Discussion

of Issues

Issue 1:

Should the Commission propose the amendment of Rule

25-14-004, F.A.C., Effect of Parent Debt on Federal Corporate Income Tax?

Recommendation:

Yes. The Commission should propose the amendment of

Rule 25-14.004, F.A.C., as set forth in Attachment A. The Commission should certify

the rule as a minor violation rule. (Sapoznikoff, Cicchetti, Guffey)

Staff Analysis:

Currently

the rule considers the debt of a parent company invested in a regulated,

subsidiary utility. Following adoption of the rule in 1983, regulatory theory and

practice, accounting principles, finance theory, economic theory, corporate

structure, and legal rulings have evolved. Consequently, use of consolidated

parent company data to set utility rates is no longer generally accepted and

the method in the recommended amendments has become the prevailing national

standard over time. By imputing a parent’s debt the current rule results in an

inaccurate revenue requirement which ultimately results in artificially low

rates that can adversely affect or increase the frequency of the need for rate

increases. Accordingly, the time has come to make a change. Staff recommends

that the rule be amended as set forth in Attachment A. Below is a detailed

discussion of staff’s recommended amendments to the rule.

Rule 25-14.004, F.A.C., Determination of

Total Corporate Income Tax

The

initial paragraph of the current rule is unnumbered and requires that when a

regulated utility is a subsidiary of one or more parent companies and files a

consolidated tax return with a parent company, the subsidiary’s income tax must

be adjusted to reflect the income tax expense of the parent debt that may be

invested in the equity of the subsidiary.

The

recommended amendments to the unnumbered introductory paragraph require that

the income tax expense of a regulated utility be determined using only its

income, regardless of any parent-subsidiary relationship that may exist. This

policy is referred to as the stand-alone approach. The stand-alone basis

ensures that the revenue requirement is based upon tax benefits associated with

the debt that is both an expense of the regulated utility and borne by that

utility’s customers.

Overall,

staff recommends changing Commission policy on how to determine the income tax

expense of a regulated utility that is a subsidiary of one or more parent

companies to align the rule with the current national standard.[5] Under the current rule, the

tax benefits associated with the parent company’s interest expense are

attributed to the subsidiary utility. This inappropriately lowers utility

rates, distorts price signals, and contributes to the inefficient allocation of

resources. Under the recommended amendments to Rule 25-14.004, F.A.C., the

Commission would use only the interest expense inherent in the

capital structure of the regulated utility to compute income tax expense,

rather than reducing the tax expense in accordance with the parent’s capital

structure.

If

the Commission votes to approve the recommended policy change, the recommended

amendments to subsections (1) through (4) and the addition of subsection (5) are

necessary to reflect the change in the process of making tax determinations from

incorporating parent debt to only using the tax expense of the regulated

utility. Staff’s recommendations for the amendment of each subsection of the

rule is below.

Subsection (1)

Subsection

(1) of the current rule addresses how to calculate the income tax effect of the

parent’s debt when there is only one parent company.

As

parent debt is not a consideration in the recommended amendments, the recommended

amendment of subsection (1) deletes the prior language in its entirety. In its

place the recommended rule language of subsection (1) sets forth the method of

determining state corporate current income tax of the regulated, subsidiary

utility. This amount is calculated by multiplying the

regulated utility’s state taxable income before state and federal income taxes

by Florida’s corporate income tax rate, plus or minus any applicable tax

adjustments or credits in accordance with applicable state income tax laws and

regulations.

Subsection (2)

Subsection

(2) of the current rule addresses how to calculate the income tax effect of the

parent’s debt when there is more than one parent company.

As

parent debt is not a consideration in the recommended amendments, the

recommended amendment of subsection (2) deletes the prior language in its

entirety. In its place, the recommended rule language of subsection (2) sets

forth the method of determining the federal taxable income of the regulated,

subsidiary utility after state corporate income tax. This amount is calculated by

deducting the state corporate income tax amount calculated pursuant to the

recommended amendment of subsection (1) from the regulated utility’s federal

income before taxes.

