. If a protest is filed within 21 days of the issuance of the

order, the tariffs should remain in effect, subject to adjustment, pending the

resolution of the protest.