Subsection (3)

Subsection

(3) of the current rule addresses what is included in the capital structure of

the parent and notes that it is a rebuttable presumption that “a parent’s

investment in any subsidiary or in its own operations shall be considered to

have been made in the same ratios as exist in the parent’s overall capital

structure.”

As

parent debt is not a consideration in the recommended amendments, the recommended

amendment of subsection (3) deletes the prior language in its entirety. In its

place, the recommended rule language of subsection (3) sets forth the method of

determining the federal current corporate income tax of the regulated,

subsidiary utility. This amount is calculated by multiplying the federal

taxable income after state taxes (which amount was calculated

pursuant to the recommended amendment of subsection (2)), by the federal

corporate income tax rate, plus or minus any applicable tax adjustments

or credits in accordance with applicable federal income tax laws and

regulations.

Subsection (4)

Subsection

(4) of the current rule addresses how to calculate the parent debt adjustment

using debt ratio and debt cost of the parent, the statutory tax rate applicable

to the consolidated entity, and the equity dollars of the regulated subsidiary,

excluding its retained earnings.

As

parent debt is not a consideration in the recommended amendments, the

recommended amendment of subsection (4) deletes the prior language in its

entirety. In its place, the recommended rule language of subsection (4) clarifies

that applicable temporary adjustments to taxable income multiplied by the

respective federal and state corporate income tax rates, plus or minus any

applicable tax adjustments or credits in accordance with applicable federal and

state income tax laws and regulation, shall be used in determining federal and

state income tax expenses for the regulated utility.

Subsection (5)

The

current version of the rule does not contain a subsection (5). The recommended

amendment of the rule adds subsection (5), which states that total income tax

expense for the regulated utility will be determined by adding the amounts

calculated pursuant to the recommended amendments of subsections (1), (3), and

(4) of the rule.

Stakeholder Comments

All

stakeholders who commented, except for OPC, support the recommended amendments

to Rule 25-14.004, F.A.C. OPC’s objections to the recommended amendment of the

rule fall into two main categories. First, OPC opposes the recommended amendment

of the rule because it alleges the stand-alone method will inappropriately

increase rates and result in double-leverage. Next, OPC alleges that precedent

disallows the stand-alone method contained in the recommended amendments to the

rule. As discussed below, staff disagrees with OPC’s comments.

The recommended amendments align the rule

with current national standards and will not inappropriately increase rates or result

in double leverage.

In

essence, the parent-debt adjustment (recognizing double leverage) perverts the

calculation of return on equity (ROE). In a rate proceeding, the Commission

determines the appropriate ROE and capital structure (i.e., the appropriate debt

and equity ratios), which reflect the utility’s cost of obtaining funds. The

parent-debt adjustment imputes the tax deduction associated with parent company

debt to the regulated utility. However, because the regulated utility did not

incur the parent’s interest expense, the regulated utility cannot claim that

expense on its taxes and reduce its costs.

When

the current rule is applied, the utility does not collect the actual cost of

providing utility service. Consequently, the utility may seek rate increases

more frequently incurring additional rate case expense. Moving away from the

parent debt adjustment and adopting the stand-alone approach is also beneficial

to rate payers. Setting rates on a stand-alone basis ensures only the costs

associated with the provision of utility service are charged to customers.

Under [the] stand-alone

methodology, a regulated entity's income tax allowance is based on the income

and deductions specifically attributable to the regulated entity's

jurisdictional cost of service and the income tax allowance does not

incorporate potentially offsetting losses and deductions of the parent owner

not reflected in the regulated entity's jurisdictional cost of service.

Trailblazer Pipeline Co., LLC,

166 F.E.R.C. P61141, 61674, 2019 WL 830962, at *10 (FERC Feb. 21, 2019) (citing

City of Charlottesville v. Fed. Energy

Reg. Comm’n, 774 F.2d 1205, 1215 (1985), cert. den’d, 475 U.S. 1108

(1986)).

While

some cases have described the stand-alone approach as relying on a

“hypothetical” calculation, using the parent debt adjustment artificially

decreases the regulated utility’s tax expense and lowers the regulated

subsidiary’s revenue requirement. While the parent debt adjustment approach

lowers rates, it results in a revenue requirement based upon tax benefits

associated with debt that is neither an expense of the utility nor borne by the

utility’s customers. If taxes are allocated in a manner other than on a

stand-alone basis, utility customers may pay rates that reflect costs or

benefits of other nonregulated members of the consolidated group.

In

its written comments, OPC alleges that staff’s concern that application of the

rule results in “double leverage” is unfounded. However, contrary to OPC’s

allegations, the cases that advance a parent-debt adjustment do so for

double-leverage. See, e.g., New England

Tele. & Teleg. Co. v. Pub. Utils. Comm’n, 390 A.2d 8, 28-47 (Me. 1978).

Double leverage occurs when a subsidiary enjoys its own leverage (use of debt

instead of all equity capital) plus the leverage factor of its parent company

(which also uses some debt instead of all equity capital). See id. at 41.

Of

the utilities providing comments, DEF, FPL,

FCG, FPUC, PGS, and TECO

agree with staff’s rationale for the recommended amendment of the rule. FPL and

its affiliates note the rule’s effect is that the “parent company’s debt is

imputed to the benefit of customers even though customers are not obligated to

pay rates reflecting the interest expense on the parent’s debt in rates” which may

result in the need to file requests for “more frequent and costly base rate

increases, which will further increase rates paid by customers.” They assert

that “to mitigate this costly and time-consuming potential that rates should

reflect the taxes associated with only the items that are included in the cost

of service and net operating income directly attributable to them.” TECO’s

comments generally adopt those submitted by FPL and its affiliates.

DEF

agrees that “the better approach is to compute the regulated utility’s tax

expense on a stand-alone basis without making the adjustment currently called

for in the Rule.” DEF asserts that the stand-alone approach “provides a match

between capital structure interest and the tax effect considered in the

regulated utility’s cost of service.” Because capital structure is always

determined in a base rate proceeding, DEF contends that the “Commission is

assured that the capital structure has been properly set.”

There is no precedent disallowing the

stand-alone method.

In

its oral and written comments, OPC argues “there is no basis to change a

40-year old consumer protection rule that has survived challenges in the

Florida Supreme Court, the United States Treasury Department and the United

States Congress.” OPC further argues that the Commission has twice considered

and denied repeal of the rule. OPC states the rule is “a fundamental bedrock

principle of Florida utility regulation that has been applied to keep Florida

customer utility rates low for 45 years.”

Staff

believes there is no indication that the rule was designed with consumer

protection in mind nor that the recommended amendments to the rule would harm

consumers. Just because the rule has survived challenges does not mean it has

been endorsed as the only or proper way to assess tax liability. In fact, as

discussed in more detail below, the cases to which OPC cites support the stand-alone

method contained in the recommended amendments to the rule.

Florida

Supreme Court precedent does not preclude the stand-alone method.

OPC

asserts the current version of the rule was unequivocally upheld by the Florida

Supreme Court in General Tele. Co. of

Fla. v. Fla. Pub. Serv. Comm’n, 446 So. 2d 1063 (Fla. 1984). OPC further

argues General Telephone supported

the Court’s prior decision in Citizens of

Fla. v. Hawkins, 356 So. 2d 254 (Fla. 1978), which OPC alleges stands for

the proposition that “the regulated utility’s tax deductible debt may cause

customers to overpay on the income tax component imbedded in their rates.” As

explained below, staff believes OPC has misconstrued the holdings of those

cases.

Citizens of Fla. v. Hawkins,

356 So. 2d 254 (Fla. 1978), was the first Florida Supreme Court case to address

the Commission’s computation of the income tax for a regulated entity that was

a subsidiary and filed a consolidated return with a parent company. At that

time, the Commission did not have a rule on that matter, but traditionally used

what was referred to as a “subsidiary approach” rather than a “consolidated

approach.” The “subsidiary approach” was described as using “an allowance for

federal income tax expense equal to the hypothetical tax which would have been

paid if [the subsidiary] had filed a separate federal income tax return.” Hawkins, 356 So. 2d at 259. In Hawkins, OPC argued that use of the

“subsidiary approach” resulted in double-leverage as the regulated entity was

able “to receive an allowance for income tax expense greater than the actual

income tax liability for which it would be properly responsible under [the]

consolidated return.” Id.

In

Hawkins, the Commission noted that

OPC did not object to using the “subsidiary approach” to calculate the cost of

capital and, accordingly, it would be consistent also to do so in determining

tax effect. Id. However, unable “to

discern a rationale for a rule of consistency” and finding that the

Commission’s order “nowhere identified a record basis for preferring...the subsidiary

approach over a calculation on the consolidated approach,” the Court held that

“each [tax] determination must be based on specific independent findings

supported by competent substantial evidence” and that “what evidence there is

in the record supports the consolidated approach as being more accurate.” Id. at 259-260 (citations omitted).

Thus,

contrary to OPC’s suggestions, Hawkins

did not mandate application of the consolidated approach. Rather, the Court

merely held that under the facts of that case, the consolidated approach was

supported by the record evidence. See id.

Thereafter,

the current rule (mandating the consolidated approach) was adopted in 1983.

Although the Florida Supreme Court upheld the validity of the rule in General Tele. Co. of Fla. v. Fla. Pub. Serv.

Comm’n, 446 So. 2d 1063 (Fla. 1984), it was not necessarily a substantive

endorsement. Rather, the Court only evaluated whether the rule was “reasonably

related to the purposes of the enabling legislation, and. . . not arbitrary or

capricious.” General Tele., 446 So.

2d at 1067 (quoting Agrico Chem. Co. v.

State, Dep’t of Env. Reg., 365 So. 2d 759 (Fla. 1st DCA 1978), cert. den’d, 376 So. 2d 74 (Fla. 1979)).

While

the Court acknowledged that it had previously “instructed the PSC to apply this

type of adjustment in a ratemaking case,” it qualified that statement by

stating:

There is no single correct

method of dealing with the income tax expense of a subsidiary-utility joining

in the filing of a consolidated return. By choosing this particular method, the

PSC is merely acting within the scope of its discretion.

General Tele.,

446 So. 2d at 1067. Therefore, the recommended amendments to the rule are

within the discretion of this Commission and reflect nationally recognized best

practices.

Moreover,

while General Telephone noted that

the Federal Energy Regulation Commission (FERC) and “at least eighteen

jurisdictions” had adopted the consolidated approach,[10]

that is no longer the case. FERC now uses the stand-alone approach reflected in

the recommended amendments to the rule,[11]

and Florida is one of only a handful of states that still use a consolidated

approach. States that have adopted the stand-alone approach have done so “due

to the increasing structural complexity of regulated utility entities and the

expansion of non-utility activities by subsidiaries.” SFPP, L.P. v.

Public Utils. Comm’n, 217 Cal. App.

4th 784, 795 (2013). In addition, “without the stand-alone treatment of the

regulated entity, the non-utility activities could result in a tax expense or

savings unrelated to the costs of providing utility service.” ARCO

Prods. Co. v. Santa Fe Pacific Pipeline, L.P., Dec.

No. 11–05–045, 2011 WL 2246059 at 8 (Cal. P.U.C. 2011).

United

States Treasury and Congressional inaction do not preclude the stand-alone

method.

OPC

also asserts that inaction by the U.S. Treasury and Congress indicated that the

stand-alone method is improper. OPC states that in 1990, the U.S. Treasury

proposed a regulation that many interpreted “as an indication that the [parent

debt adjustment] could be deemed a consolidated tax savings adjustment and a

normalization violation.” According to OPC, it and the Commission joined in

filing comments at a 1991 IRS hearing on the matter and were in agreement that

the parent debt adjustment was not a consolidated tax savings adjustment or a

normalization violation. According to OPC, of the hundreds of parties (which OPC

asserts included utilities, consumers, and regulatory agencies), no one

supported the regulation. OPC further states that the IRS eventually withdrew

the proposed regulation. OPC advises that Congress also was “concerned about

whether normalization was costing the United States Treasury tax revenue” and

held hearings. According to OPC, it and the Commission testified before

Congress “in support of the rule and the Commission’s practice to recognize the

tax effect of parent company debt in ratemaking.” OPC states that Congress took

no action. OPC does acknowledge that by that time FERC had retreated from a

parent debt adjustment.

OPC’s

reliance on the failure of the IRS to change its consolidated return rule as

validation of the parent debt rule is misplaced. The proposed Treasury regulation

may have resulted in the Commission’s parent debt adjustment rule violating a

normalization method of accounting. However, the failure of the IRS to change

its policy (regarding the flow-through of tax savings arising from the filing

of a consolidated return) does not mean the IRS endorsed the parent debt

adjustment contained in the rule, or that the rule was the proper or only way

for the Commission to determine a subsidiary’s taxes when setting rates.

Moreover,

federal tax policy and rate setting by a utility commission are two distinct regulatory

mechanisms. See Federal Power Comm’n v.

United Gas Pipe Line Co., 386 U.S. 237, 243 (1967). The Court noted that a

commission has the power “to limit cost of service to real expense” and that

doing so would not frustrate tax laws. Id.

at 245-47.

Prior

Commission orders do not preclude the stand-alone method.

In

its oral comments, OPC asserts that the Commission had twice previously been

asked to repeal the parent-debt adjustment and had twice rejected that request.

That is not correct. The Commission has never substantively rejected repeal of

the parent-debt adjustment.

In

1987, staff submitted a recommendation to repeal the rule asserting that the

rule was unnecessary and that the litigation process would resolve the tax

matter.

The Commission deferred ruling and requested that staff submit a new

recommendation.

In

1988 the Commission considered the new recommendation which provided argument both

in support of the rule and also in support of its repeal.

Again, the Commission did not affirmatively reject repeal of the rule. Rather,

the Commission order simply stated, “[w]e do not wish to revisit the rule at

this time.”[15]

Moreover,

in contrast to the options previously submitted of either repealing or keeping

the parent debt adjustment, the current recommended amendment of Rule

25-14.004, F.A.C., sets forth an alternative approach which updates the rule to

conform to best practices.

Minor Violation Rule Certification

Pursuant

to Section 120.695, F.S., for each rule filed for adoption, the agency head

shall certify whether any part of the rule is designated as a rule the

violation of which would be a minor violation. Rule 25-14.004, F.A.C., is

currently listed as a minor violation rule by the Commission. This rule is a

minor violation rule because the violation of this rule would not result in

economic or physical harm to a person, cause an adverse effect on the public

health, safety, or welfare, or create a significant threat of such harm.

Violations of Rule 25-14.004, F.A.C., with the recommended amendments would

continue to be minor violations. Therefore, for the purposes of filing the

proposed amended rules for adoption with the Department of State, staff

recommends that the Commission certify Rule 25-14.004, F.A.C., as a minor

violation rule.

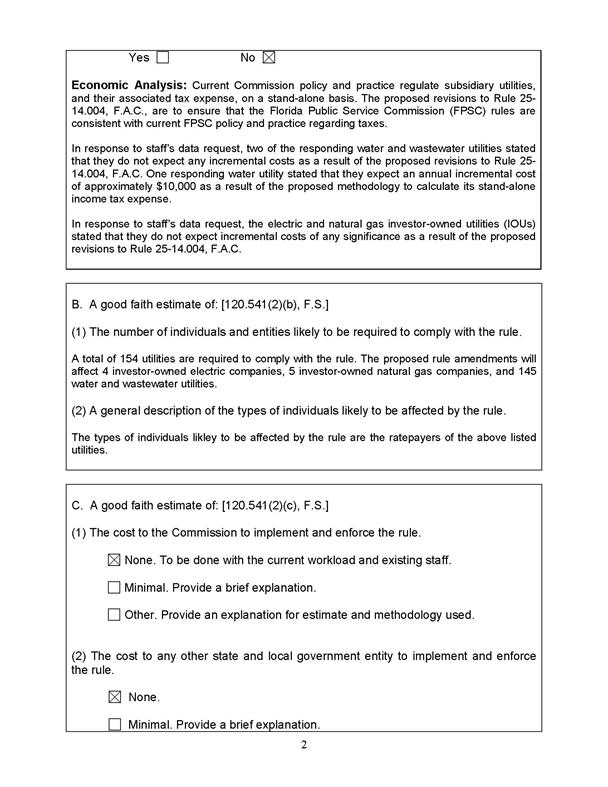

Statement of Estimated Regulatory Costs

Section

120.54(3)(b)1., F.S., encourages agencies to prepare a Statement of Estimated

Regulatory Costs (SERC) before the adoption, amendment, or repeal of any rule.

A SERC was prepared for this rulemaking and is appended as Attachment B. As

required by Section 120.541(2)(a)1., F.S., the SERC analysis includes whether the

rule amendments are likely to have an adverse impact on economic growth,

private sector job creation or employment, or private sector investment in

excess of $1 million in the aggregate within five years after implementation.

None of the impact/cost criteria will be exceeded as a result of the

recommended amendments.

The

SERC concludes that the amendments to the rule will likely not directly or

indirectly increase regulatory costs in excess of $200,000 in the aggregate in

Florida within one year after implementation. Further, the SERC concludes that

the recommended rule amendments will not likely increase regulatory costs,

including any transactional costs, or have an adverse impact on business

competitiveness, productivity, or innovation, in excess of $1 million in the

aggregate within five years of implementation. Thus, pursuant to Section

120.541(3), F.S., the recommended amendment of the rule does not require

legislative ratification.

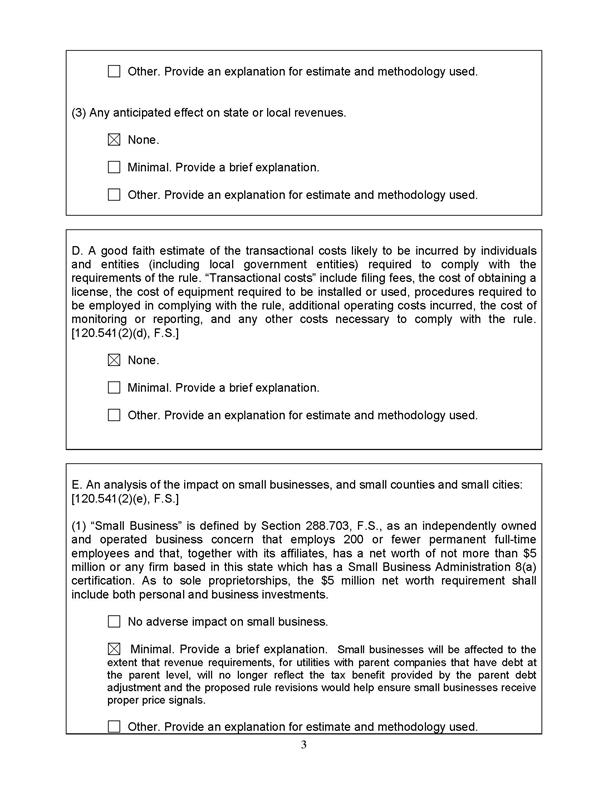

In

addition, the SERC states that the recommended amendments to the rule would

have no impact on small businesses, would have no implementation or enforcement

costs on the Commission or any other state or local government entity, and

would have no impact on small cities or small counties. The SERC states that

there will be no transactional costs likely to be incurred by individuals and

entities required to comply with the requirements.

Conclusion

The Commission should propose the amendment of

Rule 25-14.004, F.A.C., as set forth in Attachment A. Staff also recommends

that the Commission certify the rule as a minor violation rule.

Issue 2:

Should this docket be closed?

Recommendation:

Yes. If no requests for hearing or comments are

filed, the rule should be filed for adoption with the Department of State, and

the docket should be closed. (Sapoznikoff)

Staff Analysis:

If no requests for hearing or comments are filed,

the rule should be filed for adoption with the Department of State, and the

docket should be closed.